-

VideoNuze Podcast #344: A Busy Week in the Video Industry

I'm pleased to present the 344th edition of the VideoNuze podcast with my weekly partner Colin Dixon of nScreenMedia.

This week was busier than usual in the video industry and on today’s podcast, Colin and I discuss a number of news items that hit our radar. First we talk about the new Google-CBS deal for the upcoming Unplugged skinny bundle. Next up is VUDU’s Movies on Us, new free, ad-supported VOD service which we both think has potential. We then dig into Facebook’s new feature for advance scheduling and promoting live broadcasts. Finally we review LeEco’s new content and TVs (Colin attended the company’s big launch event this week.)

Clearly there was a lot happening this week as major players in the video industry continue jockeying for position. One news item that broke after we recorded is the rumor about AT&T acquiring Time Warner. That type of deal would be straight out of the Comcast-NBCU playbook and could trigger even more distribution-content tie-ups.

Listen in to learn more!

Click here to listen to the podcast (26 minutes, 17 seconds)

Click here for previous podcasts

Click here to add the podcast feed to your RSS reader.

The VideoNuze podcast is also available in iTunes...subscribe today!Categories: FIlms, Live Streaming, Podcasts, Skinny Bundles

Topics: AT&T, CBS, Facebook, Google, LeEco, Podcast, Time Warner, VUDU

-

Google, VUDU and LeEco: 3 More Potential Video Disruptions Coming?

Each week brings more innovation, product announcements and new business models to the ever-changing video industry. This week was certainly no different, and news from 3 companies - Google (a deal with CBS for its Unplugged skinny bundle), VUDU (a new ad-supported on-demand movie offering) and LeEco (a range of new products from the Chinese giant, including TVs and content) - caught my attention. Each has the potential to cause further industry disruption, or amount to nothing. Below I share thoughts on each.

Categories: Advertising, Broadcasters, Devices, FIlms, Skinny Bundles

Topics: Google, LeEco, VUDU, Wal-mart

-

VideoNuze Report Podcast #113 - Verizon and the OTT Market

I'm pleased to be joined once again by Colin Dixon, senior partner at The Diffusion Group, for the 113th edition of the VideoNuze Report podcast, for Dec. 9, 2011. In today's podcast Colin and I discuss this week's rumors of Verizon potentially launching an OTT subscription video service outside its market areas. As I wrote earlier this week, I'm skeptical of their ability to succeed, but Colin is more sanguine.

Adding to this week's intrigue was a separate report suggesting that Verizon intends to team up with Redbox on the initiative. Meanwhile Verizon isn't willing to talk about any of this, and these days you can't be sure what to believe. Beyond Verizon, in the podcast we also discuss other players' role in the OTT space such as YouTube, Dish, Amazon and Vudu, and how they're each positioned. Listen in to learn more!

Click here to listen to the podcast (16 minutes, 27 seconds)

Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!Categories: Aggregators, Podcasts, Telcos

Topics: Amazon, DISH, Podcast, Verizon, VUDU, YouTube

-

Verizon Needs to Bring More than a Knife to the OTT Gunfight

Late yesterday Reuters reported that Verizon is looking at launching an online-only subscription service for streaming movies and TV shows outside its geographical footprint. While such a move initially seems disruptive to incumbents like Netflix and others, the folks at Verizon better remember the old adage about not bringing a knife to a gunfight; if they really want to compete, significant investments in content and promotions are going to be required. Even then, it's not yet clear to me how Verizon succeeds in this highly competitive space.

such a move initially seems disruptive to incumbents like Netflix and others, the folks at Verizon better remember the old adage about not bringing a knife to a gunfight; if they really want to compete, significant investments in content and promotions are going to be required. Even then, it's not yet clear to me how Verizon succeeds in this highly competitive space.

Categories: Aggregators, Telcos

Topics: Amazon, CBS, EPIX, HBO, Netflix, Starz, Time Warner, UltraViolet, Verizon, VUDU, YouTube

-

With Recent Deals, OTT Distributors' Content Strategies Are Crystallizing

Amid the drama and headlines surrounding OTT distributors (e.g. Netflix price increases and Qwikster decision, on-again/off-again Hulu sale, etc.), these companies' content strategies actually seem to be crystallizing, with each trying to stake out a somewhat distinct value proposition for their users. True, there is still plenty of blurriness between them, and each appears reluctant to be pigeon-holed, but recent deals suggest how each OTT distributor is positioning itself.

Below is a summary of the content strategies of most of the major OTT distributors (Netflix, Hulu, Amazon, YouTube, Walmart/VUDU, iTunes and Blockbuster) with a catchphrase that best describes their approach:

Categories: Aggregators

Topics: Amazon, Blockbuster, Hulu, iTunes, Netflix, VUDU, YouTube

-

Winners and Losers Due to Netflix's Decision to Split DVDs

Netflix's bizarre decision to separate its DVD business from its streaming business will have significant ramifications for the video ecosystem. Below are some of the clear winners, potential winners and clear losers.

Categories: Aggregators

Topics: Amazon, Apple, Blockbuster, DISH, Facebook, Google, Hulu, Netflix, Redbox, VUDU, YouTube

-

Digital Movie Purchase and Rental Activity Remains Anemic

Earlier this week IHS Screen Digest Media Research released market share information for the top 5 U.S. digital/online movie stores for the first half of 2011, which together represent approximately 96% of the market. In addition, IHS released information on revenues generated for both purchase/download (Electronic sell-through or "EST") and rental (Internet video on demand or "iVOD").

In the chart below, I've taken the IHS data a step further to estimate each of the top 5 stores' revenues and transaction volume from EST and iVOD (note IHS only provides combined EST+iVOD market share information so for simplicity I have assumed each individual store's share is the same for both EST and iVOD though no doubt there are some variations). The data leads to a clear conclusion that years after movies have been available for digital purchase/download and rental, activity remains anemic, suggesting very low levels of consumer interest, particularly as compared with DVD purchase or rental/subscription options.

