-

Online/Mobile Video's Top 10 of 2010

2010 was another spectacular year of growth and innovation in online and mobile video, so it's no easy feat to choose the 10 most significant things that happened during the year. However, I've taken my best shot below, and offered explanations. No doubt I've forgotten a few things, but I think it's a pretty solid list. As much as happened in 2010 though, I expect even more next year, with plenty of surprises.

My top 10 are as follows:

Categories: Advertising, Aggregators, Broadband ISPs, Broadcasters, Cable Networks, Cable TV Operators, Deals & Financings, Devices, Mobile Video, Regulation, Satellite, Technology, Telcos

Topics: 4G, Android, Apple, Google TV, iPad, Net Neutrality, Netflix, YouTube

-

5 Items of Interest for the Week of Dec. 12th

Happy Friday. Once again I'm pleased to offer VideoNuze's end-of-week feature analyzing 5-6 interesting online/mobile video industry news items from the week that we didn't have a chance to cover previously. This week I'm changing the format a little bit, creating an individual post for each item. I'm doing this in response to reader interest in being able to share individual items (not the whole group) more easily. Let me know what you think of the new format. Here they are:

1. Potential YouTube-Next New Networks deal is a bit of a head-scratcher

2. Here's a great example of why TV Everywhere matters so much to the pay-TV industry

3. Hulu's Kilar: "Hulu Plus now a material portion" of revenues

4. Google not ready to announce fiber winning communities

5. Tiffany shows online video works for luxury retailers

Read them now or check them out this weekend!Categories: Aggregators, Broadband ISPs, Cable Networks, Cable TV Operators, Commerce, Deals & Financings, Indie Video, Satellite, Telcos

Topics: Google, Hulu Plus, Netflix, Next New Networks, Tiffany, YouTube

-

Here's A Great Example of Why TV Everywhere Matters So Much To the Pay-TV Industry

Want a really tangible example of why TV Everywhere is so critical to the pay-TV industry? Then have a look at this post from industry banker Ken Sonenclar, who recounts his personal experience of trying to find an online version of the season finale of Showtime's "Dexter" on an evening when bad weather knocked out his satellite dish. Frustrated that he couldn't find the episode available anywhere, he ultimately stumbled upon a pirate site and happily watched the episode, albeit at somewhat lower quality.

Experiences like these no doubt play out daily as pay-TV subscribers seek convenient, on-demand access to their favorite programs. The TV Everywhere model works because it still requires a valid paid subscription, so the current monetization model is unharmed. But the incremental value to viewers is substantial. With services like Netflix and Hulu Plus increasingly available on every conceivable online and mobile device, consumers' expectations are being raised. If the pay-TV industry (both operators and networks) can't meet or exceed the experiences that a sub $10/mo service can deliver, then they shouldn't be surprised when subscribers begin dropping their expensive pay-TV services.Categories: Cable Networks, Cable TV Operators, Satellite, Telcos

Topics: TV Everywhere

-

6 Key 2011 Trends in Online and Mobile Video

Yesterday Colin Dixon from The Diffusion Group and I presented a webinar describing our 6 key trends for 2011 in online and mobile video. Colin is one of the sharpest analysts of the pay-TV and online/mobile video industries and we had no shortage of ideas to sort through. Our list is a joint effort, and during the webinar we each presented the 3 trends we felt the strongest about. In today's post I share and explain each one. At the end of the webinar we conducted a poll asking attendees whether they agreed or disagreed with our predictions. I've noted those results in bold font. If you want to download the slides and/or hear more of our detailed discussion, just register for the on-demand version of the webinar and you'll be emailed a link.

Categories: Aggregators, Broadband ISPs, Cable TV Operators, Mobile Video, Predictions, Regulation, Satellite, Technology, Telcos

Topics: FCC, Google, Net Neutrality, Netflix, TV Everywhere

-

Are Live Sports Pay-TV's Firewall or Its Albatross?

