-

Recent Cable, Broadcast Financial Performance Suggests Hulu Subscription Model Should be Coming

As the annual "upfronts" - the TV industry's program preview and ad sales extravaganza - kick off today, the recent financial performance of the network TV industry and the cable TV industry continue to diverge. The cable network model, powered by both ad sales and monthly affiliate fees, is proving very durable in the Great Recession, while the ad-only network TV model has been hammered. One conclusion from these numbers is that Hulu's owners must be pushing to figure out how the site can introduce a paid subscription model.

I pulled together financial information for a select group of companies comparing performance for the recently concluded March 31 quarter vs. a year ago.

As the chart shows, operating income increased for all the cable networks and revenue was up for all of them as well, except Scripps Networks, where it was flat. The press release commentary from these cable networks was the same: affiliate revenues are up, with ad sales soft, but not disastrous. Cable operators like Comcast and Time Warner Cable also fared well in the quarter with both revenue and operating income/cash flow increasing.

Contrast this with the broadcast TV numbers for Disney, Fox and CBS, all of which operate both TV networks and own local TV stations. Disney fared the best, with revenues down 2% and operating income down 38%. CBS followed with revenues down 12% and operating income down 49%. Fox was affected the worst, with revenues down 29% and operating income down 99%. As two examples of purely local station performance, Gannett's broadcasting segment revenues were down 16% and operating income down 24%, with Sinclair's revenues down 19% and operating income down 43% (before an impairment charge). The commentary from all the broadcasters was the same: the ad market is terrible, and they're doing their best to contain costs (meaning laying off staff).

As the TV industry gears up to sell billions of dollars of ad time this week, a clear lesson from the above financial performance is that it is essential to diversify into the paid subscription ecosystem instead of relying on advertising alone. Disney, Fox and NBCU have recognized this for a while and have strongly built up their portfolio of cable networks.

With ad sales in the doldrums, it's hard not to wonder what Disney, Fox and NBCU, the three major owners of Hulu, are thinking about with respect to Hulu's own business model, which is of course currently 100% reliant on ads. I mean, if your incumbent business model is frayed, wouldn't it make sense, when essentially "starting over" online, to aggressively pursue the one that is resilient even in the recession?

Hulu's exclusive online lock on high-quality programming from 3 of the 4 broadcast networks would seem to position the company perfectly for a subscription play. If its owners looked hard at the divergent fortunes of cable vs. broadcast, it seems inevitable we'll see some type of paid subscription offering from Hulu - either directly or through distributors - sometime in the near future.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks

Topics: CBS, Disney, FOX, Hulu, NBCU

-

April '09 Recap - Innovation is Alive and Well in the Broadband Video Space

Looking over last month's posts with an eye for 2-3 themes to extract for my recap post today, I was instead struck by one overarching theme: innovation is alive and well in the broadband video space. Other sectors of the economy may have ground to a halt in the current recession, but whether it's new technologies, new service models or new approaches by traditional media companies, the pace of innovation in all things related to broadband video seems only to be accelerating.

Here are some of the examples from last month's posts:

New technologies

- SundaySky - a new approach to dynamically generate videos out of web site content

- HD Cloud - cloud-based encoding and transcoding plus 3rd party syndication

- Market7 - web-based platform for collaboratively creating and producing video

- FreeWheel - ad management/distribution company raises another $12M

New service models

- Sezmi - next-gen video service provider aiming to replace cable/satellite/telco

- TurnHere - distributed video production services for the corporate market

- Babelgum - premium-quality content destination for independent producers

- YuMe Mindshare iGRP - new measurement unit to compare on-air and online ad performance

- YouTube-Disney - short-form promotional deal

New approaches by traditional media companies

- Disney-Hulu - Exclusive 3rd party online distribution for established broadcast network

- Cable networks launching webisodes - online initiatives to attract and retain new online audiences

- New York magazine video re-launch - emphasis on curating best-of-the web videos with brand

- WWE Smashup - fan-submitted video mashup content driving awareness of on-air special

Now granted I have an eye out for broadband innovations so this list is somewhat self-serving. But remember that for every item above I was probably pitched on 2-3 others that I didn't write about due to time limitations. Some of these other items may have been picked up by other news outlets and captured in the news aggregation side of VideoNuze, while plenty of them likely received little attention.

My point is that throughout the whole broadband video ecosystem there is a vibrant sense of entrepreneurialism that is slowly but surely remaking the traditional video landscape. To be sure, not all of this stuff is going to work out; either business models will be faulty, technologies won't deliver as promised or consumers will reject what they're being offered. Nonetheless, from my vantage point, the wheels of innovation continue to spin faster. That makes it a very exciting time to be part of the industry.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Technology

Topics: Babelgum, Disney, FreeWheel, HD Cloud, Hulu, Market7, New York, SezMi, SundaySky, TurnHere, WWE, YouTube, YuMe

-

OK, Hulu Now Has ABC. But When Will It Prove Its Business Model?

OK, Hulu now has ABC in its corner for the next 2 years, along with a re-upped program exclusivity commitment from NBC and Fox. But the nagging question remains: even with all its premium content, fabulous user experience and surging traffic, when will Hulu prove its business model? How that question gets answered will be the real test of Hulu's ultimate success. And with 3 of the 4 broadcast networks now hitching themselves to the Hulu locomotive, the answer is also going to be pivotal to how the industry navigates the broadband video era.

To be clear, VideoNuze readers know that I've been a big fan of Hulu from Day 1. The site has only gotten better over time, not only with more content added, but by continued improvements in the user experience. All of this has no doubt contributed to Hulu's rapid rise up the usage rankings, landing it in the top 3 for the first time in March, with 380M views, according to comScore.

A source familiar with the Disney deal told me the deal was entirely predicated on Disney's desire to tap into Hulu's audience in order to increase ABC's online reach. Among other evidence indicating Hulu's upside potential, comScore data apparently showed that only 8% of the ABC.com audience visits Hulu and only 13% of the Hulu audience visits ABC.com.

To me, three indicators of how much the Hulu deal meant to ABC are the 2 year exclusivity commitment, the

redistribution rights for ABC programs to 3rd parties Hulu gained (except for grandfathered ABC partners), and that ABC will allow its programs to be viewed outside of its much-celebrated video player for the first time.

redistribution rights for ABC programs to 3rd parties Hulu gained (except for grandfathered ABC partners), and that ABC will allow its programs to be viewed outside of its much-celebrated video player for the first time. Importantly, the former two terms effectively foreclose any full-length program distribution deal with YouTube and others. For now at least, ABC will limit its relationship with YouTube to clips only. That's a pretty big call; remember YouTube is the category leader that not only has a 40% share of the market, but is also currently over 15 times the size (in streams) of Hulu. There's also YouTube's relationship with Google, which of course has the most formidable online monetization engine (albeit one that hasn't been fully leveraged by YouTube as yet).

The YouTube decision underscores my ambivalence about the broadcast networks' singular embrace of Hulu because there's little evidence that Hulu has yet developed a profitable or sustainable business model. I've written previously about the paucity of ads in Hulu (and broadcasters' own sites for that matter) and how this is creating user expectations that are going to be hard to reset when more ads are inevitably loaded in. One of the reasons users love Hulu is because it is so light on ads. But will Hulu's traffic flatten or decline when the non-skipppable ad load is 2x, 3x or 4x what it is currently?

Increasingly though, it's not just the ad quantity that's an issue for Hulu, it's also its ad quality. I took some time last night to sample a number of programs on Hulu ("Fringe," "Family Guy," "The Office," "The Daily Show," "Bones"). What I found were the same repetitious ads running throughout all the shows, from a relatively small number of advertisers such as Nissan, AT&T and Swiffer. I detected no meaningful targeting (e.g. I saw a number of Swiffer ads that seem misdirected at this 45 year-old male viewer). Worse, there were an alarmingly high number of PSAs (likely unpaid) from the likes of the Ad Council, Goodwill, One Laptop Per Child, American Diabetes Association, etc. In some cases these were the only ads playing during an entire episode.