Categories: Aggregators, Commerce, FIlms

Topics: Amazon, IHS, iTunes, Microsoft, Sony, VUDU, Wal-Mart

-

Will Wal-Mart Expand VUDU Into Subscriptions and Compete With Netflix?

Wal-Mart's news this week that it has more deeply integrated its movie streaming service VUDU into its web site and e-commerce operations is a good step forward in competing better with Amazon and iTunes. However, because the vast majority of users prefer all-you-can-eat subscription services, the reality is that VUDU's new visibility will likely have little impact on Netflix (except maybe for lighter users who are upset by Netflix's recent price change and aren't deterred by VUDU's per title rental model and restrictive expiration policies).

good step forward in competing better with Amazon and iTunes. However, because the vast majority of users prefer all-you-can-eat subscription services, the reality is that VUDU's new visibility will likely have little impact on Netflix (except maybe for lighter users who are upset by Netflix's recent price change and aren't deterred by VUDU's per title rental model and restrictive expiration policies).

That raises the question of when might Wal-Mart really step up to the plate and expand VUDU into subscriptions, offering a true alternative to Netflix? It seems like the time may finally be right to make the move. In particular, Netflix's recent price change, separating DVD-by-mail and streaming-only services presents a golden opportunity for Wal-Mart to go on the offensive. Here's the logic:

Categories: Aggregators

Topics: CBS, NBCU, Netflix, VUDU, Wal-Mart

-

As DVD Sales Wane, Experiments With Movies' Digital Delivery Windows Rise

Yesterday brought more evidence of how digital distribution release windows and promotions are rising as DVD sales wane. First there was news that Disney had teamed up with Wal-mart to allow buyers of the Toy Story 3 DVD to get a bonus digital version of the film playable through the company's recently acquired Vudu digital outlet. That offer was quickly one-upped by Amazon which announced an increase from 300 to 10,000 movies in its "Disc+" program, which provides a digital copy to the user's Amazon VOD account when they purchase a qualifying DVD.

Meanwhile at the Blu-con conference in Beverly Hills, studio executives debated how to best calibrate digital, VOD and DVD distribution. Even emerging practices come with exceptions and debates about results. For example, while VOD has largely gained day-and-date release with DVD, exceptions are still made on a case-by-case basis, such as with Universal's "Despicable Me" which will have its DVD go on sale on Dec 14, but its VOD release not until after Christmas.

Topics: Amazon, Apple, Best Buy, Disney, EPIX, FOX, Netflix, Sony, Starz, Universal, VUDU, Wal-Mart, Warner Bros.

-

thePlatform Unveils Support for Numerous Over-the-Top Devices

thePlatform is announcing this morning that it has integrated with numerous "over-the-top" consumer electronics devices, enabling its content customers to more easily deliver online video to them. Devices cited are boxee, Roku, TiVo, Vudu (which includes connected TVs and Blu-ray players from LG, Mitsubishi, Samsung, Toshiba and Vizio), DivX devices, Syabas (popbox), FlingoTV and others to come (including Google TV when ready). I caught up with Marty Roberts, thePlatform's VP of Sales and Marketing yesterday to learn more.

to more easily deliver online video to them. Devices cited are boxee, Roku, TiVo, Vudu (which includes connected TVs and Blu-ray players from LG, Mitsubishi, Samsung, Toshiba and Vizio), DivX devices, Syabas (popbox), FlingoTV and others to come (including Google TV when ready). I caught up with Marty Roberts, thePlatform's VP of Sales and Marketing yesterday to learn more.

Marty explained the impetus was thePlatform's content customers telling the company they want to generate more video views and have easy access to the range of OTT devices coming to market. While conceding that the universe of all these devices combined is still probably in the low single-digit millions, thePlatform and its content customers are betting on future growth. The move is significant as it underscores the mindshare that direct access to TVs via broadband and connected devices has gained in the content community.

Categories: Devices, Technology

Topics: Boxee, DivX, FlingoTV, Google TV, LG, Mitsubishi, Roku, Samsung, Syabas, thePlatform, TiVo, Toshiba and Vizio, VUDU

-

Sezmi is Slick; Marketing It Will Be the Big Challenge

While in LA this week, I caught up with Phil Wiser, Sezmi's president and co-founder and got another good look at the Sezmi service, which just officially launched in the entire LA market with Best Buy. I've been covering Sezmi for over 3 years, and from a technical and product standpoint, I continue to be impressed with what it has accomplished, especially for a 1.0 launch. Out-of-the box set up is very straightforward and a series of intuitive menus quickly creates a personalized user profile complete with recommended shows based on your interests and selections from linear and on-demand channels.

Sezmi gained my attention early on because unlike other broadband-only devices (e.g. Roku, Vudu, ZillionTV, AppleTV, gaming consoles, etc.), Sezmi's goal has always been to become a full replacement for existing multichannel video programming distributors ("MVPDs"). That "boil the ocean" strategy has

required it to develop its own hybrid broadcast/broadband content delivery system, sign up local broadcasters for access to their bandwidth, ink carriage deals with cable networks and design the user experience from scratch, among other things. Having done much of that work (with a key exception being to still get the remaining cable channels from Disney/ESPN, Fox, Scripps and A&E into the line-up), Sezmi's next challenge is to actually market the service and add subscribers cost-effectively. This could well prove to be Sezmi's biggest challenge.

required it to develop its own hybrid broadcast/broadband content delivery system, sign up local broadcasters for access to their bandwidth, ink carriage deals with cable networks and design the user experience from scratch, among other things. Having done much of that work (with a key exception being to still get the remaining cable channels from Disney/ESPN, Fox, Scripps and A&E into the line-up), Sezmi's next challenge is to actually market the service and add subscribers cost-effectively. This could well prove to be Sezmi's biggest challenge.The market for multichannel video subscriptions has never been more competitive than it is today. Deep-pocketed cable operators, satellite operators and telcos (and in some places 3rd party "overbuilders" like RCN) are beating the hell out of each other in many U.S. geographies. For example, here in the Boston area we're bombarded daily with ads on radio, in newspapers, in direct mail, through door-hangers and other means, to switch providers. While there are a lot of noisy promotional offers, there are plenty of product and technology-based pitches as well - more HD channels, faster broadband speeds, better VOD and so on. The "triple play" bundle of video, voice and data is a significant marketing lever. I don't know what the marketing cost per acquired customer is for Comcast or Verizon these days, but I have no doubt it has never been higher.

