-

5Min and Scripps Networks Partner in Key Video Syndication Deal

5Min, the video syndication platform company focused on the instructional and lifestyle categories and Scripps Networks, owner of HGTV, Food Network, DIY, Fine Living and Great American Country, are announcing this morning a content and advertising partnership. 5Min, which I described in December, '08 and again in July when it raised $7.5M, is a classic "Syndicated Video Economy" company. Its VideoSeed syndication tool drives relevant video from its content partners to specific pages within its distribution network's web sites. I talked to 5Min CEO/co-founder Ran Harnevo late last week to learn more about the new Scripps deal.

Scripps will be contributing thousands of clips to 5Min for syndication across 5Min's network, which now

generates 22 million unique viewers/mo. This is significant because Scripps owns the premier brands in the food and home & garden categories and so for 5Min the content is an important enhancement to its library. For Scripps, choosing to partner with 5Min is a strong endorsement of the syndication model as a driving force for online video.

generates 22 million unique viewers/mo. This is significant because Scripps owns the premier brands in the food and home & garden categories and so for 5Min the content is an important enhancement to its library. For Scripps, choosing to partner with 5Min is a strong endorsement of the syndication model as a driving force for online video. I've been saying for a while that to succeed in online video, established media companies need to evolve from being "destination-centric" to being "audience-centric." In other words, instead of solely focusing on attracting users to a specific channel or a web site (the traditional approach), it's becoming as important to proliferate content to the Internet's nooks and crannies, to ensure content is available wherever audiences live (niche sites, social media outlets, portals, etc.).

However, I think a key to content providers' succeeding with this model is retaining control over ad inventory that the syndicator creates, to fully leverage their ad sales capabilities. This is another element of

the 5Min-Scripps deal. As Ran explained, Scripps will sell ads against its clips that run in the 5Min network and also against all clips in 5Min's food and home & gardening categories. 5Min will collect a revenue share in exchange. Even though 5Min's own ad sales efforts have been strong, Ran reasoned that with Scripps' reach and relationships, this was a better approach to optimizing the value of the ad inventory.

the 5Min-Scripps deal. As Ran explained, Scripps will sell ads against its clips that run in the 5Min network and also against all clips in 5Min's food and home & gardening categories. 5Min will collect a revenue share in exchange. Even though 5Min's own ad sales efforts have been strong, Ran reasoned that with Scripps' reach and relationships, this was a better approach to optimizing the value of the ad inventory.This model underscores how important the concept of scale is in online video advertising. Ad sales professionals understand that it is not just targeted audiences that appeal to prospective advertisers, it's being able to offer sufficient scale to make them matter. Sub-scale media businesses have a hard time attracting major brand advertisers because their audience sizes are not large enough to meaningfully move the brand's numbers. In other words, no matter how targeted the audience, and how effective the ad campaign, the campaign's results likely will not be sizable enough to register a difference. Scale is not just a problem with niche vertical sites. Larger horizontal sites can have the same problem in certain of their content categories. In fact, whenever you visit a site (or a section of a site) and only see Google AdSense ads, that's likely an example of sub-scale.

The scale issue is particularly relevant in online video and the Internet in general because there's so much audience fragmentation. Barriers to entry for starting a web site are incredibly low, and many sites can obtain some initial traffic flow. But generating ads is another story. Brands and their agencies are not set up to deal with a lot of the Internet's minnows. Their media planning focus is on the whales that have at least reasonable targeting and significant reach. In fact, ad networks often rep smaller sites that don't have their own sales teams (as well as some that do), but even they require some minimal size to ensure they can deliver results.

All of this leads to why smart, automated video syndication is so important for the syndicated video economy to work. High-quality video is still expensive to produce so to really succeed online it needs to drive monetizable views wherever it can, not just at a single destination site. Scripps clearly understands this, and I think others are beginning to as well. Syndication platforms like 5Min's, which allow both content providers and would-be distribution points to be easily and effectively matched, are important glue in this process, which I see only becoming more critical going forward.

What do you think? Post a comment now.

Categories: Cable Networks, Syndicated Video Economy, Technology

Topics: 5Min, Scripps Networks

-

4 News Items Worth Noting from the Week of July 27th

Following are 4 news items worth noting from the week of July 27th:

New Pew research confirms online video's growth - Pew was the latest to offer statistics confirming that online video usage continues to soar. Among the noteworthy findings: Long-form consumption is growing as 35% of respondents say they have viewed a TV show or movie online (up from 16% in '07); watching video is widely popular, draw more people (62%) than social networking (46%), downloading a podcast (19%) or using Twitter (11%); usage is up across all age groups, but still skews young with 90% of 18-29 year olds reporting they watch online vs. 27% of 65+ year olds; and convergence is happening with 23% of people who have watched online reporting they have connected their computers to their TVs.