I've long assumed that live sports carried on cable TV networks (e.g. ESPN, Fox Sports, TNT, TBS, NFL Network, regional sports networks, etc.) would be a key firewall against cord-cutting since the games they air are unavailable online. In other words, if you're a sports fan, dropping your pay-TV subscription would be unthinkable. While I still believe that's mostly true, recently I've started wondering if it's possible that sports actually may also be an albatross for pay-TV operators, limiting their ability to effectively compete with online-only alternatives.

I use the word albatross because pay-TV providers actually have very little flexibility to offer non-sports fans lower-priced packages that don't include sports-oriented channels. In fact, the most surprising aspect of last week's announcement by Time Warner Cable of a new lower-priced tier called "TV Essentials" it's testing is that it will exclude ESPN, which is virtually unheard-of in pay-TV packaging. Because the underlying deals that cable networks have with sports leagues and rights-holders are so expensive, the networks try to get carried on the most popular pay-TV service tiers, thereby ensuring the highest number of subscriber homes (basic cable networks are paid by distributors on a per subscriber basis, so the more subscriber homes, the higher their revenue).

Categories: Cable Networks, Cable TV Operators, Satellite, Sports, Telcos

Topics: ESPN, Fox Sports, NFL Network, TBS, Time Warner Cable, TNT

-

How About Some Actual Data in the Cord-Cutting Debate?

No sooner did SNL Kagan's press release, announcing that the U.S. pay-TV industry had lost 119K subscribers in Q3 '10, following a loss of 216K subscribers in Q2, hit the wire today, than the blogosphere was alight with a fresh round of posts that cord-cutting was to blame. This chorus was surely egged on by Kagan senior analyst Ian Olgeirson's remark in the press release that "it is becoming increasingly difficult to dismiss the impact of over-the-top substitution on video subscriber performance." That remark was a notable change of tone from Kagan's Q2 release which ascribed subscriber losses solely to the country's ongoing economic woes.

Note however that Olgeirson only offered his opinion, rather than any actual, hard data from Kagan about cord-cutting's impact. That is characteristic of both sides of the current cord-cutting debate - lots of opining, but little-to-no reliable data. In my own Q3 analysis - in which I suggested that the pay-TV as a whole likely lost around 97K subscribers in Q3 (though the group of 8 of the top 9 pay-TV operators actually gained subscribers) - I noted that nobody truly knows the impact of cord-cutting, yet anyway.

Categories: Cable TV Operators, Satellite, Telcos

Topics: SNL Kagan

-

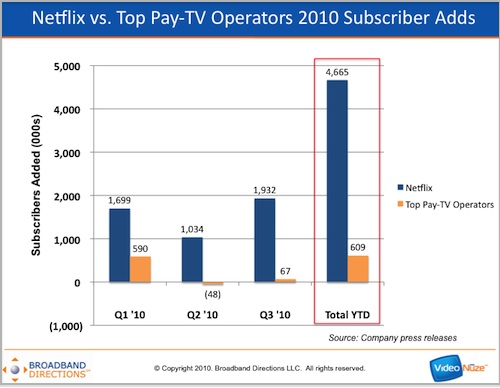

Netflix Has Added 8 Times As Many Subscribers in 2010 As Top Pay-TV Operators, Combined

Here's a pretty amazing factoid to end your week: in 2010 Netflix has added nearly 8 times as many subscribers as 8 of the top 9 pay-TV operators have, combined (#3 cable operator Cox is private and doesn't report). In the first 3 quarters of 2010, Netflix has added nearly 4.7 million subscribers while the top pay-TV operators have gained 609K.

Breaking down the pay-TV industry net gain further, the 2 main telcos (Verizon and AT&T) have added over 1.2 million subscribers and the 2 main satellite providers (DirecTV and DISH) have added 563K, while the top 4 reporting cable operators (Comcast, Time Warner Cable, Charter and Cablevision) have lost over 1.1 million.