Further, there was no evidence of customized ad creative or formats meant to incent deeper engagement (unless you count the companion banners prompting users to click to learn more). Deeper engagement and interactivity are supposed to be the calling cards of broadband video advertising. But the ads on Hulu appear to be the same as seen on-air, suggesting Hulu hasn't been able to persuade its brand advertisers to invest in custom creative to leverage the Hulu environment.

Now I know we're in a recession, but still, over a year since Hulu's official launch, and with its tremendous traffic growth, I think all of this is cause for real concern. Hulu is being embraced by the broadcast industry as its main online video vehicle, yet it isn't close to proving it has a model that can actually make money. I don't have insight as to what's going on here, but I hope the networks that are exclusively entrusting their prized programs to Hulu - and consequently incenting huge real-time shifts in viewer behavior - do.

Longer term of course, the networks' bet on Hulu becomes even more profound. That's because as convergence devices of every stripe bring broadband viewing all the way to users' TVs, there's going to be inevitable cannibalization of viewing traditionally done through linear on-air/cable delivery. (Btw, despite much-heralded research to the contrary, anecdotal evidence suggests this is happening already. Just go ask any college student about their viewing behavior.)

Down the road, networks are going to be increasingly reliant on broadband-based ad revenue as their main meal ticket. And if all that's being served up are digital pennies, nickels or dimes - as I believe Hulu is delivering today - then even all the usage in the world will still leave the networks very hungry indeed.

Now that ABC has thrown in with Hulu, you have to believe CBS will as well. With all of the networks on board, they're increasingly betting the industry on the hope that Hulu can figure out its business model. For their sake, let's hope it can.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters

Topics: ABC, CBS, FOX, Hulu, NBC

-

Disney to Buy Into Hulu

Here I am at BWI airport getting ready to send today's VideoNuze email and in pops the news that Disney is taking an equity stake in Hulu, bringing lots of its prized programming along. The rumor mill has swirled for a while that a deal was forthcoming, now it's here. The press release is not yet up on the Disney site. I'll have more thoughts later.

Categories: Aggregators, Broadcasters, Deals & Financings

-

YouTube Continues Its March Up the Content Quality Ladder

Late yesterday YouTube announced "a new destination for TV shows and an improved destination for movies," moves that continue the site's evolution from its UGC/video sharing roots to an aggregator of premium-quality video.

The reality is that this evolution has been underway for some time now, and I expect it will only continue. Two weeks ago in "6 Reasons Why the Disney-YouTube Deal Matters" I explained again why, as the 8,000 pound gorilla of the online video market, YouTube is in an excellent position to partner with premium content providers. In a media landscape marked by massive audience fragmentation, the online destination (YouTube) that accounts for 40-50% of all streams and is 15 times as big as the #2 destination (Hulu) is quite simply a must-have promotion and distribution partner.

The new destinations address what has been an ongoing Achilles' heel for the site - enabling users to easily find premium video "needles" in YouTube's user-generated "haystack." YouTube's UI weaknesses for

premium video have been highlighted by the gold-plated user experience Hulu - and more recently TV.com and Sling.com - have brought to market. The sites have quickly gained passionate fans, and at least in the case of Hulu, significant viewership.

premium video have been highlighted by the gold-plated user experience Hulu - and more recently TV.com and Sling.com - have brought to market. The sites have quickly gained passionate fans, and at least in the case of Hulu, significant viewership. From a design perspective, while there's nothing I would call truly breakthrough about YouTube's premium destinations, they are still a step forward and a solid start. For users solely interested in premium content, they help organize things nicely. There's a decent selection of content, including titles from deals with MGM, BBC, CBS, Crackle and Lionsgate and lots of other partners, which will no doubt continue to grow.

Possibly more important though, is that for content providers they show how YouTube is serious about addressing their needs for clean, well-lit spaces. Premium content providers want the benefits of being in the massive YouTube site, but without the risk of their brands showing up too close to scruffy UGC material. Being clustered with other premium content is a must.

YouTube's concurrent beta launch of Google TV Ads Online, which allows targeted instream ads, is another positive for premium content providers. Beyond YouTube's massive traffic, Google's potent monetization capabilities are the other reason I've been so bullish on YouTube's prospects for premium content. As I wrote on Monday, with increased DVR penetration driving rampant ad-skipping, broadcast and cable's traditional ad model is looking more and more defunct. Online video ads offer a lot of promise as an even higher value ad medium, but much of it is still unproven. Having large players like Google and YouTube involved is significant for showing online video advertising's true upside.

One last take on this is how YouTube continues to position itself in the "over-the-top" sweepstakes, where multiple competitors are vying to be viewed as bona fide substitutes for cable/satellite/telco subscribers itching to cut the cord. I remain skeptical that the trickle of cord-cutters is going to turn into a gusher any time soon, but I will say that with its move up the content ladder, YouTube continues to burnish its standing as a must-have partner for any convergence device-maker looking to make over-the-top inroads (e.g. Roku, Vudu, AppleTV, etc.). YouTube is the most-recognized online video brand, the most-heavily trafficked, and increasingly a credible alternative to premium aggregators like Hulu and others.

For everyone in the online video ecosystem, YouTube continues to be a key player to watch.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks, FIlms

Topics: Disney, Google, Hulu, Sling, TV.com, YouTube

-

Babelgum's Deal for "The Linguists" Showcases Online Distribution Model

Babelgum, the ad-supported broadband/mobile video aggregator and platform has recently embarked on an expansion into the U.S. market. A discussion I had with Karol Martesko-Fenster, the producer of Babelgum's film channel about the company's recent deal for exclusive worldwide Internet and mobile distribution rights for the new documentary film "The Linguists" reveals how Babelgum is seeking to succeed in an already crowded market, and also provides an outline for how independent content creators can tap the broadband medium.

Karol explained that Babelgum is focusing on premium-only content that fits within its half dozen curated channels. Babelgum's focus is the "Internet Free on Demand" (IFOD) window and it always seeks worldwide

distribution rights, since it targets a global audience. A window of exclusive distribution is also important. To find new films, Babelgum has an acquisitions team that scouts film festivals and also works closely with digital rights aggregators such as Cinetic Rights Management, Content Republic, CAA and others. In addition it often deals directly with the content creators.

distribution rights, since it targets a global audience. A window of exclusive distribution is also important. To find new films, Babelgum has an acquisitions team that scouts film festivals and also works closely with digital rights aggregators such as Cinetic Rights Management, Content Republic, CAA and others. In addition it often deals directly with the content creators. That was the case with The Linguists, a new documentary film from Ironbound Films which Babelgum spotted at the 2008 Sundance Film Festival. Karol noted that the producers had been careful about retaining all of their rights. Babelgum secured a 4 month IFOD exclusive window for The Liguistics in exchange for an advance payment and a 50-50 split of ad/sponsorship revenue. Karol wouldn't specify the size of the advance, but said it's typically in the 4 to 6 figure range and is fully recouped before the splits kick in.

Karol believes Babelgum's willingness to pay advances is a key differentiator relative to competitors who he said are mainly focused on pure revenue-sharing deals. His experience is that for most creators who are even somewhat established, revenue-sharing alone won't be appealing.

Of course to make this model work on ad/sponsorship revenue alone requires Babelgum to be pretty careful about which films it acquires. Karol explained the variables that go into calculating the advance. Among other things, how exposed the film is, the length of exclusivity period and the ad sales team's projections. Then there's the traffic expectations. Babelgum pursues an aggressive online campaign including distributing excerpts to social media sites like Facebook and also distributing the film via an affiliate player to film festival sites and on mobile platforms (iPhone only today).

Karol acknowledges that there's some risk involved here, and that it's still very early days in figuring out the formula for how ad-supported only films will work online. However, Babelgum believes the IFOD window augments other distribution (theatrical, DVD, paid online, TV, etc.) and that the industry has recently begun to understand this. Babelgum's progress will be well worth following.

It's no secret that there's a huge amount of interest among independent content creators to exploit the emerging broadband medium. Karol's advice for independents is to get talks started with online distributors simultaneous with hitting the film festivals, clear all the worldwide rights, and be willing to carve up distribution rights into many different slices (with or without the help of digital rights aggregators).

What do you think? Post a comment now.