FreeWheel has a very good week - FreeWheel, the syndicated video ad management company I most recently wrote about here, had a very good week. On Monday, AdAge reported that YouTube has begun a test allowing select premium partners to bring their own ads into YouTube, served by FreeWheel. Then on Wednesday, blip.tv announced that it too had integrated with FreeWheel, so ads could be served for blip's producers across their entire syndication network. I caught up with FreeWheel's co-CEO Doug Knopper yesterday who added that more deals, especially with major content producers, are on the way. FreeWheel is riding the syndication wave in a big way.

Plenty of action with CDNs - CDNs were in the news this week, as Vusion (formerly Jittr Networks) bit the dust, after going through $11 million in VC money. Elsewhere CDN Velocix (formerly CacheLogic) was acquired by Alcatel-Lucent. ALU positioned the deal as fitting with its "Application Enablement" strategy, supporting customers' needs in a "video-centric world." Limelight announced its LimelightREACH and LimelightADS services for mobile media delivery and monetization (both are based on Kiptronic, which it acquired recently). Last but not least, bellwether Akamai reported Q2 '09 earnings, that while up 5% vs. year ago, were down sequentially from Q1. Coupled with a cautious Q3 outlook, the company's stock dropped 20%.

IAC is making big moves into online video - IAC is making no bones about its interest in online video. Last week the company unveiled Notional, a spin-out of CollegeHumor.com, to be headed by that site's former editor-in-chief Ricky Van Veen. Then this week it announced another new video venture, with NBCU's former co-entertainment head Ben Silverman. IAC chief Barry Diller seems determined to push the edge of the envelope, as IAC talks up things like multi-platform distribution and brand integration. With convergence and mobile consumption starting to take hold, the timing may finally be right for these sorts of plays. At a minimum IAC will keep things interesting for industry watchers like me.

Click here to see an aggregation of all of the week's broadband video news

Categories: Advertising, CDNs, Indie Video, Syndicated Video Economy

Topics: Akamai, Alcatel-Lucent, blip.TV, FreeWheel, IAC, Limelight, Pew, Velocix, Vusion, YouTube

-

Blip.TV's New Deals Give Broadband Producers a Boost

Broadband-only producers got a boost yesterday as blip.tv, which provides technology, ad sales and

distribution for thousands of online shows, announced a variety of new deals as well as product improvements. The deals offer blip's producers new distribution, new monetization and new access to TVs. In order:

distribution for thousands of online shows, announced a variety of new deals as well as product improvements. The deals offer blip's producers new distribution, new monetization and new access to TVs. In order:Distribution: blip's new deal with YouTube means that producers using blip can deliver their episodes directly to their YouTube accounts, eliminating the two step process. With YouTube's massive traffic, getting in front of this audience is critical to any independent producer. Since my first conversation with blip's co-founder Mike Hudack several years ago, the company's mantra has been widespread syndication. Blip already distributed its producers' shows to iTunes, AOL Video, MSN Video, Facebook, Twitter, and others. Vimeo is another new distribution partner announced yesterday.

Monetization: A new integration with FreeWheel means that ads blip sells can follow the programs it distributes wherever they may be viewed. I've written about FreeWheel in the past, which offers essential monetization capability for the Syndicated Video Economy. With the blip deal, FreeWheel delivered ads can be inserted on YouTube. This follows news earlier this week that YouTube and FreeWheel had struck an agreement which allows content providers that use FreeWheel and distribute their video on YouTube can have FreeWheel insert their ads on YouTube (slowly but surely YouTube is opening itself up to 3rd parties).

Access to TVs - Last but not least is blip's integration with the Roku player which will help bring blip's shows directly to TVs (adding to deals blip already had with TiVo, Sony Bravia, Verizon FiOS, Boxee and Apple TV). While Roku's footprint is still modest, it is positioned for major growth given current deals with Netflix and Amazon, and others no doubt pending. At $100, Roku is an inexpensive and easy-to-operate convergence device that is a great option for consumers trying to gain broadband access on their TVs. Gaining parity access to TV audiences for its broadband producers is a key value proposition for blip.

In addition to the above, blip also redesigned its dashboard and work flow, making it easier for producers to manage their shows along with their distribution and monetization. An additional deal with TubeMogul announced yesterday allows second by second viewer tracking, providing more insight on engagement.

Taken together the new deals help blip further realize its vision of being a "next generation TV network" and provide much-needed services to broadband-only producers. This group has taken a hit this year, given the tough ad sales and funding environments, so they need every advantage they can get.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, Analytics, Devices, Indie Video, Syndicated Video Economy

Topics: blip.TV, FreeWheel, Roku, TubeMogul, Vimeo, YouTube

-

Video Syndicator 5Min Raises $7.5 Million Series B Round

5Min, a video syndication company specializing in "how-to" content, is announcing this morning that it has raised a $7.5 million series B round, led by new investor Globespan Capital Partners with participation from prior investor Spark Capital. The new round comes on top of the $5 million first round the company raised in January '08. I spoke with CEO Ran Harnevo yesterday to learn more about the company's progress.