Categories: Aggregators, Cable TV Operators, Satellite, Telcos

Topics: AT&T, Cablevision, Charter, Comcast, Cox, DirecTV, DISH, Netflix, Time Warner Cable, Verizon

-

Top U.S. Pay-TV Operators Post Narrow Subscriber Gains in Q3, Rebounding From Q2 Loss

Eight out of the nine largest U.S. pay-TV operators have reported their Q3 '10 results, gaining a slim 66,700 video subscribers, a rebound from a loss of 47,600 subscribers in Q2 '10. The Q2 loss was the first on record for the industry and fueled speculation that "cord-cutting" due to adoption of Internet-delivered video alternatives was rising. With only mildly positive subscriber adds - and 5 of the top 8 operators actually losing subscribers in Q3 - fears that cord-cutting is rising will surely accelerate.

The 8 operators (privately-held Cox Cable, the 3rd-largest cable operator does not disclose its results) represent more than 85% of all U.S. pay-TV households. Though they collectively showed a quarterly gain, if Cox and other cable operators lost subscribers at a comparable rate as the 4 large cable operators in the top 8 (Comcast, Time Warner Cable, Charter and Cablevision), the industry as a whole would have actually lost about 97K subscribers in the 3rd quarter.

Categories: Cable TV Operators, Satellite, Telcos

Topics: AT&T, Cablevision, Charter, Comcast, Cox, DirecTV, DISH, Netflix, Time Warner Cable, Verizon

-

Cable's Original Programs Should Be A Bulwark Against Cord-Cutting

A WSJ article today, "TV's Alternate Universe," about the proliferation and inventiveness of basic cable programs, provides an unintentional reminder of the value these shows have as a bulwark against cord-cutting. The article points out that basic networks will spend $23 billion this year on 1,462 originals, up from $14 billion on 863 shows just 5 years ago. The fact that these shows are both finding an audience and that they are virtually unavailable for free online makes them highly strategic assets as the pay-TV industry is increasingly buffeted by over-the-top video competition.

Two years ago, in "Cutting the Cord on Cable: For Most of Us It's Not Happening Any Time Soon," I argued that there are 2 key reasons mass-scale cord-cutting was unlikely, at least in the short term: first, the difficulty of watching online-delivered video on TVs (instead of on computers) limited its appeal as a substitute for pay-TV service for mainstream consumers, and second, the loss of numerous popular cable entertainment programs resulting from cord-cutting would give many people pause.

Categories: Cable Networks, Cable TV Operators, Satellite, Telcos

Topics: AMC, FX, Lifetime, Spike TV, TNT, TV Land, USA

-

For Pay-TV Operators, Will TV Everywhere Be TV Nowhere?

I continue to be confounded by the fact that the pay-TV industry - both operators and cable TV networks - have not made more progress on TV Everywhere, their most important competitive initiative in the online era. Yesterday I got yet another dose of this sobering reality watching a panel discussion at ScreenPlays magazine's Media Innovations Summit in LA. The panel included Synacor's Ted May, Starz's John Penney, EPIX's Emil Rensing, thePlatform's Marty Roberts and AT&T's Dan York and was moderated by Marketing/PR executive Bob Gold.

It's not that industry executives can't articulate the value to both operators and networks. For pay-TV operators, it's providing increased value to paying subscribers, which helps both acquisition and retention efforts. For cable networks, its expanded audience reach and advertising, while maintaining their hybrid model of paid distribution and advertising. For both it's staying competitive by providing access to premium content for consumers when, how and where they want it.

Categories: Cable Networks, Cable TV Operators, Satellite, Telcos

Topics: AT&T, EPIX, Starz, Synacor, thePlatform

-

Time Warner's "Premium Video-on-Demand" Experiment is a Blind Alley

Talk about an initiative that flies in the face of all prevailing sentiment: Time Warner is moving forward on testing a new window for early-release movies on VOD priced at $20-30 apiece in 2011, according to comments its CFO John Martin made yesterday at the Goldman Sachs conference. Never mind the wrath the idea will stir up among movie theater owners whose traditional windows get cannibalized as a consequence (Disney learned about that with its "Alice in Wonderland" early DVD release experiment last February), the real issue is that pay-TV operators should deem the idea a non-starter.

wrath the idea will stir up among movie theater owners whose traditional windows get cannibalized as a consequence (Disney learned about that with its "Alice in Wonderland" early DVD release experiment last February), the real issue is that pay-TV operators should deem the idea a non-starter.