Categories: Aggregators, FIlms, Indie Video

Topics: Babelgum

-

YouTube to Merge with Hulu, Entity to be Renamed Either "YouLu" or "HuTube"

In a surprising turn-of-events, VideoNuze has learned that Google will acquire Hulu and merge it with YouTube. The resulting entity will be named either 'YouLu' or 'HuTube.' The merger brings together the two most-trafficked video sites into a powerful new player.

In an interesting twist, the final acquisition price has not yet been determined. Instead, the price will be based on a new algorithm Google is creating to accurately measure just how effective Hulu is at turning its

users' brains into 'creamy giggity-goo' as Seth MacFarlane asserts it will in the latest of Hulu's alien-inspired ads. The algorithm will actually be able to count how many more of users' brain cells die as a result of watching shows on Hulu beyond the cells that already died due to regular on-air network TV viewership.

users' brains into 'creamy giggity-goo' as Seth MacFarlane asserts it will in the latest of Hulu's alien-inspired ads. The algorithm will actually be able to count how many more of users' brain cells die as a result of watching shows on Hulu beyond the cells that already died due to regular on-air network TV viewership. It turns out that Hulu's positioning as an 'evil plot to destroy the world' was considered highly synergistic with Google's longstanding mantra to 'do no evil.' Google CEO Eric Schmidt revealed that the company decided some time ago to move beyond its good-guy image, saying, "Look, we got a lot of mileage out of that 'doing no evil' malarkey, but it's time to get real. We're an avaricious multi-billion company now, and all these wacky tree-hugging green initiatives our engineers keep dreaming up can't hide that." He added, "We really admire the traction Hulu is getting by turning 'evil' into a virtue and want to tap into that concept further. Those Hollywood guys beat us hands-down when it comes to creativity."

For its part, Hulu's owners' decision to merge with YouTube, for a price not yet quantifiable, can only be seen as waiving the white flag of surrender. In an email exchange between Jeff Zucker, NBCU's CEO and Peter Chernin, Fox's former CEO (who made the original Hulu deal), obtained by VideoNuze, Zucker's frustration with Hulu's distant second place status is palpable. Among other things he says, "I thought we had dumbed down our shows as much as possible, but YouTube has clearly tapped into audiences' insatiable appetite for the inane. Who would have thought that skateboard-riding cats crashing into walls would have more audience appeal than our $2 million/episode scripted dramas. There really is no accounting for taste."

In response Chernin is quoted as saying, "Rupert always thought Hulu was a small potatoes deal, not really

capable of losing a large, exciting amount of money. On the other hand, YouTube has been a gigantic black hole for Google, so the opportunity to join forces and achieve scale at losing money together was just incredibly compelling." He added, "Plus, you have to remember, Rupert's heart is really in newspapers. He continues to think this whole Internet thing is a fad that will eventually blow over, with people returning to newspapers as their trusted source of news and propaganda. So the company is logically positioning itself to have sizable video losses to offset expected massive gains in newspaper profitability."

capable of losing a large, exciting amount of money. On the other hand, YouTube has been a gigantic black hole for Google, so the opportunity to join forces and achieve scale at losing money together was just incredibly compelling." He added, "Plus, you have to remember, Rupert's heart is really in newspapers. He continues to think this whole Internet thing is a fad that will eventually blow over, with people returning to newspapers as their trusted source of news and propaganda. So the company is logically positioning itself to have sizable video losses to offset expected massive gains in newspaper profitability."Meanwhile, in a meeting with employees, Hulu CEO Jason Kilar reportedly sought to put a positive spin on the merger. Employees who have Twittered the meeting say that to pump up employee enthusiasm he re-told stories of how much fun it was to originally come up with the name 'Hulu,' reportedly saying, "Look how much mileage we got of one ridiculous-sounding made-up name, just imagine the branding possibilities of the even more-ridiculous sounding names YouLu or HuTube..." Negotiations are already underway with the Chinese portal and domain parking company that own the respective URLs.

The merger left many industry analysts scratching their heads. Representative of their reaction, VideoNuze's Will Richmond said, "Geez, I never thought we'd see a more nonsensical media merger than the one between Time Warner and AOL, but I think this YouLu/HuTube thing might just be it. Let's hope it's not for real, and is just some kind of April Fool's Day joke cooked up by an industry analyst to provide some once-per-year, cheap laughs."

Categories: Aggregators, Deals & Financings

Topics: FOX, Hulu, NBCU, YouTube

-

6 Reasons Why the Disney-YouTube Deal Matters

Late yesterday's announcement that Disney-ABC and ESPN would launch a number of ad-supported channels focused on short-form content was yet another meaningful step in broadband video's maturation process. Here are 6 reasons why I think the deal matters:

1. It validates YouTube as a must-have promotional and distribution partner

For many content providers it's long since become standard practice to distribute clips, and often full-length content, on YouTube. Yet aside from CBS, no broadcast TV network has seriously leveraged YouTube.

That's been a key missed opportunity, as YouTube is simply too big to ignore. It's not just that YouTube notched 100M unique viewers in Feb. '09 according to comScore, it's that the site has achieved dramatically more market share momentum over the past 2 years than anyone else, increasing from 16.2% of all streams to 41% of all streams.

That's been a key missed opportunity, as YouTube is simply too big to ignore. It's not just that YouTube notched 100M unique viewers in Feb. '09 according to comScore, it's that the site has achieved dramatically more market share momentum over the past 2 years than anyone else, increasing from 16.2% of all streams to 41% of all streams. Increasingly, YouTube is not the 800 pound gorilla of the broadband video market; it's the 8,000 pound gorilla. Disney has acknowledged what has long been tacitly understood - as a video content provider, it's impossible to succeed fully without a YouTube relationship.

2. It creates a path for full-length Disney-ABC programming to appear on YouTube and elsewhere

While this deal only contemplates short-form video, and more than likely, mostly promotional clips, it almost certainly creates a path for full-length episodes to appear as well, as the partners build trust in each other and learn how to monetize. Full-length content is most likely to come from ABC, not ESPN (the release

pointedly states no long-form content from ESPN's linear networks is included) as part of a newly expanded distribution approach.

pointedly states no long-form content from ESPN's linear networks is included) as part of a newly expanded distribution approach.For YouTube, which has been aggressively evolving from its UGC roots in its quest to generate revenues, the current clip deal alone is a big win; gaining distribution rights to full-length programs would be an even more significant step. Underscoring YouTube's flexibility, the current deal allows ESPN's player to be embedded, and for Disney-ABC to retain ad sales. YouTube's reported redesign, which places more emphasis on premium content, is yet another way it is getting its house in order for premium content deals.

3. It opens up a new opportunity for original short-form video to flourish

When you think about broadcast TV networks and studios, you immediately think of conventional long-form content. Yet all of these companies have been producing short-form content that either augments their broadcast programs, or is originally produced for broadband, as Disney's own Stage 9 is pursuing. The levels of success of this content have been all over the board.

With YouTube as a formal partner, Disney can aggressively leverage it as its primary distribution platform, gaining more direct access to this vast audience. Facing unremitting market pressures on many fronts, broadcast TV networks themselves need to reinvent their business models. Short-form original content married to strong distribution from YouTube would be a whole new strategic opportunity.

4. It puts pressure on Hulu and other aggregators

It's hard not to see YouTube's gain as Hulu's - and other aggregators' - loss. For sure nothing's exclusive here, and as PaidContent has reported, discussions about Disney distributing full-length programs on Hulu (as well as YouTube) are also underway. But the Disney deal underscores something important that differentiates YouTube from Hulu: YouTube is both a massive promotional vehicle and a potential long-form distributor, while Hulu is really only the latter.

YouTube's benefit derives from its first-mover status. Hulu has done a tremendous job building traffic and credibility in its short life, but it is still distant to YouTube in terms of reach. I continue to believe it is far easier for YouTube to evolve from its UGC roots to become also become a premium outlet than it is for Hulu - or anyone else - to ever compete with YouTube's reach.

5. It raises threat warning to incumbent service providers by another notch

It's also hard not to see the Disney deal moving YouTube's threat level to incumbent video service providers (cable/satellite/telco) up another notch. We discussed YouTube's importance to these companies at the Broadband Video Leadership Evening 2 weeks ago (video here), and I thought the panelists generally did not give YouTube much credit as it deserves.