5Min, which I last wrote about in Dec. '08, is a textbook Syndicated Video Economy company. As Ran

explained, its key value proposition is an automated, comprehensive solution for sites seeking to incorporate high-quality relevant video that also offers content providers viewership reach and awareness beyond their own destination sites. There is no cost to either distributors or content providers to participate and resulting ad revenues are split among the parties.

explained, its key value proposition is an automated, comprehensive solution for sites seeking to incorporate high-quality relevant video that also offers content providers viewership reach and awareness beyond their own destination sites. There is no cost to either distributors or content providers to participate and resulting ad revenues are split among the parties. The model is enabled by 5Min's VideoSeed syndication platform, which matches video from 5Min's 100,000+ title catalog to pages that its distribution network's sites specify. The matching is based on the video's metadata which 5Min has assigned and a semantic understanding of the pages themselves. 5Min's video player is embedded on these pages, providing content and ads. The network now consists of hundreds of horizontal (e.g. Answers.com, Wikia, etc.) and vertical sites that reach over 200 million unique visitors/mp generating 14 million unique viewers/mo. This is in addition to the 3.5 million unique visitors to its 5Min.com site. Ran wouldn't specify how many actual video views the network is driving, but said it's in the "tens of millions per month."

5Min focuses on key categories in lifestyle, knowledge and instructional and has built critical mass important for advertisers seeking to contextually target these viewers. 5Min has its own sales team and also uses 3rd party ad networks. Primary units are pre-rolls and overlays. Ran says the company has sold out 100% of its inventory, but would only say CPMs are on the "high end of the market."

5Min continues to aggressively grow its content library, but without producing any of its own content. Ran believes strongly that there's plenty of great content out there already, the challenge producers have is getting it more widely distributed, viewed and monetized (all the things 5Min focuses on).

Historically the company has sourced mainly from DVDs, small-to-medium sized video producers and semi-professionals (all with agreements). 5Min is also starting to offer branded content from partners like UGO Entertainment, Motor Trend, Ford Models, Kiplinger's and others. Ran also alluded to upcoming deals with tier 1 video brands. The how-to category itself is chock full of competitors like Demand Media, Howcast and VideoJug that are producing their own video, but at this point the only how-to specific provider 5Min has a deal with is MonkeySee.com.

I'm not surprised by 5Min's success. It is playing to many of the most important trends in the online video space I've written about repeatedly: fragmentation of audiences, the importance of search and SEO for discovery, higher CPMs through targeted advertising, technology to drive distribution scale and the superior value to consumers in certain categories (especially how-to) of video-based content over traditional text-based alternatives. As more and more sites recognize they need video to stay competitive, but that producing it themselves is an expensive and uneconomic proposition, syndicators like 5Min will enjoy ongoing success.

What do you think? Post a comment now.

Categories: Deals & Financings, Syndicated Video Economy

Topics: 5Min, Globespan Capital Partners, Spark Capital

-

June 24th Webinar on Online Video Syndication

Next Wednesday, June 24th at 1:30pm EDT / 10:30am PDT, I'll be presenting in a free webinar, "Demystifying Online Video Syndication." Video syndication continues to be one of the key trends in the online video market. I'll be sharing thoughts on where syndication is heading and where the main opportunities and challenges lie.

I've been writing about the emergence of the "syndicated video economy" for over a year now and during this time syndication has continued to grow in importance for all video content producers and technology providers.

The webinar is sponsored by Grab Networks, whose co-president Marcien Jenckes will present information about its grabMediaOS solution that enables a "Create Once, Publish Anywhere" business model. Grab works with hundreds of content providers and is one of the primary players in driving the video syndication market.

We have 260+ people registered for the webinar already, but there's plenty of room left. If you're trying to understand the syndication opportunity and identify the right solutions to fit your needs, this webinar is for you!

Categories: Events, Syndicated Video Economy

Topics: Events, Grab Networks, Webinar

-

June 24th Webinar on Video Syndication

Please join me on Wednesday June 24th at 1:30pm EDT / 10:30am PDT for a free webinar, "Demystifying Online Video Syndication." As VideoNuze readers know, I've been writing about the emergence of the "syndicated video economy" for over a year now. During this time syndication has continued to grow in importance for all video content producers and technology providers. I hear almost daily about how strategic syndication has become for reaching fragmented online audiences.

I'll be sharing updated trends and data on video syndication, as well as thoughts on where the market is heading. The webinar is sponsored by Grab Networks, whose co-president Marcien Jenckes will provide information on its grabMediaOS solution that enables a "Create Once, Publish Anywhere" business model. Grab was formed from the Fall '08 merger of Anystream and Voxant and it recently announced a $12M financing. Grab works with hundreds of content providers and is one of the key players in driving the video syndication market.