Typical VOD rental rates of $4-5 already look expensive to consumers compared to Netflix's $9 all-you-can-eat monthly plans and Redbox's $1 DVD rentals. And while there are scenarios where getting a group or family together to watch a movie makes sense, it's getting harder than ever to do so. The reality is that families are atomizing to their individual activities; perusing or playing on Facebook, watching YouTube/Hulu/Netflix/etc., playing with the Wii or Farmville, chatting on Skype, shopping on Amazon, etc. Corralling this crowd and getting them to agree on any one movie is already a challenge; the prospect of paying $20-30 for the pleasure just sets the bar that much higher.

Categories: Cable TV Operators, FIlms, Satellite, Studios, Telcos

Topics: Disney, Netflix, Redbox, Time Warner, Time Warner Cable

-

Are Pay-TV Providers Getting Hit By a Perfect Storm in Q3?

The U.S. pay-TV industry, which as a whole lost multichannel video subscribers for the first time in Q2 '10, may be heading for a soft 3rd quarter as well. As Multichannel News reported yesterday, Time Warner Cable's CFO Rob Marcus said at a conference this week that Q3 "video net losses are pacing ahead" of where they were in Q3 '09. He attributed the downturn to recession-related factors of high unemployment, high home vacancy rates and slow new home formation. Though that's a fair explanation, it's only one element in a perfect storm pay-TV operators now find themselves battling.

Aside from the above recession-related matters, pay-TV operators are also up against belt-tightening that's rooted in basic household economics. As Craig Moffett at Sanford Bernstein pointed out in a note last weekend, in the past 25 years, cable and satellite spending has increased from 1/2 of 1% of discretionary spending to 1.4%, a growth rate that's triple other household discretionary line items.

Categories: Cable TV Operators, Satellite, Telcos

Topics: Sanford Bernstein, Time Warner Cable

-

5 News Items of Interest for the Week of Aug 23rd

Following is the latest update to VideoNuze's new Friday feature, highlighting 5-6 of the most intriguing industry news items from the week that VideoNuze wasn't able to cover.

Ads skipped by 86% of TV viewers, but TV ads still most memorable

A new Deloitte survey unsurprisingly finds high rates of ad skipping among DVR users watching time-shifted programs, yet also notes that 52% of respondents say TV advertising is more memorable than any other type (only 2% cited online video advertising). Is there a love-hate relationship with good old TV advertising?

Endemol USA Plans Kobe Bryant Web Series

Online video continues attracting celebrities, with the latest being LA Laker star Kobe Bryant, who will be featured in 8 episodes teaching Filipino kids about hoops. The series is being produced and promoted by powerhouse Endemol. More evidence that independent online video is gaining.

NFL Sunday Ticket To-Go, Without DirecTV

DirecTV unbundles its popular NFL package, selling online access to non-subscribers for $350. It's not clear there will be many takers at this price point, but it does raise interesting possibilities about unbundled subscribers connecting to their TVs and also how sports will be impacted by online and mobile viewing.

TiVo Launches Remote with Slide-Out Keyboard

TiVo is enhancing navigation with a long-awaited keyboard that slides out of its standard-shaped remote control for $90. With TiVo's new Premiere box offering more video choices than ever, quicker navigation is required. As other connected devices hit the market, it will be interesting to see what clever solutions they come up with too.