This is battleground that Sezmi is now entering after nearly four years of development. Many people are skeptical about Sezmi's odds of success (read TDG president Michael Greeson's well-done piece from last week for a rundown of the issues), at least as Sezmi is currently configured. Some of these concerns are very valid, in particular Sezmi's $299 upfront equipment fee (which is pretty much unique in the industry), its currently incomplete channel lineup (note also that HBO, Showtime and Starz are also not available) and the $20/mo rate which is marginally better than alternatives (but is likely to increase anyway as more channels and especially expensive ones like ESPN are added).

No question, Sezmi faces a steep marketing challenge. Still, I believe there are reasons for optimism. First, as Sezmi has said many times, it is not a box company and Best Buy isn't its only route to market. It plans deals with telco and ISP partners who will not only bundle its pricing but also erase the upfront charge through a rental model. The rental could be very aggressive depending on the partner's goals, opening up more pricing competitiveness for Sezmi. Second, Sezmi's user interface and certain product features are very compelling differentiators. Granted, incumbent MVPDs are not standing still (see Cablevision's "Media Relay" announcement just yesterday), but the fact that Sezmi owns its whole system from end to end gives it more control and flexibility to enhance the product (for example in VOD it is not relying on traditional vendors).

Lastly, and I'll admit this is where things get fuzzy, but I do think there's a segment of existing MVPD customers who hunger for something new, better and lower cost than is currently available. I've made the analogy for Sezmi to what JetBlue has done in the airline industry and I think that still holds. Depending on how distinctive Sezmi's positioning and messaging is, I think it could really resonate with younger, urban, tech-savvy users. One Sezmi feature alone - access to all YouTube videos - is a totally new value proposition. Phil and I quickly searched YouTube yesterday for "Alec Baldwin Hulu Super Bowl Ad" and in seconds there it was. Can any other MVPD offer that today?

There are plenty of reasons to discount Sezmi's chances of success, but I think that's premature thinking, especially given how dynamic the video landscape is today. But even if Sezmi doesn't thread the needle and fully surmount the marketing challenges ahead, the company still has a lot of value in its technology and products. If Vudu fetched a reported $100 million from Wal-Mart, and Sling got $380 million from DISH as announced a couple years ago, then there should be a palatable financial exit in store for Sezmi as well, even with $75 million or so invested to date. Of course its investors and executives are hoping for far more than just a "palatable" final chapter. The real test of what's in store for Sezmi is just now beginning.

What do you think? Post a comment now (no sign-in required).

Categories: Cable TV Operators, Satellite, Telcos

Topics: Comast, SezMi, Sling, TDG, Verizon, VUDU

-

Wal-Mart's Acquisition of Vudu Makes Little Difference

Yesterday's announcement by retailing giant Wal-Mart that it was acquiring Vudu, the on-demand movie service, generated a flurry of reactions from industry commentators. Some think it gives Wal-Mart the juice it needs to finally be a major digital media player. Others believe that Wal-Mart's miserable record in digital media suggests that the deal will be much ado about nothing. I'm in the latter camp, but not because of Wal-Mart's track record, but rather because of Vudu's own shortcomings.

Vudu's problem is that its value proposition is hamstrung by both the deals the Hollywood studios insist on to give Vudu access to their titles and by the current state of technology. Each of Vudu's 2 movie delivery

models - rental and download-to-own - has its own problems that severely curtail its consumer appeal. No matter how slick the service looks or how many CE devices it's embedded in, consumers will readily see these drawbacks and resist embracing Vudu.

models - rental and download-to-own - has its own problems that severely curtail its consumer appeal. No matter how slick the service looks or how many CE devices it's embedded in, consumers will readily see these drawbacks and resist embracing Vudu.The rental model is primarily handicapped by the ongoing provision that the rental period "expires" 24 hours after the movie was started. That means that if real life (e.g. a crying child, a call from an old friend, a household emergency) interrupts the Vudu's users' planned viewing window, they're out of luck. It's an absurd restriction, but all online movie rentals are laboring under it. Then there's the provision that most new releases aren't available for rental until 30 days after they debut on DVD. This kind of delay doesn't mean as much for a subscription service like Netflix (which of course just agreed to a new 28-day "DVD sales window" with Warner Bros.), because it has a huge back catalog to offer. But for Vudu (and Redbox) these delays are very noticeable to users.

The download-to-own model is even more challenged. First off, tech-savvy and value-conscious consumers are increasingly focused on cost-effective rentals or subscriptions, not purchasing films. The demise of DVD sales is ample evidence of this. The idea of creating a movie "collection" in a fully on-demand world is already on the verge of seeming as archaic as creating a CD collection has been for a while. And with download-to-own prices of approximately $20, which are more than a DVD costs, consumers will be even more hesitant.

But the real killer for download-to-own is the technology limitations, more specifically the lack of portability and interoperability. Say you're actually inclined to own movies using Vudu. What do you do, download them to an external hard drive? And when you travel, do you lug that thing around with you? When you get to your destination, what device will actually let you play back your movie from your hard drive? The issues go on. The reality is that ubiquitous, cheap DVD players and the compact size of the discs themselves have created a very high bar for digital delivery to exceed. "Digital locker" concepts like DECE and Disney's KeyChest are desperately needed to move digital downloads along, but even they are just a part of a larger CE puzzle.

So, although the Vudu service is very impressive, with a slick user experience and really nice quality video, the reality is that unless Wal-Mart is able to break through these challenges, the Vudu service is going to be marginally attractive to consumers at best. That means the Wal-Mart acquisition, in fact, makes little difference.