I continue to believe that of all the various "over-the-top" threats to the current world-order, YouTube is the most meaningful ad-supported one. It has massive audience, a potent monetization engine in Google's AdWords, and with the Disney deal, increased credibility with premium content providers. Especially for younger audiences, the YouTube brand means a lot more than any incumbent service provider's. If I were at Comcast, Verizon or DirecTV, I'd be keeping very close tabs on YouTube's evolution.

6. It exposes the absurdity of the ongoing Viacom-Google litigation

Two weeks ago at the Media Summit I listened to Viacom CEO Philippe Dauman describe the status of his company's $1 billion lawsuit against Google and YouTube. As he talked of mounds of data and reams of documentation being collected and reviewed, I found myself slumping in my chair, thinking about how well all the lawyers involved in the case must be doing, and yet how pointless it all seems.

The old adage "2 wrongs don't make a right" fits this situation perfectly. There is no question that in the past YouTube was lax about enforcing copyright protection on its site and cavalier about how it responded publicly to the concerns of rights-holders. But it has made much progress with its Content ID system and a good faith effort to become a trusted partner. All of this is evidenced by the fact that Disney wouldn't even be talking to YouTube, much less cutting a deal, if it didn't view YouTube as reformed. While the media world is moving on, adapting itself to the new rules of video creation, promotion and distribution, Viacom continues to waste resources and executive attention pursuing this case. To be sure, Viacom has been plenty active on the digital front, but it is long overdue that these companies figure out how to resolve their differences and instead focus on how to work together to generate profits for themselves, not their lawyers.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, Broadcasters, Cable Networks, Partnerships, UGC

Topics: Disney, ESPN, Google, Viacom, YouTube

-

Blockbuster Follows Netflix Onto TiVo Boxes; Ho-Hum

Blockbuster and TiVo have announced that Blockbuster OnDemand movies will be available on TiVo devices. Though I'm all for creating more choice for viewers to gain access to the content they seek, in this

case I don't see the deal creating a ton of new value in the market, as it comes 6 months after Netflix and TiVo announced that Netflix's Watch Instantly service would be available on TiVo devices and nearly 2 years after Amazon and TiVo made Amazon's Unbox titles available for purchase and download to TiVo users. It looks like the main differentiator here is that Blockbuster will begin selling TiVos in their network of physical stores.

case I don't see the deal creating a ton of new value in the market, as it comes 6 months after Netflix and TiVo announced that Netflix's Watch Instantly service would be available on TiVo devices and nearly 2 years after Amazon and TiVo made Amazon's Unbox titles available for purchase and download to TiVo users. It looks like the main differentiator here is that Blockbuster will begin selling TiVos in their network of physical stores. The deal underscores the flurry of partnership activity now underway (which I think will accelerate) between aggregators/content providers and companies with some kind of device enabling broadband access to TVs. I believe the key to these deals actually succeeding rests on 2 main factors: the content offering some new consumer value (selection, price, convenience, exclusivity, etc.) and the access device gaining a sufficiently large footprint. Absent both of these, the new deals will likely find only limited success.

Consumers now have no shortage of options to download or stream movies, meaning that announcements along the lines of Blockbuster-TiVo break little new ground. To me, a far more fertile area to create new consumer value is offering online access to cable networks' full-length programs. As I survey the landscape of how premium quality video content has or has not moved online, this is the category that has made the least progress so far. That's one of the reasons I think the recent Comcast/Time Warner Cable plans are so exciting.

With these plans in the works, but no timetables yet announced, non-cable operators need to be thinking about how they too can gain select distribution rights. There's still a lot of new consumer value to be created in this space. Given lucrative existing affiliate deals between cable networks and cable/satellite/telco operators, I admit this won't be easy. However, Hulu's access to Comedy Central's "Daily Show" and "Colbert Report" does prove it's possible.

We're well into the phase where premium video content is delivered to TVs via broadband. Those that bring distinctive content to large numbers of consumers as easily as possible will be the winners.

What do you think? Post a comment now.

Categories: Aggregators, Devices, FIlms, Partnerships

Topics: Amazon, Blockbuster, Comcast, Netflix, Time Warner Cable, TiVo

-

Vuze Moves PC-to-TV Convergence Another Step Forward

Everywhere I look there are companies doing innovative, clever things to bring broadband video to the TV and to mobile devices.

Yesterday brought another great example, from Vuze, a company with roots as a BitTorrent client that has evolved to an aggregator of hi-def niche broadband video using its desktop application for discovery, download and playback. Vuze announced an update that enables users to drag-and-drop downloaded

videos for playback on non-PC devices such as Xbox, PS3 and - via an integration with iTunes - to the iPhone, Apple TV and iPods. It's a pretty cool extension of the Vuze client experience and I spoke with Vuze's CEO Gilles BianRosa and Sr. Director of Marketing Chris Thun to learn more.

videos for playback on non-PC devices such as Xbox, PS3 and - via an integration with iTunes - to the iPhone, Apple TV and iPods. It's a pretty cool extension of the Vuze client experience and I spoke with Vuze's CEO Gilles BianRosa and Sr. Director of Marketing Chris Thun to learn more. Without getting too far into the technical details, what Vuze has done is capitalized on hooks that have existed in these various devices, making videos downloaded via Vuze visible in these devices' interfaces. As Gilles explained it, these hooks have been available for a while, but only the super-technical would have invested the time and effort to benefit from them.

The connections to Xbox (installed base of 30M) and PS3 (installed base of 23M) are quite complimentary to Vuze, which has 10M unique visitors/mo and about 50M downloads to date, because its content library is heavily skewed toward SciFi, animation, games and comedy (all HD btw) along with its user base. In other words, there's an affinity audience who will immediately benefit from being able to watch Vuze's content on their big screens and on-the-go. In fact, in a recent survey of its users for how they'd want to connect their PCs to TV and mobile, Vuze got 30K responses with a strong emphasis on gaming and Apple devices.

In prior conversations with Gilles I've raised a concern about the viability of Vuze's (or anyone's) client download model given the ever-increasing quality of browser-based streaming. But these integrations do shed new light on the value proposition of having a desktop presence. With its update, Vuze actually goes one step further by automatically transcoding downloaded videos into the format appropriate for the target device, often in real-time, thus eliminating playback issues.

Gilles noted that this is a beta release however, and that one current limitation is that ads cannot be passed through. This is a not insignificant gap for an ad-supported site. Vuze hopes to have ads up and running within a month or so. It also has its eye on integrating with additional devices. My bet is that TiVo is next up given that TiVo founder Mike Ramsey sits on Vuze's board.

For now Vuze's content is relatively nichey and Gilles concedes that despite ongoing negotiations with major studios and TV networks, they're still getting comfortable with Vuze's P2P platform. Given the crowded video aggregator space, Vuze's ongoing challenge is to bolster its content library to broaden its appeal.

But Vuze's new update, sure to mimicked by others, which comes on top of Netflix reporting 1M Watch Instantly users connecting to their Xboxes and consuming 1.5 billion in the first 2 months of its availability, Boxee's multiple integrations and other PC-to-TV convergence initiatives underway, shows the huge pent-up interest users have in watching broadband video on their TVs. The genie is way out of the bottle and content providers need to begin adapting to the coming landscape where video flows between PC, TV and mobile, offering unprecedented convenience to users.

What do you think? Post a comment now.

Categories: Aggregators, Devices, Downloads, HD

-

NBCU's Zucker: "We're at digital dimes now"

NBCU CEO Jeff Zucker provided the opening keynote interview at the Media Summit in NYC this morning with Businessweek Executive Editor Ellen Pollock. I've seen him speak a number of times and true to form he was pragmatic, quite candid and humorous. Highlights below:

"We're at digital dimes now" - Zucker of course famously worried aloud about the risk of "exchanging analog dollars for digital pennies," the notion that half-baked online delivery models would only serve to cannibalize traditional profitability. Zucker sees progress, saying Hulu is "well ahead of plan" and is yes, is now making money. Zucker repeatedly praised the success of the company's wide-ranging digital initiatives, but also noted often there is still a lot of work to do. He also wondered aloud whether digital would ever be a 1 to 1 revenue substitute for traditional revenue streams, but that further cost rationalization would help drive profitability.