If you're trying to understand the syndication opportunity and identify the right solutions to fit your needs, this webinar is for you!

Categories: Events, Syndicated Video Economy

Topics: Grab Networks

-

A New Old Model for Making Money with Original Online Entertainment Video

Today I'm pleased to introduce "VideoNuze Forums," a periodic opportunity for online video industry experts to contribute their thoughts and ideas to the VideoNuze community. I'm a firm believer that only through the industry's collective ideas and energy will online video reach its ultimate potential.

In this kickoff post, David Graves shares his thoughts on how advertisers can collaborate with online video producers to fund original online entertainment, while leveraging the syndication model. David is a veteran media executive who I've known for years; he's served in executive roles at Yahoo and Reuters, and more recently founded PermissionTV. He's now consulting with Global Capital Strategic Group.

Please contact me if you're interested in contributing. I can't guarantee I'll run everything, but I welcome your ideas.

A New Old Model for Making Money with Original Online Entertainment Video

by David Graves

In the very beginning of television, advertising agencies worked directly with creative people to produce the dramatic programs they wanted to put their ads in. Now, 60 years later, it's time for them to do so again, on the Web.

Between then and now, distributors such as TV networks have become the ones who financed and controlled video programming and acted as the middleman between creatives and advertisers. But today there aren't enough distributors with both the will and the resources to speculatively fund large volumes of online entertainment video.

There are many creative people who would like to produce for the new online medium, particularly now that it can be done for historically low costs. But it's hard to make money. Even so, some dramatic video like Strike.TV is getting produced on the hopes that it will attract an audience that might get sold to advertisers. This is nice but inefficient and usually unprofitable.

In order for the Internet to develop as a substantial platform for original entertainment video, a new model has to form that gives producers some additional upfront confidence. There needs to be a better chance of generating a profit in order to encourage Internet producers to produce and people with money to fund them. Since the paid model is still highly challenged, even for well-known, branded fare (e.g. broadcast network programs), advertising is the most likely source of revenue.

Advertisers are clearly open to the potential benefits of online video advertising. To begin with, they love TV commercials over every other form of advertising. Online, their ads can't be skipped, can be better targeted and offer the possibility of an immediate response or interaction on top of the branding value. What's not to like?

But experiments with advertiser-created programming have by and large been disappointing. That's because it doesn't make sense for advertisers to be the ones financing, creating or distributing video. It's not what they do. On the other hand, partnerships like that of Alloy Entertainment and Johnson & Johnson, to create the "Private" Web series for teen girls, which debuts next month, exemplifies the potential. Brands like Neutrogena will be subtly integrated into the shows.

The model that will work is one where advertisers hook up directly with creative programmers to help encourage show ideas they like. Some call this "branded entertainment" and it can take many forms. For example, it could be an advertising commitment at an agreed-upon CPM, contingent on seeing the finished product. Or a pre-buy that helps fund the production in return for a lower CPM. Even a smile and a wink would have value.

If a producer had an embedded advertiser at a decent CPM, they could arrange for distribution both on their own sites and through syndication. Given the state of ad sales today, offering syndicated sites free, high-quality video content with a built-in CPM split would be like offering the proverbial candy to a baby. Further, there will be syndicators like Pixsy and others who would no doubt be happy to take on the job of arranging distribution for a slice of the CPM.

This model is very similar to the way TV stations have been getting their first run syndicated content (like Oprah and Wheel of Fortune) for years. The programs come with a certain number of embedded commercials along with slots that the stations can sell themselves. It's called "syndicated barter." There are many advertisers who have used this method to ensure that their ads run in the right editorial environment. What they end up paying is the aggregate rating that the individual stations generate.

For original online video entertainment to flourish it seems inevitable that producers and advertisers will need closer partnerships to address the vacuum created by the lack of distribution funding.

What do you think? Post a comment now.

Categories: Advertising, Indie Video, Syndicated Video Economy, VideoNuze Forums

Topics: Alloy, Johnson & Johnson, Pixsy

-

Jambocast: White-Label Video Syndication Platform for Vertically-Focused Web Sites

Jambo Media has moved video syndication another step forward with the official release of "Jambocast," an all-in-one video syndication platform. Jambocast, which is available for white-label licensing, essentially allows vertically-focused web sites to build out their own private video syndication networks. For web site that either don't have their own video, or want to augment what they do have, syndicating video into their sites is a great option. Jambo's CEO Rob Manoff recently explained to me how Jambocast works.

Jambocast follows on the company's success with its own video syndication network, Jambo Video Network

(JVN). According to comScore, JVN ranked #18 in March '09, with 9M unique visitors and 37M video streams (U.S. only). As Rob noted, JVN has taught the company a ton about what's required to build and run a syndication network, lessons it has incorporated into the development of Jambocast.