Maybe Wal-Mart has the clout to move the studios, but given mighty Apple's own difficulties doing so, I'm skeptical that Wal-Mart will have better luck. I continue to believe that Netflix's model - which combines the full selection of DVDs with the convenience and growing selection of online delivery (including TV shows by the way) - is a far better approach. Netflix may not have all the HD and user interface bells and whistles that Vudu has, but it's a far better value proposition for consumers. This is partly why Netflix has doubled in size, to 12.3 million subscribers, in the last 3 years.

What do you think? Post a comment now (no sign-in required).

Categories: Deals & Financings, FIlms, Studios

Topics: Apple, DECE, Disney, KeyChest, Netflix, VUDU, Wal-Mart

-

Amazon VOD Now On Roku; Battle with Apple Looms Ahead

Amazon and Roku announced yesterday that Amazon's VOD service will soon be available on Roku's $99 Digital Video Player. The deal starts to make good on Roku CEO Anthony Woods's intentions about "opening up the platform to anyone who wants to put their video service on this box."

With Amazon VOD's 40,000+ TV programs and movies added to the 12,000 titles already available to Netflix subscribers via its Watch Instantly service (plus more content deals yet to come), little Roku is starting to look like a potentially important link in the evolving "over-the-top" video distribution value chain.

More interesting though, is that I think we're starting to see the battle lines drawn for supremacy in the download-to-own/download-to-rent premium video category between Amazon on one side and Apple on the other. Though Apple dominates this market today, having sold 200 million TV programs alone, there are ample reasons to believe competition is going to stiffen.

Apple is of course in the video download business for the same reasons it was in the music download business: to drive sales of the iPod and more recently - and to a lesser extent - the iPhone. According to the latest info I could find, iTunes now has 32,000+ TV programs and movies, including a growing number in

HD. For now that's slightly less than Amazon VOD, but my guess is that over time the two libraries will be virtually identical.

HD. For now that's slightly less than Amazon VOD, but my guess is that over time the two libraries will be virtually identical. While Apple has a near monopoly on portable viewing via the iPod and iPhone, it is a laggard in bridging broadband-to-the-TV. Its Apple TV device, introduced in January, 2007, and meant to give iTunes access on the TV, has been an underperformer. Certainly a detractor has been price, with the 40GB lower-end model still running $229. But more importantly, as an iTunes-only box, Apple TV perpetuates a closed, "walled-garden" paradigm that consumers are increasingly rejecting (as companies like Roku astutely understand).

For Amazon, the world's largest online retailer, video downloads are a rich growth market. The company brings significant advantages to the table, starting with tens of millions of existing customer relationships with credit cards or other payment options just waiting to be charged for video downloads. Amazon has strong brand name recognition and trust. And of course, it has a near-limitless ability to cross-promote downloads with DVDs and other products.

Determined not to be left behind in the great race to get broadband delivered video all the way to the TV, it has been integrating its VOD service with 3rd party devices like TiVo, Sony's Bravia Internet Video Link, Xbox 360 and Windows Media Center PCs. Its latest deal with Roku is far from its last.

Amazon VOD's adoption will benefit from the fact that there are many non-Amazon reasons that people will be buying these devices. For example, consider Roku, TiVo and Xbox 360. With Roku, Netflix is fueling sales. As Netflix subscribers realize that new releases are generally not available in Watch Instantly, but are through Amazon VOD on Roku, they'll be prone to give Amazon VOD a try (the Netflix limitation is course due to Hollywood's windowing, and another reason why I believe it's crucial for Netflix to make deals with broadcast networks for online distribution of their hit programs). For TiVo and Xbox 360, each has a well-defined value proposition for consumers to purchase. Amazon VOD's availability is a pure bonus for buyers.

Amazon VOD's adoption will benefit from the fact that there are many non-Amazon reasons that people will be buying these devices. For example, consider Roku, TiVo and Xbox 360. With Roku, Netflix is fueling sales. As Netflix subscribers realize that new releases are generally not available in Watch Instantly, but are through Amazon VOD on Roku, they'll be prone to give Amazon VOD a try (the Netflix limitation is course due to Hollywood's windowing, and another reason why I believe it's crucial for Netflix to make deals with broadcast networks for online distribution of their hit programs). For TiVo and Xbox 360, each has a well-defined value proposition for consumers to purchase. Amazon VOD's availability is a pure bonus for buyers.Still, Amazon VOD's Achilles heel that it is missing a portable playback companion on a par with the iPod and iPhone. Users clearly value portability and Amazon needs to solve this problem (hmm, can you say "Kindle for Video?"). Yet another issue is that despite its various 3rd party device deals, the user experience will always be governed by these devices' strengths and weaknesses. In this respect, Apple's ownership of the whole hardware/software/services ecosystem gives it significant user experience advantages (which of course it has masterfully exploited with iTunes/iPod).

Apple and Amazon hardly have the market to themselves though. Others like Microsoft Xbox LIVE, Vudu and Sezmi are vying for a place in the market. And then of course there are the VOD offerings from the cable/satellite/telco video service providers, who have big-time incumbency advantages. Not to be forgotten in all of this is consumer inertia around the robust DVD market, which to a large extent all of these video download options seek to supplant.

In the middle of all this are Joe and Jane Consumer - soon to be overwhelmed by a barrage of competing and confusing offers for how to get on-demand TV program and movie downloads in better, faster and cheaper ways. In this market, I believe simplicity, content choices, brand and especially price will determine the eventual winners and losers. These are front and center considerations for Amazon, Apple and all the others going forward.

What do you think? Post a comment now.

Categories: Aggregators, Devices, Downloads, FIlms, HD

Topics: Amazon, Apple, iTunes, Roku, SezMi, TiVo, VUDU, XBox

-

Reviewing My 6 Predictions for 2008

Back on December 16, 2007, I offered up 6 predictions for 2008. As the year winds down, it's fair to review them and see how my crystal ball performed. But before I do, a quick editorial note: each day next week I'm going to offer one of five predictions for the broadband video market in 2009. (You may detect the predictions getting increasingly bolder...that's by design to keep you coming back!)