MTVN's Greg Clayman Heads to News Corp to Lead iPad Newspaper

Amid the ongoing shuffle of digital media executives, MTV Networks lost a key leader in Greg Clayman, who's moving to News Corp to head up their new iPad newspaper. Greg's been on VideoSchmooze panels and we've done webinars together; he always brings great insights as well as a terrific sense of humor.Categories: Advertising, Cable Networks, Devices, Indie Video, People, Satellite, Sports

Topics: Deloitte, DirecTV, Endemol USA, MTV, News Corp, NFL, TiVo

-

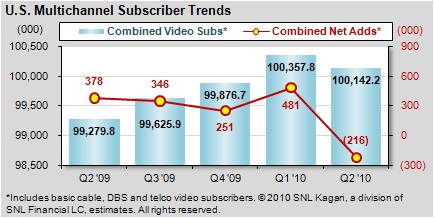

Pay-TV Industry Loses Subscribers in Q2 '10 For First Time Ever; Cable Bears Brunt

Research firm SNL Kagan is reporting today that the U.S. pay-TV industry (cable/satellite/telco) lost 216,000 multichannel TV subscribers in Q2 '10, the first time the industry as a whole has lost subscribers. Cable operators bore the brunt of the losses, dropping 711,000 subscribers, with Kagan saying 6 of the 8 operators reporting suffered record quarterly losses. By contrast, telcos added 414,000 subs in the quarter and satellite providers gained 81,000. The losses leave cable's industry share at 61%, down from 63.6% a year ago.

Kagan analyst Mariam Rondeli ascribed the quarterly losses to low housing formation and high unemployment due to the ongoing recession, coupled with churn due to promotions from last year's broadcast digital transitions expiring. Rondeli pointed out that over-the-top video alternatives were not the cause. By comparison, the pay-TV gained 378,000 subscribers in Q2 '09, meaning there was a swing of 594,000 subscribers year-over-year. U.S. Pay-TV providers as a whole ended Q2 '10 with 100.1 million subscribers.

Looking ahead, I've heard some murmurs that Q3 '10 could be softer than in prior years, again partially due to the recession, but also because seasonal college students' subscriptions may be reduced due to over-the-top alternatives. While we've yet to see any tangible evidence of cord-cutting, the first impact may simply be slower multichannel sign-ups from younger users more accustomed to watching online. We'll see.

What do you think? Post a comment now (no sign-in required).Categories: Cable TV Operators, Satellite, Telcos

Topics: SNL Kagan

-

NY Times Gives Online Video High-Profile Coverage With Today's "Sofa Wars" Series

More evidence that online video has gone mainstream, as the NY Times is running a series today, dubbed "The Sofa Wars," includes half a dozen articles looking at online video's incursion into the living room. Included in the series are articles on cord-cutting (or the lack thereof), Sony's bet on Crackle, the range of connected devices vying for market share, the role of 3D in selling TVs and Dish Network's new online initiatives.

The Times' coverage further underscores how online video has burst into the public consciousness in the past few years. In the pre-YouTube era (before 2005), online video was still a fringe activity for people willing to hunt around for valuable video and suffer through often sub-optimal delivery quality. Now, as comScore reports each month, online video is watched by the vast majority of Internet users. It's becoming as common as sending an email. With connected devices proliferating to bring online video to TVs, what additional consumer behavior changes can we expect over the next 5 years?

What do you think? Post a comment now (no sign-in required).Categories: Devices, Indie Video, Satellite

Topics: NY Times

-

TV Everywhere On Track for 30-50 Million Homes By End of 2010: Turner Exec

TV Everywhere services will be available to 30-50 million U.S. homes by the end of this year, according to Jeremy Legg, SVP of Business Development and Multi-Platform Distribution at Turner Broadcasting whom I spoke to last week. Jeremy characterized the 30 million number as "realistic" and 50 million as "plausible." Turner is part of Time Warner, which has been the most significant proponent among content providers of TV Everywhere services; Jeremy is the point person at Turner for its efforts.

I've thought TV Everywhere was a smart concept since it was unveiled last summer, in a high-profile news conference with Time Warner's CEO Jeff Bewkes and Comcast's CEO Brian Roberts. Since then though, pay-TV distributors in the U.S. have been relatively quiet about their TV Everywhere rollout milestones, leading me to grow skeptical about whether they're putting enough muscle behind their efforts. As I argued recently, the stakes for TV Everywhere success have grown considerably as Netflix in particular has ramped up its online offerings, getting closer and closer to pay-TV players' traditional turf.