"We're in process of finding new economic models" - On the above point, Zucker was candid in saying that the work to be done on new economic models is still experimental and that "a lot of success is often accidental." He readily concedes that nobody has all the answers, and that a key challenge is bridging from the traditional business models to new ones, balancing the interests of older audiences comfortable with the status quo with younger ones that are aggressively embracing the new. Describing his own kids' media activity, which focuses on Hulu, generating their own content and being interactive must give Zucker ample perspective.

"Technology is unbelievably exciting" - Zucker has always emphasized the importance of technology on NBCU's various businesses and today was no exception. He noted that technology is increasing access to TV programs and movies in unprecedented ways, which is a good thing. However he also candidly observed that it has fundamentally changed the broadcast business, primarily through consumers' use of DVRs and online delivery. All of that, plus NBC's lagging primetime performance, has caused it to completely re-think the broadcast model. He observed that newspapers' current woes can be traced to them not being willing to quetion the fundamentals of their model and the role of technology. Like other video providers, he seems determined to confront realities and avoid repeating this mistake.

"NBCU is first and foremost a cable programming company" - Zucker has often highlighted the benefits of the two revenue stream cable programming model (affiliate fees and advertising), but this was the first time I've heard him so clearly position the company as being mainly in the cable business. NBCU's stable of channels, USA, SciFi, Oxygen, MSNBC, Bravo, etc. contributed 60% of NBCU's operating profit last year. The networks' ability to "outperform the market, especially in women's programming and news" is key to NBCU's overall success. Zucker noted that USA is increasingly a "must buy" for advertisers, and with its mass appeal, should justifiably be considered the 5th broadcast network.

"We're hopeful we'll resolve TV.com-Hulu issues soon" - Zucker only briefly touched on Hulu's recent decision to pull its programming from TV.com, which is fast emerging as a Hulu competitor. As has been previously reported, Hulu's attorneys obviously believe TV.com compromised its Hulu distribution agreement as part of its new configuration subsequent to CBS's acquisition of CNET. With a battle looming between aggregators especially in the down economy, I think it remains to be seen whether a settlement can be found.

Categories: Advertising, Aggregators, Broadcasters

Topics: NBCU

-

The Video Industry's Winners and Losers 10 Years from Now: 5 Factors to Consider

Last week a publicly-traded communications-equipment company invited me to speak to a group of investment analysts it had assembled for its annual "investor day." In the Q&A session following my presentation I took a question that I'm not often asked, nor do I give much thought to: "10 years from now, who will be the video industry's winners and losers?"

It's a far-reaching question that doesn't lend itself well to an impromptu answer. Also, while it's great fun to prognosticate about the long run, I've found that it's also a complete crapshoot, which is why my focus is much shorter-term. I've long-believed there are just too many variables in play to predict with any sort of certainty what might unfold 10 years into the future.

Still, as I've thought more about the question, it seems to me that there are at least 5 main factors that will influence the video industry's winners and losers over the next 10 years:

1. Penetration rate of broadband-connected TVs -There's a lot of energy being directed to "convergence" technologies and devices which connect broadband to the TV. Broadband to the TV is a big opportunity for video providers outside the traditional video distribution value chain. It's also a minefield for those who have dominated the traditional model, such as broadcasters. The Hulu-Boxee spat demonstrates this. A high rate of adoption of broadband to the TV technologies will result in more openness and choice for consumers. That's a good or a bad thing depending on where you currently sit.

2. The effectiveness of the broadband video ad model - A large swath of broadband-delivered video is and will be ad-supported. But key parts of the broadband ad model such as standards, reporting and the buying process are still not mature. There's a lot of work going into these elements which is promising. The extent to which the ad model matures (and the economy rebounds) will have a huge influence on how viable broadband delivery is. Producers need to get paid to do good work or it won't get done. The imploding newspaper industry offers ample evidence. Those with robust online ad models like Google are likely to play a key role in helping distribute and monetize premium content.

3. How well the broadcast industry adapts to broadband delivery - The broadcast TV industry generates about $70 billion of ad revenue annually. But both broadcast networks and local stations are on the front lines of broadband's change and disruption, putting a chunk of that ad revenue up for grabs. With broadband-to-the-TV coming, broadcast networks must figure out how to make broadband-only viewership of their programs profitable on a stand-alone basis (i.e. when the online viewing is the sole viewing proposition). Local stations face bigger challenges. As the Internet was to newspapers, broadband delivery is to local stations. They face a slew of new competitors for ad dollars and audiences, while losing their exclusive access to network programming. To what extent they're able to reinvent themselves will determine how much share they hold on to and how much others peel off.

4. How aggressively today's video providers (cable/telco/satellite) and new paid aggregators pursue broadband video delivery - While anecdotes about "cord-cutting" will no doubt only intensify, the reality is that if today's video providers adapt themselves to broadband realities, they are likely to be as strong or stronger 10 years from now. The recent moves from Comcast and Time Warner are encouraging signs that the cable industry gets that being ostriches about the importance of broadband delivery is a road to nowhere. Consumers expect more flexibility and value; incumbents are in a tremendous position to deliver. Ownership of local broadband access networks that serve consumers' unquenchable bandwidth demands is going to be a very good business to be in. That all said, new paid aggregators like Netflix, Amazon and Apple could well steal some share if they aggressively beef up their content, offer a competitive user experience and deliver a better value. They could have a major impact on online movie distribution in particular.

5. The level of investment in startups - The venture capital industry, crucial to the funding of early-stage innovative technology companies, is going through its own turmoil. The industry's limited partners have been wounded by the market's drop, causing VCs to raise smaller funds (if they're even able to do this), limit the number of investments they make, and shy away from betting on big transformational startups. Plenty of strong video technology companies are still successfully raising money, but it's harder than ever. Lots of potentially promising ideas are going begging. The length and severity of the economic slowdown will have a big effect on just how much funding new technologies that can potentially reshape the video landscape over the next 10 years.

So there are 5 factors to consider in how the video landscape shapes up over the next 10 years. Now back to the here and now..

What's your crystal ball say? Post a comment now.

Categories: Advertising, Aggregators, Broadcasters, Cable TV Operators, FIlms

Topics: Boxee, Comcast, Google, Hulu, Time Warner

-

Netflix Confirms "South Park" is Coming to Watch Instantly

Netflix confirmed for me that the first 9 seasons of "South Park" are indeed coming to its "Watch Instantly" streaming service. This was mentioned by South Park's Matt Stone in a longer NY Times story yesterday about the program's digital activities. However, since there was no formal announcement yesterday and I couldn't add South Park episodes to my Netflix Watch Instantly I followed up to verify.

A Netflix spokesman told me that a deal has indeed been signed, and that the formal announcement will

follow later this month when the release timeline has been finalized. He did not comment on the Times report that Netflix is paying for the episodes, though I assume this is almost certainly the case.

follow later this month when the release timeline has been finalized. He did not comment on the Times report that Netflix is paying for the episodes, though I assume this is almost certainly the case. Netflix's move demonstrates the beginnings of what I think is real power in its Watch Instantly model, namely the ability to pay to get great content which itself can be a subscriber acquisition and/or retention tool. I expect we'll see a lot more of Netflix cherrypicking programs and or specific networks to build out its Watch Instantly feature. As it does, it will become an increasingly appealing alternative for early adopter cord-cutters.

What do you think? Post a comment now.

Categories: Aggregators, Cable Networks

Topics: Netflix, South Park

-

The Cable Industry Closes Ranks - Part 2

An article in Friday's WSJ "Cable Firms Look to Offer TV Programs Online" outlined a plan under which Comcast and Time Warner Cable, the nation's 2 largest cable operators, would give just their subscribers online access to cable networks' programming.