Now a review of my '08 predictions:

1. Advertising business model gains further momentum

I saw '08 as a year in which the broadband ad model continued growing in importance as the paid model remained in the back seat, at least for now. I think that's pretty much been borne out. We've seen countless new video-oriented sites launch in '08. To be sure many of them are now scrambling to stay afloat in the current ad-crunched environment, and there will no doubt be a shakeout among these sites in '09. However, the basic premise, that users mainly expect free video, and that this is the way to grow adoption, is mostly conventional wisdom now.

The exception on the paid front continues to be iTunes, which announced in October that it has sold 200 million TV episode downloads to date. At $1.99 apiece, that would imply iTunes TV program downloads exceed all ad-supported video sites to date. The problem of course is once you get past iTunes things fall off quickly. Other entrants like Xbox Live, Amazon and Netflix are all making progress with paid approaches, but still the market is held back by at least 3 challenges: lack of mass broadband-to-the-TV connectivity, a robust incumbent DVD model, and limited online delivery rights. That means advertising is likely to dominate again in '09.

2. Brand marketers jump on broadband bandwagon

I expected that '08 would see more brands pursue direct-to-consumer broadband-centric campaigns. Sure enough, the year brought a variety of initiatives from a diverse range of companies like Shell, Nike, Ritz-Carlton, Lifestyles Condoms, Hellman's and many others.

What I didn't foresee was the more important emphasis that many brands would place on user-generated video contests. In '08 there were such contests from Baby Ruth, Dove, McDonald's, Klondike and many others. Coming up in early '09 is Doritos' splashy $1 million UGV Super Bowl contest, certain to put even more emphasis on these contests. I see no letup in '09.

3. Beijing Summer Olympics are a broadband blowout

I was very bullish on the opportunity for the '08 Summer Games to redefine how broadband coverage can add value to live sporting events. Anyone who experienced any of the Olympics online can certainly attest to the convenience broadband enabled (especially given the huge time zone difference to the U.S.), but without sacrificing any video quality. The staggering numbers certainly attested to their popularity.

Still, some analysts were chagrined by how little revenue the Olympics likely brought in for NBC. While I'm always in favor of optimizing revenues, I tried to take the longer view as I wrote here and here. The Olympics were a breakthrough technical and operational accomplishment which exposed millions of users to broadband's benefits. For now, that's sufficient reward.

4. 2008 is the "Year of the broadband presidential election"

With the '08 election already in full swing last December (remember the heated primaries?), broadband was already making its presence known. It only continued as the year and the election drama wore on. As I recently summarized, broadband was felt in many ways in this election cycle. President-elect Obama seems committed to continuing broadband's role with his weekly YouTube updates and behind-the-scenes clips. Still, as important as video was in the election, more important was the Internet's social media capabilities being harnessed for organizing and fundraising. Obama has set a high bar for future candidates to meet.

5. WGA Strike fuels broadband video proliferation

Here's one I overstated. Last December, I thought the WGA strike would accelerate interest in broadband as an alternative to traditional outlets. While it's fair to include initiatives like Joss Wheedon's Dr. Horrible and Strike.TV as directly resulting from the strike, the reality is that I believe there was very little embrace of broadband that can be traced directly to the strike (if I'm missing something here, please correct me). To be sure, lots of talent is dipping its toes into the broadband waters, but I think that's more attributable to the larger climate of interest, not the WGA strike specifically.

6. Broadband consumption remains on computers, but HD delivery proliferates

I suggested that "99.9% of users who start the year watching broadband video on their computers will end the year no closer to watching broadband video on their TVs." My guess is that's turned out to be right. If you totaled up all the Rokus, AppleTVs, Vudus, Xbox's accessing video and other broadband-to-the-TV devices, that would equal less than .1% of the 147 million U.S. Internet users who comScore says watched video online in October.

However, there are some positive signs of progress for '09. I've been particularly bullish on Netflix's recent moves (particularly with Xbox) and expect some other good efforts coming as well. It's unlikely that '09 will end with even 5% of the addressable broadband universe watching on their TVs, but even that would be a good start.

Meanwhile, HD had a banner year. Everyone from iTunes to Hulu to Xbox to many others embraced online HD delivery. As I mentioned here, there are times when I really do catch myself saying, "it's hard to believe this level of video quality is now available online." For sure HD will be more widely embraced in '09 and quality will get even better.

OK, that's it for '08. On Monday the focus turns to what to expect in '09.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, Brand Marketing, Devices, HD, Indie Video, Politics, Predictions, Sports, Technology, UGC

Topics: Amazon, Apple, AppleTV, Barack Obama, Hulu, iTunes, NBC, Netflix, Olympics, Roku, VUDU, XBox

-

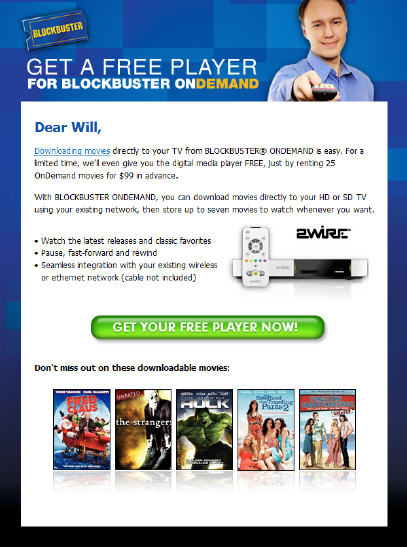

Blockbuster Online with New 2Wire MediaPoint Player Has a Tough Climb Ahead

Have you received the email pitch from Blockbuster Online yet, to rent 25 movies and get the new 2Wire MediaPoint Digital Media Player "free?" I've received a couple already this week (see below), and after reviewing the offer and its details, and comparing it to other alternatives, my conclusion is that the new service has a tough climb ahead.