Categories: Cable Networks, Cable TV Operators, Satellite, Telcos

-

5 News Items of Interest for the Week of Aug 2nd

In addition to producing daily original analyses focused on the evolution of the online/mobile video industry, another key element of VideoNuze is collecting and curating links to industry coverage from around the web. Each week there are typically 30-40 stories that VideoNuze aggregates in its exclusive news roundup. Many readers have come to depend on this curated news collection to ensure they're always up to speed.

Now, to take news curation up another level, on Fridays I'm going to test out highlighting 5-6 of the most intriguing news items of the week. In case you missed VideoNuze for a day or two during the week, you can check in on Friday to see the these top 5-6 industry stories of the week, some of which VideoNuze may have covered itself. Synopses and implications are noted. Enjoy and let me know your reactions!

Wired to Produce Short Films For iPad

The tech magazine recruits Will Ferrell for four short videos that lampoon inventions that failed to take off. Exclusively for its iPad app. More evidence of print pub capitalizing on video.

Motorola and Verizon team up for TV tablet

Enjoying success with its Droid smartphones, Motorola now looks to challenge the iPad, with its own tablet device, using Google's Android OS. A partnership with Verizon could mean new online video features for the phone giant's FiOS service. Another sign of evolution in the pay-TV business.

Bewkes: Rental Delays From Netflix, Redbox Is Paying Off For DVD Sales

The 28-day DVD delayed release window Warner Bros. struck with Netflix earlier this year is helping the studio gain better sales for films The Blind Side and Sherlock Holmes. The deal helps Netflix position itself as a valued partner in the midst of declining DVD sales.

Dish to stream live TV on iPad, other devices

Dish Network takes place-shifting to a new level with plans for an iPad app that would allow remote streaming, likely using its Sling technology. Subscription TV, mobile video viewing and cool devices converge.

FCC Calls Off Stakeholders Meetings

The FCC's private net neutrality negotiations are off the rails as a reported bilateral deal between Verizon and Google causes controversy. Next steps are unknown as the FCC's plan to keep Internet playing field level hits a major pothole.Categories: Devices, FIlms, Magazines, Regulation, Satellite, Telcos

Topics: DISH, FCC, iPad, Motorola, Netflix, Verizon, Warner Bros., Wired

-

NDS Leads $20 Million Investment in BlackArrow for Advanced Advertising

Amid all the coverage that online video advertising receives, it's also important to remember that advanced advertising in on-demand and pre-recorded TV continues to evolve. News today that NDS, one of the largest technology providers to multichannel video programming distributors ("MVPDs") is leading a $20 million Series C round in BlackArrow, a provider of advanced advertising solutions, is a reminder of progress. Last week I spoke to Todd Narwid, VP of New Media for NDS and Dean Denhart, BlackArrow's CEO, to learn more about the deal.

("MVPDs") is leading a $20 million Series C round in BlackArrow, a provider of advanced advertising solutions, is a reminder of progress. Last week I spoke to Todd Narwid, VP of New Media for NDS and Dean Denhart, BlackArrow's CEO, to learn more about the deal.

To put the deal and its upside in context, it's important to first understand there's a big difference between how online video advertising against free streams in the open Internet works vs. how advertising against VOD and DVR programs in paid, subscription-based services run by MVPDs works. In the Internet world, there are pretty well-established standards, allowing significant interoperability among sites and ad servers. While measurement challenges persist, the act of getting video ads inserted where they're supposed to be is now pretty straightforward.

Conversely, in the MVPD world, the first challenge is just getting ad serving systems approved and deployed. Because ads are served from within the MVPD's own infrastructure, new ad servers must be tested and integrated with existing video delivery infrastructure residing in distribution centers often called "headends" in the cable world. Unlike MVPDs' broadband deployments, much of MVPDs' TV delivery architecture pre-dates the Internet and therefore is heterogeneous and often difficult to integrate with. In addition, there are the tens of millions of deployed set-top boxes which also differ in their capabilities and openness. MVPDs have made significant progress in creating their own standards and in deploying advanced services, but as anyone who's ever tried to implement any kind of advanced service in the MVPD world can attest, it's hard work and has ground down many promising technology start-ups.