(JVN). According to comScore, JVN ranked #18 in March '09, with 9M unique visitors and 37M video streams (U.S. only). As Rob noted, JVN has taught the company a ton about what's required to build and run a syndication network, lessons it has incorporated into the development of Jambocast.First and foremost is the importance of offering a comprehensive solution. Rob explained that what he sees as unique about Jambocast is that it offers each piece part of what a syndicator would need - a "video syndication network-in-a-box." Customers get a customizable video player, ad management (which is also integrated with 3rd party ad networks), publisher/syndication management, content management and tracking/reporting. Jambocast's goal is to make it easy to get up and running and start making money. As Rob says, "we're a bunch of ad network guys building a video network with an ad network mentality."

Jambocast also responds to what content providers have been telling Jambo for a while: they want full control of where their content resides. Though embedding has become highly popular, Rob sees Jambocast as the "anti-embed alternative," for content providers who want hyper-distribution, but without risk of their brands ending up in undesirable places. Jambocast's syndication management features give web sites the tools to offer 3rd party content providers comfort.

Jambocast is getting quick traction - customers on board include Mondo Media (adult animation), KidsTube (video aggregator for kids), a large pet-related site (undisclosed for now) plus 6-8 others signed up, but also not yet disclosed.

Jambocast is a classic example of how syndication is continues to permeate the broadband video ecosystem. Though it's distinct, I'd put Magnify.net and KickApps in a somewhat similar orbit, with the former placing more emphasis on UGC and the latter more on social media features. Yet all are part of what I refer to as the Syndicated Video Economy, which continues to grow in influence. Having already made its own syndication network profitable, Jambo is now also going to help others do the same.

What do you think? Post a comment now.

(note: Jambo Media is a VideoNuze sponsor)

Categories: Syndicated Video Economy

Topics: Jambo, Jambocast, KickApps, Magnify.net

-

Visible Measures $10M Series C Round Caps Solid Q1 of Investments in Broadband Video Sector

Yesterday's announcement by Visible Measures that it raised a $10M Series C round is further evidence that broadband video companies are still able to attract financing in this brutal economic climate. Here are other video sector investments I've tracked on VideoNuze in Q1 '09:

- RipCode ($12.5M) - 1/5/09

- SundaySky ($8M) - 1/6/09

- JibJab ($7.5M) - 1/08/09

- Motionbox ($6M) - 1/14/09

- Digitalsmiths (undisclosed from Cisco) - 1/26/09

- Fliqz ($6M) - 1/28/09

- Mixpo ($4M) - 2/2/09

- WhistleBox ($2.3M) - 2/9/09

- Tremor Media ($18M) - 2/19/09

- Auditude ($10.5M) - 3/11/09

Plus 7 others totaling over $80M in the Fall of '08, and no doubt others I've missed.

Visible Measures founder and CEO Brian Shin and Matt Cutler, VP, Marketing & Analytics explained to me yesterday that key to their financing was having both solid short-term traction in the form of customer acquisitions and a long-term story built around increasing transparency and accountability for the burgeoning broadband video medium. This echoes criteria I continue to hear from other industry CEOs successfully raising money in this environment.

Since I initially profiled Visible Measures last June, and then followed-up with a post about their deal with MTV Networks last September, the company has continued to build momentum. Brian said that it's now

powering video measurement and reporting for many of the largest web properties and dozens of advertisers. Revenue is about evenly split between the two categories.

powering video measurement and reporting for many of the largest web properties and dozens of advertisers. Revenue is about evenly split between the two categories. Despite its progress, Brian explained the company has maintained a relatively low profile because neither it nor its customers have wanted to publicize their activities. Brian said there are a few competitors but none that he feels are that close to offering what Visible Measures has, and he'd like to keep it that way by being low-key about their wins. Skeptics might say "a publicity-shy early-stage company? Hmm...." but knowing Brian and his team as I do, I know that's been their approach since starting the company.

Brian added that the new round, led by Northgate Capital, a fund of funds that has also does some direct investing, "presented itself" without Visible Measures out looking for it. But Brian was quick to note that he considers the company extremely fortunate, given that he believes the current environment is even tougher than the post-bubble years in 2001-2003. Northgate is a limited partner in MDV-Mohr Davidow Ventures, one of the company's two original investors, along with General Catalyst. The company has raised a total of $29M to date.

Visible Measures plans to use the new funds to accelerate product development and grow faster. Brian and Matt made repeated references to the mountain of tracking data the company is sitting on, and that many people are interested in accessing it (which I can believe). The intent is to further productize the data, though no specifics were offered.

With publishers facing more pressure than ever to monetize effectively, and advertisers' need to understand the ROI of their spending intensifying, Visible Measures is at the intersection of two very strong trends in the fast-growing broadband video industry. It's also a textbook "syndicated video economy" company, which is yet more wind at its back. I've been bullish for a while on the company's prospects and continue to be so.

What do you think? Post a comment now.