The new 2Wire box itself is in the same general family as other single-purpose boxes such as AppleTV, Vudu and Netflix's Roku. There are some differences among them in hard drive size, pricing, outputs and streaming vs. downloading orientation. But they all serve the same basic purpose: connecting you via your home broadband connection to one source of "walled garden" premium-quality video content.

VideoNuze readers know I've been quite skeptical of the standalone box model, especially when box prices start in the $200-300 range. There's no question there's an upscale, early adopter audience that will buy in, but mainstream consumers will be uninterested for all kinds of reasons including: financial considerations (especially in this economy), resistance to connecting another box in already crowded consoles, perceived technical complexity, strong existing substitutes (e.g. cheap ubiquitous DVD players) and indistinct value propositions.

My judgment is based on a pretty simple set of criteria I rely on to gauge a new product or service's likelihood of success: Does it offer meaningful new value (some combination of better price, quality or speed) with minimal adoption effort required? Can a large target audience for this new value be clearly defined, served and acquired in an economically-reasonable manner? Is this new value attainable without sacrificing meaningful benefits of existing alternatives?

Miss on any one of these and the odds of success lengthen. Miss on any two and you're in long-shot territory. Miss on all three and you're dead on arrival. After evaluating the Blockbuster Online/MediaPoint current offer, my sense is that it misses on at least two and possibly all three.

Value: As explained below, for certain movies renters, the offer is valuable. It provides convenience at a relatively low financial commitment for the new device. But explaining these benefits just to the relevant target audience at an economic cost per acquisition is going to be nearly impossible. I'm dubious that even in-store promotions - which on the surface seem Blockbuster's strength - will work. First, there may be franchisee issues, as there were with previous "Total Access" promotions. And second, Blockbuster has closed so many stores in prime target neighborhoods - due to the rise of Netflix and other options eroding their business - that they'll be missing many prospects (example: in my upscale home town of Newton, MA there is not a single Blockbuster store left).

Audience: There's only one real target audience I can see for this offer, and it seems very narrow to me: low-volume renters of movies only, who are not iTunes users. Think about it - if you rent a lot of movies, you've likely been subscribing to Netflix for years (more so if you also rent TV shows). If you want to own your content instead of rent it, then you buy DVDs or maybe more recently have been buying digital version, most likely with iTunes primarily. If that's the case, then when it comes to watching on TV, you're going to buy an Apple TV (even then, few have done so to date), not a 2Wire MediaPoint. The eligible target audience left for Blockbuster/MediaPoint seems pretty slim.

Sacrificing existing benefits: Inevitably all digital distribution options need to be compared to the incumbent DVD format, which is remarkably strong (no wonder a billion units have been shipped to date). Against the DVD standard, Blockbuster/MediaPoint is inferior in a number of ways: limited viewing windows (the usual online limitations of 24 hour expiration after starting, and 30 day automatic file deletion), no portability to view rented movies on other TVs not connected to a MediaPoint, no TV shows available for rent, and at this point, smallish storage that only keeps up to 5 movies at a time.

Add it all up, and it's a pretty daunting set of issues. To be sure, much of this isn't specific to Blockbuster. To succeed, all new digital delivery options must be mindful of the above criteria as well.

What do you think? Post a comment now.

Categories: Aggregators, Devices

Topics: 2Wire, AppleTV, Blockbuster, Netflix, VUDU

-

Video is the Killer App Driving Coming Bandwidth Explosion

A short interview in Multichannel News with Rouzbeh Yassini before the Thanksgiving break last week caught my eye.

Rouzbeh's name is likely unfamiliar to many of you. But for others who have been in and around the cable and broadband industries since the '90s, he is semi-famous. In those days Rouzbeh ran a company called LANCity, which was a pioneer in designing and manufacturing cable modems. These of course are the devices that now reside in tens of millions of homes around the world, enabling broadband Internet access and the high-quality video services like YouTube, Hulu, iTunes and others that run through them.

Though it's only been about 15 years, the early-to-mid '90s seem like another age entirely. Can you remember dial-up Internet access? Busying up your phone line if you wanted to be online? Listening to all those weird tones as your creaky 56K modem connected you to Prodigy, CompuServe, AOL, or eventually this thing everyone seemed to be talking about called the "World Wide Web?"

In my opinion, Rouzbeh deserves as much credit as anyone for the transformation of the dial-up Internet era

to the broadband world we now enjoy. He played a crucial role in articulating broadband's business potential to scores of senior cable executives who barely knew what a computer was, much less this new-fangled thing called the Internet. Importantly, he was a key technical architect of modern cable networks, which today barely resemble the passive, one-way networks of old.

to the broadband world we now enjoy. He played a crucial role in articulating broadband's business potential to scores of senior cable executives who barely knew what a computer was, much less this new-fangled thing called the Internet. Importantly, he was a key technical architect of modern cable networks, which today barely resemble the passive, one-way networks of old. In short, I've learned to take notice of Rouzbeh's prognostications. Though he can be irrepressibly optimistic, he's directionally right more often than not.

All of that brings me to his Multichannel interview. Rouzbeh now envisions the era of gigabit or 1,000 megabit Internet access within a decade. To put this in perspective, today's cable modems typically deliver around 10 megabit service or 1% of a gigabit. Spurred by competitive pressures, Comcast has recently announced the rollout of 50 megabit service to certain regions, with expansion to its entire footprint by 2010. These new rollouts are part of the cable industry's "DOCSIS 3.0" standards, covering a new generation of modems and channel management techniques.

There's an axiom in the broadband industry that usage always rises to the level of bandwidth provided. Yet when we're talking 1 gigabit service, one has to rightly ask, "what in the world are people going to do with all that bandwidth?" Rouzbeh posits things like corporate networking, remote offices, medical services and the like, but only touches briefly on video delivery.

From my perspective, video is the killer application that will drive this bandwidth explosion. As I wrote recently in "Video Quality Keeps Improving - What's it All Mean?" we are on the front end of a shift toward dramatically higher video quality, with near HD delivery already becoming common (Hulu, Netflix and Vudu are among the most recent to announce HD initiatives). This shift will only accelerate going forward. And to accommodate it will require lots more bandwidth from network providers.