When I first wrote about BlackArrow, on its launch in Oct, '07, I liked its vision of delivering advanced advertising in VOD and DVR programs, but I noted the above challenges gave it a steep hill to climb. Since then, BlackArrow has made progress, deploying with Comcast in Jacksonville, FL and with other operators (though Dean isn't able to mention them due to MVPD restrictions). Still, MVPDs have so many priorities and their resources for testing and integrating new technology are limited. Further, there's a lingering sentiment that MVPDs have only made a half-hearted attempt to really monetize VOD and DVR.

Given these circumstance, the NDS deal appears to offer BlackArrow a lot of upside. As one of the largest technology providers to MVPDs globally ("conditional access" systems that provide secure MVPD video delivery are its main product line, among others), NDS immediately gives BlackArrow both credibility and significantly improved sales and support reach, particularly outside North America. The companies also announced a joint solution offering, which will be key to realizing actual sales Importantly, NDS gives BlackArrow improved financial footing for what promises to be a very long-term process of deploying advanced advertising by MVPDs. Conversely, for NDS, as Todd explained, BlackArrow provides the monetization piece of the puzzle that MVPDs need to create business cases to help them justify NDS's advanced technology delivery systems.

upside. As one of the largest technology providers to MVPDs globally ("conditional access" systems that provide secure MVPD video delivery are its main product line, among others), NDS immediately gives BlackArrow both credibility and significantly improved sales and support reach, particularly outside North America. The companies also announced a joint solution offering, which will be key to realizing actual sales Importantly, NDS gives BlackArrow improved financial footing for what promises to be a very long-term process of deploying advanced advertising by MVPDs. Conversely, for NDS, as Todd explained, BlackArrow provides the monetization piece of the puzzle that MVPDs need to create business cases to help them justify NDS's advanced technology delivery systems.

For MVPDs, who are witnessing the rapid adoption of online video and the threat of cord-cutting down the road, it is essential to be able to offer subscribers more flexible viewing options like VOD and DVR and to give their content partners opportunities to effectively monetize these views. This has been the Achilles heel of VOD and DVR to date, and the scarcity of ad-supported programs in VOD (particularly relative to what's available online) is a direct reflection of this.

Going forward, the challenge for MVPDs will only intensify as content providers face escalating choices about where to optimally monetize their programming. This is where BlackArrow fits in. Plus the company has always had a multi-platform vision, so once it's enabled for TV and DVR, BlackArrow could also provide a pathway to online monetization, which given MVPDs' TV Everywhere initiatives, is also a growing priority.

What do you think? Post a comment now (no sign-in required).

Categories: Advertising, Cable TV Operators, Deals & Financings, DVR, Satellite, Technology, Telcos, Video On Demand

Topics: BlackArrow, Comcast, NDS

-

Here's How Google TV Will Work - And What It Might Mean

Last week, the NY Times shared some details of "Google TV," the new set-top box Google is developing in partnership with Intel and Sony. The article provided a good outline, and now, based on additional information I've gathered, I'm able to provide new details on the box and also explain what it might mean.

The first and most important thing to know about Google TV is that it is not being positioned to induce users to "cut the cord" on their subscriptions to existing multichannel video programming distributors' ("MVPDs" like cable, satellite or telco) services. Or at least that's Google's initial positioning; whether it's genuine or really just a Trojan Horse game plan is another whole matter. For now anyway, Google is taking a "friend of the industry" approach, telling MVPDs that it's briefing that it is looking to complement their businesses by bringing the full Internet to the TV (this follows the same convergence theme as the new Kylo browser).

existing multichannel video programming distributors' ("MVPDs" like cable, satellite or telco) services. Or at least that's Google's initial positioning; whether it's genuine or really just a Trojan Horse game plan is another whole matter. For now anyway, Google is taking a "friend of the industry" approach, telling MVPDs that it's briefing that it is looking to complement their businesses by bringing the full Internet to the TV (this follows the same convergence theme as the new Kylo browser).