Categories: Deals & Financings, Syndicated Video Economy, Technology

Topics: General Catalyst, MDV-Mohr Davidow, MTV, Northgate Capital, Visible Measures

-

Betawave TV: Video Syndication Aimed at Kids and Moms

The "syndicated video economy" continues to mature with today's announcement of Betawave TV, a video distribution network offering video content and ads to kids age 6-17 and moms. Betawave TV is being launched by Betawave Corp., which was until recently called GoFish (and which also recently raised $22.5M). The company has amassed a U.S. publisher network totaling 25 million monthly unique visitors. I recently spoke to Betawave's executive chairman Jim Moloshok to learn more.

Betawave TV illustrates how broadband is helping merge the traditional concept of an ad network with the

potential for widespread distribution of video to contextually targeted publisher sites. The bet here is that Betawave TV's content and ads can generate more value on its publishers' pages than just pure advertising could. Since Betawave TV's network has a heavy emphasis on gaming sites (e.g. GamesGecko, Hallpass, etc.) that don't have really have video strategies themselves, Betawave TV's offering seems like a good augment. Betawave TV will be released on sites totalling 6 million monthly uniques by the end of Q1.

potential for widespread distribution of video to contextually targeted publisher sites. The bet here is that Betawave TV's content and ads can generate more value on its publishers' pages than just pure advertising could. Since Betawave TV's network has a heavy emphasis on gaming sites (e.g. GamesGecko, Hallpass, etc.) that don't have really have video strategies themselves, Betawave TV's offering seems like a good augment. Betawave TV will be released on sites totalling 6 million monthly uniques by the end of Q1. Of course, these sites are by nature very immersive, so drawing users' attention away from their primary purpose requires compelling content. Betawave TV has a broad content strategy, including licensing from producers like Cookie Jar Entertainment, MGM and Young Hollywood to creating its own series. First up is the fashion-oriented and brand-sponsored "Raven Symone Presents." My guess is that much of Betawave TV's programming is relatively inexpensive to acquire or to produce, all the more so if Betawave TV can do more brand-sponsored deals.

Ultimately, Betawave TV is competing for audience attention and ad dollars that have traditionally flowed to major kids' TV programmers like Disney, Nickelodeon and Cartoon Network. As a piece in Mediaweek just yesterday suggested, 50-75% of ad dollars spent on kids' sites are no longer a part of integrated TV packages. The massive fragmentation of kids' attention away from just watching TV is certainly the underlying cause for this and what Betawave is banking on for success. I can attest to this trend myself: when my 8 1/2 year-old daughter gets together with friends they are far more likely to play games at AmericanGirl.com than watch Disney Channel.

No doubt Betawave TV won't be alone in pursuing kids online with syndicated video and ads. While Jim says they own 100% of the target inventory on their publishers' sites, there's no question these publishers will be evaluating plenty of competing offers in the future. Betawave TV's results will be an interesting test of how mature the video syndication opportunity actually is.

What do you think? Post a comment now.

Categories: Advertising, Syndicated Video Economy

Topics: Betawave

-

Pixsy Premium Feed is Latest Entrant in the Syndicated Video Economy

Pixsy, a white label video search provider made an interesting announcement yesterday about the launch of its new "Premium Feed" service, which I think is another example of the Syndicated Video Economy that I've been talking about for a while now. I talked to Pixsy CEO Chase Norlin about Premium Feed to learn more.

For those of you not familiar with Pixsy, it has been quietly building one of the largest video indexes since its founding in 2005. To date it has mainly focused on licensing the index to partner sites which wanted to offer easy video discovery to their users. As more content providers have offered embedding, Pixsy also enabled found videos to be played right on its partners' sites. Even though activity has grown well, Chase is pretty candid about monetization to date being difficult.

Premium Feed takes embedding to the next level by creating a subset of Pixsy's video index that is both higher-than-average quality and has accompanying pre-roll and overlay ads. Then Pixsy is developing an economic relationship between the content provider and its publisher network by signing redistribution and revenue-sharing deals with both. Chase says that to date the publisher network has 45 million unique visitors/mo and that 1-2 million videos are in the Premium Feed.

One of those publishers is EgoTV, and I chatted with founder/president Jimmy Hutcheson to find out how they're implementing Premium Feed. If you look in the lower right corner of their home page you'll see 3 new "channels," Ego Cars, Ego Comedy and Ego Travel. Each of these are constructed solely of Pixsy Premium Feed videos that are curated by an EgoTV editor. In another example at Ego People, the 300x250 ad in the right column is now populated with the Premium Feed. This is a simple "highest-and-best-use" real estate decision: Jimmy explained that Premium Feed is yielding 2-4x as much net revenue for EgoTV as it would receive if it sold rich media ads in this position.

The concept of bundling content with ads (or vice versa?) and distributing them to sites seeking video and extra monetization is of course at the heart of the syndicated video economy. Much of what Pixsy is doing with Premium Feed is conceptually familiar to Google Content Network, Adconion TV, Voxant (now Grab Networks), Syndicaster, Jambo, Magnify.net, 1Cast and others.