A Comcast spokesperson contacted me later Friday morning to explain that the plan, dubbed "OnDemand Online" is indeed in the works, though a release timeline is not yet set. The move is part of the company's

"Project Infinity" a wide-ranging on-demand programming vision that was unveiled at CES '08, but oddly has not been messaged much since. Meanwhile, thePlatform, Comcast's broadband video management/publishing subsidiary also called me on Friday to confirm that - unsurprisingly - it would be powering the OnDemand Online initiative (thePlatform's CEO Ian Blaine explains more in this post).

"Project Infinity" a wide-ranging on-demand programming vision that was unveiled at CES '08, but oddly has not been messaged much since. Meanwhile, thePlatform, Comcast's broadband video management/publishing subsidiary also called me on Friday to confirm that - unsurprisingly - it would be powering the OnDemand Online initiative (thePlatform's CEO Ian Blaine explains more in this post).The idea of cable operators setting up online walled gardens for their subscribers alone was first signaled by Peter Stern, Time Warner's EVP/Chief Strategy Officer on the panel I moderated at VideoNuze's Broadband Leadership Breakfast last November. As I wrote subsequently in "The Cable Industry Closes Ranks" my takeaway from his and other cable executives' recent comments was that the industry was poised to collaborate in order to defend cable's traditional - and highly profitable - business model. Under that model, cable operators currently pay somewhere between $20-25 billion per year in monthly "affiliate fees" to programmers whose networks are then packaged by operators into various consumer subscription tiers.

It should come as a surprise to nobody that both cable networks and operators are mightily incented to defend their model against the incursions of free "over the top" distribution alternatives. Indeed what's surprising to me is why it has taken the industry so long to act forcefully when the stakes are so high and the market's moving so fast? I mean cable operators themselves are the largest broadband Internet access providers in the country, and they have watched for years as their networks have been engorged by surging online viewing, courtesy of YouTube, Hulu, Netflix and others. While they've made some tepid moves to push programming online (though to be fair Comcast's Fancast portal has evolved quite a bit recently), overall their broadband video distribution activities have been underwhelming, evidence of broadband distribution's lower priority status vis-a-vis TV-based video-on-demand.

Meanwhile Friday's article triggered plenty of hackles from the blogosphere that those evil cable operators were up to their old monopolistic tricks, this time moving to control the broadband delivery market and choke off open access to premium video. While it's indeed tempting to see these plans that way, I think that would be the wrong conclusion.

Rather, I look at the Comcast/TWC moves as both welcome and likely to spur more, not less, consumer

access to broadband-delivered programming. That's because, if the cable networks are smart in their negotiations, they will gain from operators the approval to push more of their programs onto both their own web sites, and even to distribute some through others' sites. With net neutrality agitators hopeful in the wake of Barack Obama's election, Comcast and TWC need to tread carefully in these negotiations. Yet another part of the model I foresee is archived programs, which have been locked up in vaults due to programmers' concerns over operator reprisals if they leaked out online, becoming much more openly accessible.

access to broadband-delivered programming. That's because, if the cable networks are smart in their negotiations, they will gain from operators the approval to push more of their programs onto both their own web sites, and even to distribute some through others' sites. With net neutrality agitators hopeful in the wake of Barack Obama's election, Comcast and TWC need to tread carefully in these negotiations. Yet another part of the model I foresee is archived programs, which have been locked up in vaults due to programmers' concerns over operator reprisals if they leaked out online, becoming much more openly accessible. The Comcast/TWC hecklers need to remember one simple fact: to make quality programming requires solid business models. And in this economic climate, solid business models are far and few between. Despite having lost a total of over 500,000 video subscribers during the last 6 consecutive quarters, Comcast still owns one of those few sold models. And don't forget it is now investing to increase its broadband speeds, pledging 30 million, or 65% of its homes, will have 50 Mbps access by the end of '09 (a rollout which incidentally is all privately financed, without a dime of federal bailout money or other assistance).

In the utopian fantasy of some, all premium content flows freely, supported by a skimpy diet of ads alone. For some that works. Yet for cable networks accustomed to monthly affiliate fees this is completely unrealistic and uneconomic. One needs look no further than the wreakage of the American newspaper industry (including bankruptcy filings recently by the Chicago Tribune and today by the Philadelphia Inquirer) to understand the damage that occurs when business model disruption occurs in the absence of coherent, evolutionary planning.

Someday, when broadband video business models mature (as indeed they ultimately will), there will be lots of cable and other programming available for free online. For now though, getting Comcast and TWC to finally pursue an aggressive broadband distribution path is a welcome evolutionary step in unlocking this exciting new medium's ultimate potential.

What do you think? Post a comment now.

(Note: we'll be diving deep into this topic, and others, at VideoNuze's Broadband Video Leadership Evening on March 17th in NYC. More information and registration is here.)

Categories: Aggregators, Broadband ISPs, Cable Networks, Cable TV Operators

Topics: Comcast, Hulu, Netflix, Time Warner Cable, YouTube

-

Hulu vs. Boxee is Litmus Test for Networks

This week's drama between Hulu and Boxee shines the strongest light yet on all of the disruptive forces broadband-delivered video has unleashed: the fight for how video content will reach your living room in the broadband era, and who exactly will control the process. It is a litmus test for major networks in how they intend to transition from the orderly and closed traditional distribution world to the new, open and messy one.

For those who haven't been paying close attention, this week Hulu's CEO Jason Kilar announced in a blog post that its content would no longer be available to users of Boxee, which is an open source media player

that connects broadband delivered content to the TV with a friendly and social interface. Boxee has quickly become a darling of the early adopter and techie set (it's still in "Alpha" release, and only runs on Mac OSX and Ubuntu Linux).

that connects broadband delivered content to the TV with a friendly and social interface. Boxee has quickly become a darling of the early adopter and techie set (it's still in "Alpha" release, and only runs on Mac OSX and Ubuntu Linux). Despite not having a formal agreement from Hulu, several months ago Boxee was able to extend its product to enable Hulu viewing. Hulu promptly became Boxee's #1 content source, and according to Boxee's CEO Avner Ronen, it was recently generating 100K streams per week (note that this amount is still chicken feed relative to Hulu's 240 million monthly streams). Boxee doesn't interrupt Hulu's business model; Hulu's content and ads are shown in their entirety. One would have thought the calculation for Hulu and its owners would be pretty simple: more streams = more ads = more success.

Yesterday I checked in with senior executives around the industry to see what's going on here. The picture that emerges is one of big media companies trying to reassert their control over how users access their content. In his blog post, Kilar says "our content providers requested that we turn off access to our content via the Boxee product, and we are respecting their wishes." According to everyone I spoke to, the unnamed content providers can only be Hulu's two owners, NBC and Fox.

Embracing broadband delivery by backing Hulu was progressive thinking by NBC and Fox. And as long as its skyrocketing usage was perceived as a net positive for on-air distribution (research has shown no cannibalization, higher sampling, more awareness, etc.) and its usage was mainly computer-based, all was fine.

But what Boxee did was extend the Hulu experience to sanctified ground: the TV itself. And that opened a

real can of worms for the networks. Are they aiding and abetting "over the top" user behavior which could lead to "cord-cutting," in turn jeopardizing their highly profitable cable operator relationships? Are they undermining their own P&L's because Hulu usage on TV will cannibalize on-air delivery which carries higher revenues/viewer? Are they setting a dangerous precedent that any scruffy startup can distribute their prized programming without a formal relationship? And so on. These questions were too significant and Boxee's implications too profound to go unchecked. So Hulu's owners snapped its leash.

real can of worms for the networks. Are they aiding and abetting "over the top" user behavior which could lead to "cord-cutting," in turn jeopardizing their highly profitable cable operator relationships? Are they undermining their own P&L's because Hulu usage on TV will cannibalize on-air delivery which carries higher revenues/viewer? Are they setting a dangerous precedent that any scruffy startup can distribute their prized programming without a formal relationship? And so on. These questions were too significant and Boxee's implications too profound to go unchecked. So Hulu's owners snapped its leash.There's just one problem here: what's the impact of the decision on Hulu's users and by extension, the Hulu franchise? A quick perusal of the comments to Kilar's post says it all: people are ballistic and they are deeply confused. They don't get the arbitrary logic of why it's ok to watch Hulu in lots of other ways, but just not through Boxee. And they raise the nightmare scenario that this decision will only serve to fuel piracy, an outcome networks were expected to avoid given the devastating Napster precedent their music industry brethren experienced.