In reality, the trickiest part of bandwidth expansion is less the technology development and deployment and more the business models that support the investments and make the most strategic sense. Questions abound: Is the right model to charge $150/mo for 50 megabit access as Comcast plans? Or to build a content service available only to those high-powered users? Or act like a CDN and provide services so as to charge content providers themselves to deliver higher-quality video? Maybe some hybrid of these, or some other model? And of course, what impact do these models have on the incumbent multichannel subscription video offering?

While there's murkiness now, like Rouzbeh, I'm a big believer that these things will ultimately be worked out and that bandwidth expansion is inevitable. Just as we now look back on the dial-up era and wonder how we got by, eventually we'll look at the mid-to-late 2000s and wonder how we survived on so little bandwidth.

What do you think? Post a comment now.

Categories: Aggregators, Broadband ISPs, Cable TV Operators, People

Topics: Comcast, DOCSIS, Hulu, Netflix, VUDU

-

Cutting the Cord on Cable: For Most of Us It's Not Happening Any Time Soon

Two questions I like to ask when I speak to industry groups are, "Raise your hand if you'd be interested in 'cutting the cord' on your cable TV/satellite/telco video service and instead get your TV via broadband only?" and then, "Do you intend to actually cut your cord any time soon?" Invariably, lots of hands go up to the first question and virtually none to the second. (As an experiment, ask yourself these two questions.)

I thought of these questions over the weekend when I was catching up on some news items recently posted to VideoNuze. One, from the WSJ, "Turn On, Tune Out, Click Here" from Oct 3rd, offered a couple examples of individuals who have indeed cut the cord on cable and how their TV viewing has changed. My guess is that it wasn't easy to find actual cord-cutters to be profiled.

There are 2 key reasons for this. First it's very difficult to watch broadband video on your TV. There are special purpose boxes (e.g. AppleTV, Vudu, Roku, etc.), but these mainly give access to walled gardens of pre-selected content, that is always for pay. Other devices like Internet-enabled TVs, Xbox 360s and others offer more selection, but are not really mass adoption solutions. Some day most of us will have broadband to the TV; there are just too many companies, with far too much incentive, working on this. But in the short term, this number will remain small.

The second reason is programming availability. Potential cord-cutters must explicitly know that if they cut their cord they'll still be able to easily access their favorite programs. Broadcasters have wholeheartedly embraced online distribution, giving online access to nearly all their prime-time programs. While that's a positive step, the real issue is that cord-cutters would get only a smattering of their favorite cable programs. Since cable viewing is now at least 50% of all TV viewing (and becoming higher quality all the time, as evidenced by cable's recent Emmy success), this is a real problem.

To be sure, many of the biggest ad-supported cable networks (MTV, USA, Lifetime, Discovery) are now making full episodes of some of their programs available on their own web sites. But these sites are often a hodgepodge of programming, and there's no explanation offered for why some programs are available while others are not. For example, if you cut the cord and could no longer get Discovery Channel via cable/satellite/telco, you'd only find one program, "Smash Lab" available at Discovery.com. Not an appealing prospect for Discovery fans.

Then there's the problem of navigation and ease of access. Cutting the cord doesn't mean viewers don't want some type of aggregator to bring their favorite programming together in an easy-to-use experience. Yet full streaming episodes are almost never licensed to today's broadband aggregators. Cable networks are rightfully being cautious about offering full episodes online to aggregators not willing to pay standard carriage fees.

For example, even at Hulu, arguably the best aggregator of premium programming around, you can find Comedy Central's "The Daily Show" and "Colbert Report." But aside from a few current episodes from FX, SciFi and Fuel plus a couple delayed episodes from USA like "Monk" and "Psych," there's no top cable programming to be found.

As another data point, I checked the last few weeks of Nielsen's 20 top-rated cable programs and little of this programming is available online either. A key gap for cord-cutters would be sports. At a minimum, they'd be saying goodbye to the baseball playoffs (on TBS) and Monday Night football (on ESPN). In reality, sports is the strongest long-term firewall against broadband-only viewing as the economics of big league coverage all but mandate carriage fees from today's distributors to make sense.

Add it all up and while many may think it's attractive to go broadband only, I see this as a viable option for only a small percentage of mainstream viewers. Only when open broadband to the TV happens big time and if/when cable networks offer more selection will this change.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks, Cable TV Operators, Devices, Telcos

Topics: AppleTV, Comedy Central, Discovery, ESPN, FX, Hulu, Lifetime, Roku, SciFi, TBS, USA, VUDU, Xbox360

-

Online Movie Delivery Advances, Big Hurdles Still Loom

Online movie delivery is back in the news, but dramatic change is still well down the road in this space as usability, rights issues and incumbent business models/consumer behaviors pose formidable hurdles.

Yesterday Netflix announced a $99 appliance with Roku, enabling the company's "Watch Instantly" streaming service on TVs. That news follows Apple's deals with a number of big studios in early May obtaining "day-and-date" access to current titles. And today brings news that Bell Canada, that country's largest telco, is formally launching its Bell Video Store, also providing day-and-date delivery, of Paramount titles to start (and soon others), plus portable viewing on Archos devices.

Netflix, which I last wrote about here, took a shot across the bow of Apple TV and Vudu by introducing the

Roku box, the lowest-priced broadband movies appliance yet. Apples-to-apples comparisons aren't fair as the stripped-down Netflix/Roku box doesn't have a hard-drive or equivalent processing. That inevitably means lower quality delivery vs. locally-stored content with the others, plus uncertainty about HD-delivery. Netflix/Roku's big advantage is that it's a value-add service for current Netflix subscribers, meaning no new fees as with the Apple TV/Vudu approaches.