Yet each of these initiatives has its own somewhat differentiated value proposition and underlying technology approach. As syndication grows in importance, sites with strong traffic and an interest in incorporating video will have many choices. As to how they'll decide, Chase makes a good point: simplicity and one-stop shopping are always valued by resource-constrained sites. Providers that can address as many of these sites' potential needs will be in a strong position.

What do you think? Post a comment now.

Categories: Advertising, Syndicated Video Economy, Video Search

Topics: 1Cast, Adconion, EgoTV, Google Content Network, Grab Networks, Jambo, Magnify.net, Pixsy, Syndicaster, Voxant

-

FreeWheel Launches MRM Version 2.0

FreeWheel, whose technology manages video ad inventory and monitors and allocates revenue across multiple syndication partners, gave me a heads up last week that it has launched the 2.0 version of its Monetization Rights Management platform.

FreeWheel is one of the best examples of a company completely focused on the Syndicated Video Economy,

recently announcing CBS and Warner Bros. as customers. The key MRM 2.0 enhancements include auto-translation of third-party ad server tags (which eliminates a layer of manual work), support for IAB in-video ad metrics and improved usability in its work flow.

recently announcing CBS and Warner Bros. as customers. The key MRM 2.0 enhancements include auto-translation of third-party ad server tags (which eliminates a layer of manual work), support for IAB in-video ad metrics and improved usability in its work flow. I caught up with Jed Simmons, COO/co-founder of Next New Networks, which was one of FreeWheel's first customers. Jed's particularly excited about how FreeWheel enables NNN to sell and easily implement specific ad packages across multiple partner sites. He's seen pieces of what FreeWheel does from other companies, but none that are as advanced or focused specifically on syndication's budding opportunities. MRM's advances are another example of why I'm predicting big things from the SVE in '09. The building blocks for syndication's success continue falling into place.

What do you think? Post a comment.

Categories: Syndicated Video Economy, Technology

Topics: FreeWheel

-

Recapping 5 Broadband Video Predictions for 2009

For those who weren't up for reading 700-1,000 words each day last week, today I offer a quick recap my 5 broadband video projections for 2009.

1. The Syndicated Video Economy Accelerates

This one is easily my least controversial prediction, since I've been writing about this trend for most of 2008. The "SVE" as I call it, is an ecosystem of video content providers, distributors and the technology companies who facilitate their relationships. In '08 video content providers increasingly realized that widespread distribution to the sites that users already frequent would improve on the "one central destination site" approach. That's a big change in the traditional media mentality. In '09 the SVE will only accelerate, as the technology building blocks for distributing, monetizing and measuring syndicated video continues to improve. To be sure, the SVE is still nascent, but many companies across the broadband landscape have begun embracing it in earnest.

2. Mobile Video Takes Off, Finally

In '08 VideoNuze has been mainly focused on wired broadband delivery of video to homes and businesses. But as the year has progressed, powerful new mobile devices have mutated the definition of broadband to also include wireless delivery. The huge success of the iPhone and other newer video-capable devices, coupled with 3G, and soon 4G networks, have contributed to mobile delivery finally realizing some of its long-held promise. Still, as some of you commented, obstacles remain. iPhones don't support Flash, the most popular video format. Wireless carriers are careful with doling out too much bandwidth for video apps. And so on. Still, '08 was a big year for video delivery to mobile devices, and I think '09 will be even bigger.

3. Net Neutrality Remains Dormant

Proponents of "net neutrality" legislation, which would codify the Internet's level playing field, expected that under an Obama administration they would finally be granted their wish, particularly since he supported the concept on the campaign trail. But I'm predicting that net neutrality will be dormant for yet another year. Mr. Obama has been emphatic about basing policy decisions on facts and data, and this is an area where net neutrality advocates continue to come up short as there's yet to be any sustained and proven ISP misbehavior. With Mr. Obama and his team having urgent fires to address all around them, there are only two scenarios I can see that move net neutrality up the prioritization list: a startling new pattern of ISP misbehavior or some kind of deal ISPs agree to in exchange for infrastructure buildout subsidies from the stimulus package.

4. Ad-Supported Premium Video Aggregators Shakeout

One of the best-funded categories of the broadband landscape has been aggregators of premium-quality video - TV programs, movies and other well-produced video. These companies have been thought of as potential long-term online competitors to today's video distributors (cable/satellite/telco). However, it's proving very difficult for these sites to differentiate themselves. Content is commonly available, user experience advantages are hard to maintain, user acquisition is not straightforward, audiences are fragmented and ad dollars are under pressure. All of this means that '09 will see a shakeout among the many players in this category, though it's hard to predict at this point who will be left standing (though at a minimum I expect Hulu and Fancast to be in this group).