One can only imagine the anguish being felt by Kilar and the Hulu team. Having sweated every detail to create the best video experience out there, it is now watching that goodwill evaporate due to its owners' squeamishness. Better yet, one wonders what the folks at Providence Equity Partners, which invested $100 million in Hulu at a $1 billion valuation, are thinking? Did they sign up at this stratospheric valuation only to see NBC and Fox circumscribe Hulu's reach?

I've been saying for a while now that broadband's openness makes it the single greatest disruptive influence on the traditional video distribution value chain. The Hulu-Boxee situation illustrates this perfectly. Once content providers embrace broadband they inherently give up some of their traditional control. And there's no going back; once the proverbial genie is out of the bottle, it can't be put back in. Hulu, NBC and Fox are learning this first hand. With everyone now watching for their next move, I'm betting a change of heart is forthcoming. Hulu will be back on Boxee in one form or another soon enough. Resistance is futile.

What do you think? Post a comment now.

(Note: Hulu-Boxee is going to be outstanding grist for the Mar 17th Broadband Leadership Evening's panel discussion. Early bird discounted tickets are available through the end of today)

Categories: Aggregators, Broadcasters, Devices

Topics: Boxee, FOX, Hulu, NBC, Providence Equity Partners

-

Crunching comScore's Video Data Yields Market Insights

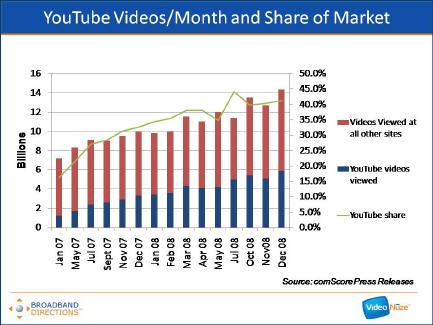

Last week when comScore announced data from its Video Metrix service for December '08, I made a note to myself to go back and look at all the video usage data comScore has released and see what it reveals. Below are 5 charts that I've compiled from comScore's press releases covering January 2007 - December 2008 (note comScore didn't report on every single month during this 24 month period so there are some holes in the graphs).

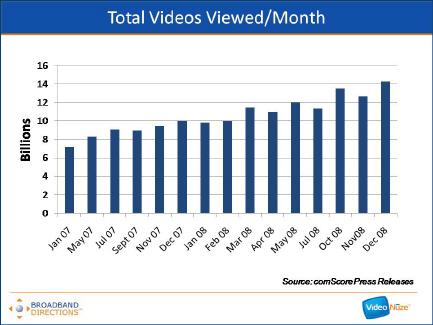

The first graph shows the growth in total videos viewed per month, roughly doubling from 7.2 billion views in Jan. '07 to 14.3 billion views in Dec. '08.

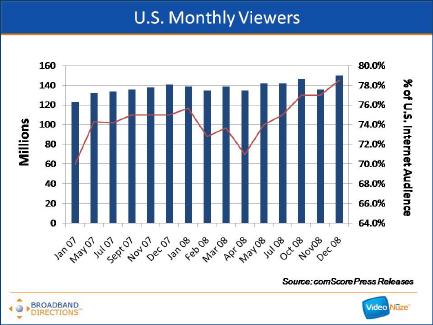

That growth is driven by a number of factors including an increase in the number of monthly viewers from 123 million in Jan. '07 (70% of U.S. Internet users) to 150 million in Dec. '08 (78.5% of U.S. Internet users).

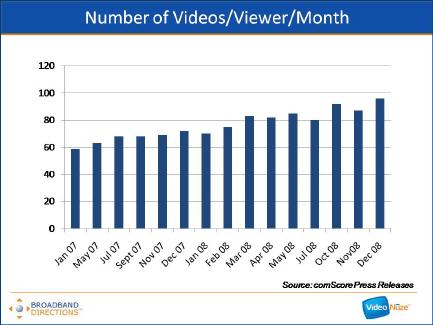

It also reflects an increase in the number of videos viewed per viewer from 59 in Jan. '07 to 96 in Dec. '08.

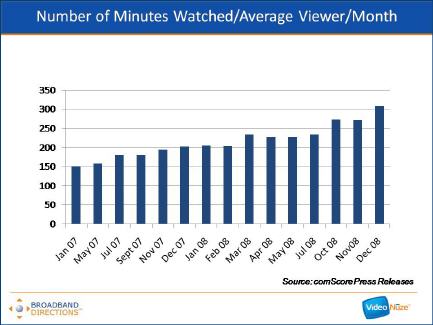

Which further translates into the growth of total number of minutes the average viewer watched per month from 151 minutes per month in Jan. '07 to 309 minutes per month in Dec. '08.

Aside from the sheer growth of the market over the last two years, the most striking thing about the comScore data is the growth in usage and market share by YouTube. Back in Jan. '07, YouTube generated approximately 1.2 billion video views per month for a 16.2% share of all videos viewed. Two years later in Dec. '08 YouTube generated approximately 5.9 billion video views per month for a 41.2% market share. YouTube's share growth is staggering: in every month but 1 during this period YouTube increased its sequential monthly views and in all but 3 months it increased its sequential monthly market share.

Aside from the sheer growth of the market over the last two years, the most striking thing about the comScore data is the growth in usage and market share by YouTube. Back in Jan. '07, YouTube generated approximately 1.2 billion video views per month for a 16.2% share of all videos viewed. Two years later in Dec. '08 YouTube generated approximately 5.9 billion video views per month for a 41.2% market share. YouTube's share growth is staggering: in every month but 1 during this period YouTube increased its sequential monthly views and in all but 3 months it increased its sequential monthly market share.

Recall that Google closed on the YouTube acquisition in Nov. '06 and at $1.65 billion, many thought Google had grossly overpaid. Some may still believe this as YouTube is still very much a work in progress in terms of how it generates revenue. But there's no questioning the phenomenal two-year run it has had in terms of its usage and market share growth. This is one of the reasons why I continue to believe YouTube is one of the most powerful platforms for eventually disrupting the traditional video distribution value chain.

If these slides are hard to view, I've uploaded them all to SlideShare.

What do you think? Post a comment now.

Categories: Aggregators

Topics: comScore, Google, YouTube

-

Netflix Watch Instantly Now Connected to 1 million Xboxes

Netflix has pulled back the curtain a little on its progress connecting its Watch Instantly streaming feature to TVs through its device partners. It and Microsoft have announced that since November '08,1 million Xbox LIVE Gold members have enabled the WI feature, consuming 1.5 billion minutes of movies and TV episodes.

By any measure this is an impressive start. For perspective, this may well be the largest number of people

who have connected broadband to their TVs using an external device. More have probably connected their computers directly to their TVs, but as for devices I can't imagine any other having close to a million (Apple TV? Vudu? Roku?). In addition, simple math suggests that these users would already be watching the equivalent of around 1 movie or so per week (1.5 billion minutes divided by 1 million Xbox users divided by 12 weeks = 125 minutes viewed per user per week). Obviously this is just an average and also doesn't account for the ramp up in users over the 3 months. I think consumption will steadily increase especially if Netflix can expand WI's library of 12K titles.Xbox must represent the largest footprint of Netflix-connected devices, simply because the number of Xbox LIVE Gold members is far larger than the number of owners of TiVo or the Blu-ray players that connect to Netflix. The Xbox adoption rate underscores the validity of Netflix's approach to make WI a value add for its subscribers and to integrate with third-party devices.

VideoNuze readers know I've become extremely enthusiastic about Netflix's broadband activities. The Xbox numbers are a positive early indicator of success. I only see more good news coming down the road.

What do you think? Post a comment now.

Categories: Aggregators, Devices

Topics: Microsoft, Netflix, XBox

-

January '09 VideoNuze Recap - 3 Key Themes

Following are 3 key themes from VideoNuze in January:

Broadband video marches to the TV - At CES in early January there were major announcements around connecting broadband to TVs, either directly or through intermediary devices (a recap of all the news is here). All of the major TV manufacturers have put stakes in the ground in this market and we'll be seeing their products released during the year. Technology players like Intel, Broadcom, Adobe, Macrovision, Move Networks, Yahoo and others are also now active in this space. And content aggregators like Netflix and Amazon are also scaling up their efforts.