Roku box, the lowest-priced broadband movies appliance yet. Apples-to-apples comparisons aren't fair as the stripped-down Netflix/Roku box doesn't have a hard-drive or equivalent processing. That inevitably means lower quality delivery vs. locally-stored content with the others, plus uncertainty about HD-delivery. Netflix/Roku's big advantage is that it's a value-add service for current Netflix subscribers, meaning no new fees as with the Apple TV/Vudu approaches.However, Watch Instantly has older titles and amounts to less than 10% of Netflix's total catalog. I don't see that changing much; Watch Instantly runs smack into studios' incumbent windowing approach and deals with HBO, Showtime and Starz for premium TV. Netflix's model is built on the home video window, so new online delivery rights must be obtained which will be a tough road. However, with Paramount, MGM, Lionsgate and others splintering from Showtime recently to set up their own premium channel, it's possible that some studios' rights may loosen up, but of course at a price.

Still, I don't see the Netflix/Roku box breaking 10% penetration of Netflix's sub base any time soon, barring a box giveaway. Enlarging the value proposition by licensing the Roku technology for inclusion in other devices (e.g. Blu-ray) could also help drive adoption.

Meanwhile, today Bell Canada is announcing the formal launch of its Bell Video Store. In beta since late '07,

it offers 1,500 titles, now including day-and-date delivery from Paramount (and others soon according to Michael Freeman, Bell's director of product management who I spoke to yesterday). This is noteworthy, as it appears to be the first time a service provider has received day-and-date online access from any studio. If other providers follow suit we may finally witness some internal competition with sacrosanct-to-date Video on Demand initiatives.

it offers 1,500 titles, now including day-and-date delivery from Paramount (and others soon according to Michael Freeman, Bell's director of product management who I spoke to yesterday). This is noteworthy, as it appears to be the first time a service provider has received day-and-date online access from any studio. If other providers follow suit we may finally witness some internal competition with sacrosanct-to-date Video on Demand initiatives.By using ExtendMedia's platform, Bell is also enabling downloads-to-own directly to Archos portable devices. With a couple million satellite homes and fiber IPTV fiber-based deployments continuing, there are multiple three screen options looming for Bell. Yet for now these are limited. Michael confirmed Bell has no plans to offer a branded movie appliance a la Netflix/Roku, meaning it will dependent on XBoxes and other PC-TV bridge devices.

Renewed progress and experimentation are welcome in this space, but lots of hard work remains for online movie delivery to become mainstream.

What do you think of the online movie delivery space? Post a comment now!

Categories: Aggregators, Cable Networks, Devices, Downloads, FIlms, Studios

Topics: Apple, Bell Canada, HBO, Netflix, Paramount, Roku, Showtime, Starz, VUDU

-

YouTube: "Over-the-Top's" Best Friend

The announcement a couple of weeks ago that YouTube was partnering with TiVo got me to thinking that YouTube is probably the best friend that so called "over-the-top" or "cable bypass" aspirants could have.

As a quick refresher, "over-the-top" and "cable bypass" refer to the emerging category of devices and service providers seeking to bring broadband video to the consumer's TV, but without the involvement of existing video providers such as cable and satellite. Some of these efforts (Apple TV, Vudu and Internet-enabled TVs) are positioned as augmenting incumbent providers, while some (Building B, others) are meant to compete directly.

Today's players share the common trait of being closed, "walled gardens," offering only certain content that they select. This contrasts with the open Internet/broadband model, where users are able to access any content they choose. Many of you know that I have been a strong proponent that open is the winning competitive path for aspiring over-the-top players.

If the over-the-top crowd adopts the open approach, YouTube is their perfect ally; it is the best-known brand name in broadband video, has the largest library of both user-generated and increasingly premium

video and has huge loyalty. Positioned properly it could be a killer value proposition for over-the-top players. I've previously argued that Apple missed the boat by not adopting this positioning for Apple TV.

video and has huge loyalty. Positioned properly it could be a killer value proposition for over-the-top players. I've previously argued that Apple missed the boat by not adopting this positioning for Apple TV.I talked last week with David Eun, VP of content partnerships at Google and Chris Maxcy, head of biz dev for YouTube, and they both made clear that the goal is to morph YouTube from a consumer destination site to a full-fledged video platform distributing video everywhere - devices, mobile, web sites, others. To this end, YouTube recently published an expanded set of APIs to allow 3rd parties to gain easier access to YouTube's content. This of course is great news for over-the-top devices, who should have considerable flexibility for how to incorporate YouTube into their offering. For now TiVo is leading the way in offering YouTube, albeit to a very small audience.

If you were wondering whether YouTube or Google itself will enter the device business, that seems unlikely. David and Chris were clear in saying that devices are not their core competency, and they'll leave it to others to decide how to implement the YouTube APIs and create and test various user experiences. Meanwhile with more premium content flowing into YouTube, its value as an over-the-top partner only increases.

What do you think? Post a comment!

Categories: Aggregators, Devices

Topics: Apple, Apple TV, Google, TiVo, VUDU, YouTube

-

Vudu Cuts Price

Some of you may have noticed that Vudu announced last Thursday that it was cutting the price of its box by over $100 to $295. I recently wrote about Vudu in "Apple TV Improves, Vudu in its Crosshairs." Looks like it didn't take long for Vudu to start feeling Apple's heat. It's a good move, but I still remain skeptical about this box's mass appeal.

Categories: Devices

Posts for 'VUDU'

| Next

Connect with VideoNuze

Exclusive News Roundup

- Peacock Brings Starz to the Platform as First-Ever Add-On Subscription CNET

- Willy Wonka Competition Show at Netflix Uses AI to Re-Create Gene Wilder’s Voice The Hollywood Reporter

- Peacock Ad-Free Tier Launches On YouTube Primetime Channels As Part Of 2025 Distribution Deal Deadline

- Microdramas, Often Dismissed as Lowbrow Curiosities, Eye the Mainstream NY Times

- YouTube Shorts are getting even shorter with an update that lets you double the playback speed TechCrunch

- TikTok and YouTube are reinventing sports viewership. Broadcasters are taking note CNBC