Google is contemplating an entirely novel strategy for its set-top box, seeking to insert it alongside the existing MVPD's set-top box by daisy chaining them together via HDMI connections. In other words, the MVPD's set-top's HDMI output would be connected to the Google TV set-top's HDMI input, and then its HDMI output would be connected to the TV. The authorized TV channels would still be delivered, but Google TV would collect data from the MVPD's set-top and introduce an entirely new UI for users to control their TV experience, to include searching and browsing channels. It would also add a host of new interactive web-type capabilities around the content.

Since the Google TV box would have a full browser and connect to the Internet via the user's WiFi or wired access, it would also bring all of the rest of the Internet to the TV as well, including the full breadth of online video (yes, that would mean one more thing for Hulu to block). My understanding is that on the whole, the Google TV experience is extremely impressive and well conceived. In short, it will get the attention of any MVPD executive who has a look at it and will certainly get them to thinking about how able - or unable - they are to deliver a similar experience themselves to their subscribers.

A key reason that Google is planning to insert its box this way is because it believes that in order to deliver a compelling Internet experience on TV requires a new web-based, and open platform. For Google that of course means Android, which it is vigorously proliferating on smartphones as well. Throw in Google's Chrome browser that it is promoting for online usage and you get a glimpse of how Google's multi-platform strategy comes together. While Sony would be making the box, you have to believe it will have Google branding on it, a first for the company in the living room too.

Categories: Cable TV Operators, Devices, Satellite, Telcos

Topics: Comcast, DISH Network, Google, Google TV, Intel, Sony

-

Government to the Rescue in the Retransmission Consent Quagmire?

Earlier this week, in "Will Nasty Fee Fights Fuel Consumers' Cord-Cutting Interest," I conjectured that last weekend's WABC-Cablevision retransmission consent fee fight (the most recent of many fee fights) would ultimately sow consumers' interest "cutting the cord" in favor of free, online-only alternatives. Obviously that would be bad news for multichannel video programming distributors (MVPDs), but it would also be bad for the whole video ecosystem that depends on consumer payments for its economics to work.

In this context it's only mildly surprising that subsequently this week a group of MVPDs including Time Warner Cable, Cablevision, DirecTV, Verizon and others petitioned the FCC to intervene and revise the retransmission consent rules (for what it's worth, I can't remember the last time MVPDs asked the government for anything, except to stay out of their business). In a sure sign of who currently has the negotiating leverage, broadcasters sent their own letter saying the playing field was level and in no need of a review.

With broadcasters intent on getting paid for their signals, there are many chapters yet to be written in the retransmission consent story. The big risk here is that the parties' jousting will ultimately kill the proverbial golden goose, with consumers getting fed up and deciding they'll make do with whatever they can get through the combination of good old-fashioned antennas and a cheap convergence device that hooks their broadband connection to their TV. Cord-cutting has lacked a strong catalyst to date, but history shows that a wronged consumer is a motivated consumer. The TV industry as a whole needs to figure out the retransmission morass before consumers take things into their own hands.

What do you think? Post a comment now (no sign-in required)Categories: Broadcasters, Cable TV Operators, Satellite, Telcos

Topics: Cablevision, DirecTV, NAB, Time Warner Cable, Verizon

Posts for 'Satellite'

Connect with VideoNuze

Exclusive News Roundup

- Disney Selling A+E Global Media Stake To Hearst In Billion-Dollar Deal Deadline

- Netflix and AMC Global Media Ink $500 Million ‘Walking Dead’ Streaming Deal The Hollywood Reporter

- Netflix paying $200M for FIFA Women’s World Cup rights Sports Business Journal

- Fox, iSpot Aim to Deliver Faster Data Tying Ads to Business ‘Outcomes’ Variety

- YES Network, MSG Networks to exit Gotham app for DAZN streaming service CNBC

- HBO Max Dips Toe Into Vertical Video With ‘HBO Max Shorts’ The Hollywood Reporter