Some of you have heard me say that as amazing as the growth in broadband video consumption has been over the last 5 years, what's even more amazing is that virtually all of it has happened outside of the traditional TV viewing environment. Consider if someone had forecasted 5 years ago that there would be this huge surge of video consumption, but by the way, practically none of it will happen on TVs. People would have said the forecaster was crazy. Now think about what will happen once widespread TV-based consumption is realized. The entire video landscape will be affected. Broadband-to-the-TV is a game-changer.

Broadband video advertising continues to evolve - The single biggest determinant of broadband video's financial success is solidifying the ad-supported model. For all the moves that Netflix, Amazon, iTunes and others have made recently in the paid space, the disproportionate amount of viewership will continue to be free and ad-supported.

This month brought encouraging research from ABC and Nielsen that online viewers are willing to accept more ads and that recall rates are high. We also saw the kickoff of "the Pool" a new ad consortium spearheaded by VivaKi and including major brands and publishers, which will conduct research around formats and standards. Three more signs of advertising's evolution this month were Panache's deal with MTV (signaling a big video provider's continued maturation of its monetization efforts), a partnership between Adap.tv and EyeWonder (further demonstrating how ecosystem partners are joining up to improve efficiencies for clients and publishers) and Cisco's investment in Digitalsmiths (a long term initiative to deliver context-based advanced advertising across multiple viewing platforms). Lastly, Canoe, the cable industry's recently formed ad consortium continued its progress toward launch.

(Note all of this and more will be grist for VideoNuze's March 17th all-star panel, "Broadband Video '09: Building the Road to Profitability" Learn more and register here)

Broadband Inauguration - Lastly, January witnessed the momentous inauguration of President Barack Obama, causing millions of broadband users to (try to) watch online, often at work. What could have been a shining moment for broadband delivery instead turned into a highly inconsistent and often frustrating experience for many.

In perspective this was not all that surprising. The Internet's capacity has not been built to handle extraordinary peak load. However on normal days, it still does a pretty good job of delivering video smoothly and consistently. As I wrote in my post mortem, hopefully the result of the inauguration snafus will be continued investment in the infrastructure and technologies needed to satisfy growing demand. That's been the hallmark of the Internet, underscored by the fact that 70 million U.S. homes now connect to the 'net via broadband vs. single digit millions just 10 years ago. I remain confident that over time supply will meet demand.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, Devices, Politics, Technology

Topics: ABC, Adap.TV, Adobe, Amazon, Broadcom, EyeWon, Intel, Macrovision, Move Networks, MTV, Netflix, Nielsen, Panache, VivaKi, Yahoo

-

For YouTube, A William Morris Deal Would Create Issues

The NY Times reported this week that YouTube is in talks with the William Morris talent agency about a possible deal to have some of its clients create videos especially for YouTube.

Nothing's confirmed at this point and who knows if an actual deal will result. However, if one does it would

be a major strategy change for YouTube and I believe would create lots of new issues for the company to deal with. YouTube has always insisted that it is not a content creator; rather its goal has been to be a platform partner for premium video providers seeking to get the most out of the broadband medium. The company has made significant progress on this front while recognizing that its vast collection of user-generated video will always be valued by its users but will be largely unmonetizable. Still, YouTube has been viewed cautiously by large media companies wary of its reach and disruptive potential. There's still lingering concern about why it took so long to get its Content ID system in place to protect its partners' copyrights (lest we forget the residual of that delay is the Viacom lawsuit that still looms).

From my perspective YouTube risks its credibility with its premium partners if the Morris deal happens. It is going to reopen the debate about what YouTube wants to be when it grows up: distribution partner or content creator. Other questions abound: Will the YouTube-Morris content compete directly with certain premium partners? Will the Morris content receive preferential promotional treatment? And how about the risk that data YouTube keeps about its premium partners' channels could be shared with Morris to help guide its content strategy? The questions go on. YouTube may feel it can finesse these questions and/or that its 40% video market share gives it leeway to push the envelope.

I've long thought that YouTube would find it irresistible to eventually get into the content business itself. The logic flows from precedent. For example, in the cable TV world, TCI was once the largest cable operator. It recognized the enormous financial leverage it enjoyed if it evolved beyond simply being packager of others' channels. As partner in channels in which it owned equity, it guaranteed them distribution, which in turn created viewership, ad and affiliate revenues and big-time value. In fact, TCI's content activities were so successful that it ultimately spawned a whole new company, Liberty Media, to manage its programming investments.

Similarly for YouTube, its access to millions of eyeballs creates a lot of temptation to have its own content properties, all the more so as broadband finds its way to the TV. No doubt YouTube has been pitched on this idea repeatedly over the years. But if it chooses to proceed this time it will no doubt hear concerns raised from its partners. Can it be a neutral, committed distribution partner while it also tries to build up its own content portfolio?

Further, there's the specter of Google and its potent monetization engine backing YouTube's content properties, which could also be viewed as competitive with its partners' ad sales efforts. Put all of this together and the potential Morris deal creates lots of new issues. If it comes to fruition it will be interesting to see how YouTube navigates them.

What do you think? Post a comment now.(Update 2/3/09 - Since I posted this piece, sources close to the YouTube-Morris deal have reached out to me and explained that the deal will be similar to the Seth MacFarlane-Media Rights Capital deal previously unveiled on Google Content Network. They have also clarified the point I discussed above, saying that YouTube and Google will remain a platform for distributing content, but will not be involved in producing or taking an equity stake in it.The deal suggests that the Hollywood community continues to think innovatively about how top tier talent can get involved with broadband video. In this case, Morris has a roster of big-name clients and relationships that could be married to the Google Content Network for widespread distribution. No doubt further deals will follow as the model gets further baked. More on this deal and its implications coming soon.)

Categories: Aggregators, Partnerships, UGC

Topics: William Morris Agency, YouTube

-

Netflix's Q4 Results Powered by Streaming; Further Growth Ahead

Netflix's Q4 earnings and business metrics released late Monday are resounding evidence of how important the company's Watch Instantly streaming feature is becoming to its future. Netflix ended '08 with just under 9.4 million subscribers, up 26% for the year. In Q4 '08 it added almost 2.1M gross subs (39% better than in Q4 '07) and 718K net subs (59% better than in Q4 '07). The company generated $51M in free cash flow in Q4 alone, more than in all of 2007. Did someone say there's a recession going? Not for Netflix it seems.

But here's the really interesting news: on the earnings call CEO Reed Hastings pinned the company's ability to beat its Q4 subscriber growth guidance on underestimating "the positive impact of the introduction of the multi-function CE devices from LG Electronics, Samsung, Microsoft and TiVo that promote Netflix streaming." He further added that "streaming is energizing our growth." Those are pretty strong validations of the company's broadband and CE strategy. (Btw, SeekingAlpha has the full transcript here. If you're a Netflix follower like me, it's a must-read.)

Hastings highlighted the LG and Samsung Blu-ray players as having a high connect rate in the 4th quarter,

though noting that in terms of gross numbers Xbox and TiVo were more significant simply because their installed bases are so much larger. It's also important to know that Netflix is paying spiffs to CE partners to generate new Netflix subscribers. That further enhances the relationship between Netflix and its CE-partners. On the one hand Netflix content is both a competitive differentiator for these brands' and a generator of cash while on the other CE partners are a driver of both new subs and streaming adoption for Netflix. Hastings noted that Netflix is in discussions with all major CE companies to "broadly cover the Blu-ray category and Internet TV category over the next few years." In the coming years, expect Netflix to be the content locomotive for marketing broadband-enabled devices the same way that "Intel Inside" was once the technology locomotive for marketing PCs. What other content provider is going to come close to such ubiquity? Possibly Amazon, whose pay-per-download model could actually be complimentary to Netflix in driving more device adoption. But certainly not Apple, which seems intent to yoke its massive iTunes video library to the proprietary Apple TV box in a fruitless (my opinion) attempt to recreate its iPod success.