5. Microsoft Will Acquire Netflix

My long-ball prediction was that at some point in '09 Microsoft will acquire Netflix. Though many of you emailed me offering kudos for boldness, not many are buying into my prediction. Fair enough, I'll either be flat-out wrong on this one or I'll get a gold star for prescience. I provided my rationale, which starts with the assumption that Apple and Google (Microsoft's two fiercest rivals in the consumer space) are best-positioned for success in the battle for the biggest consumer prize of the next 10 years: delivering broadband video services directly to the TV.

I think Microsoft needs to directly play in this space, and Netflix is a perfect vehicle. It has a great brand, a large and loyal subscriber base and excellent back-end fulfillment systems. In 2008 Netflix great strides in broadband, building out its "Watch Instantly" feature. Yet to grow WI's catalog from its current 12K titles to anything approaching the 100K+ available by DVD will require deep financial resources to deal with a recalcitrant Hollywood, and also shelter from quarter-to-quarter earnings pressures. Netflix's measured approach to broadband is consistent with its historical overall operating style. While that style has worked exceedingly well in the past, the broadband-to-the-TV service landscape is wide open right now, and Netflix should be pursuing in a thoughtful, yet ultra-aggressive way. Combined with Microsoft it would be poised to become the broadband video category leader over the next 10 years.

OK, there's the summary. I'll be checking back in on these as the year progresses.

What do you think? Post a comment now.

Categories: Aggregators, Broadband ISPs, Deals & Financings, Mobile Video, Predictions, Syndicated Video Economy

Topics: Apple, Fancast, Google, Hulu, Microsoft, Net Neutrality, Netflix

-

2009 Prediction #1: The Syndicated Video Economy Accelerates

To kick off my 2009 broadband video predictions, here's one that won't surprise loyal VideoNuze readers: the "Syndicated Video Economy" will accelerate in the new year.

This is hardly a controversial assertion given how much I've written in '08 about the SVE, which I first introduced last March. As a refresher, the SVE describes an ecosystem of content providers, distributors and all those who facilitate their relationships. In the SVE, content providers seek widespread distribution of their video. They understand that the Internet itself is a highly fragmented medium and that to optimize viewership, they must shift from "aggregating eyeballs" to a central destination site to instead focus on "accessing eyeballs" wherever target viewers may spend their time: on social networks, with portable devices or game consoles, on personalized portal pages, on vertical subject-driven web sites and myriad other places.

Underlying this transition to widespread distribution is the recognition that, at least for now, advertising is the primary business model for the vast majority of broadband video content providers. Massive scale and accurate targeting are the two key ingredients to optimizing the ad model. While the SVE is still nascent and its ultimate potential is still far off, in '08 a diverse array of SVE enablers began laying the foundation for its future success.

Two of the more interesting initiatives kicked off in '08 were Google Content Network and Adconion.TV, both of which seek to blend content, distribution and advertising into one scalable bundle. I expect more of these kinds of initiatives in '09, especially from ad networks, which are ideally positioned to distribute video to their partner sites. Plenty of others are also distributing premium video into the "mid tail" and "long tail" of web sites such as Grab Networks (a company formed by the Sept '08 merger of Anystream and Voxant), 1Cast, Jambo Media, ClipBlast, Magnify.net and Syndicaster.

An important part of understanding the SVE is that, unlike traditional distribution which was focused on long-form episodes, the SVE is particularly well-suited to targeted distribution of video clips or short series. Creating, bundling and matching these clips to their appropriate audiences is where companies like 5Min, EveryZing, Digitalsmiths, Gotuit and others all play roles. Of course these clips must be managed coherently as part of a content providers' larger catalog, which is why many of the leading content management and publishing platforms like Brightcove, thePlatform, WorldNow, VMIX and others that cater to large media companies also offer syndication features.

With the explosion of video syndication, content providers need the ability to enforce their business rules, measure usage and accurately carry ads even when video is played offline or on mobile devices. These needs are being filled by companies like FreeWheel, Visible Measures, comScore, WebTrends, Kiptronic, Volo Media, Transpera and Azuki Systems. As video is further married to the burgeoning social media landscape, companies like YouTube, KickApps, blip.tv, Slide, RockYou, ClearSpring, Facebook, MySpace and others are all pioneering innovative new forms of community building and user participation.

Thought much of this activity only just started in '08, some of the SVE's rewards are already becoming clear. As one example, Hulu's October traffic as measured by comScore attests to how syndication is powering Hulu's impressive growth.

The innovation and product development that's happening in the SVE, coupled with the broad investment focus on it cause me to be confident about syndication's future. I expect much more activity from all of the companies mentioned above, plus plenty of others I haven't been exposed to yet. In '09 the SVE's foundation will continue to get built out, with users being the ultimate beneficiaries.

What do you think? Post a comment now.

Categories: Syndicated Video Economy

Topics: Syndcated Video Economy

-

5Min Unveils VideoSeed, a Clever Syndication Tool

5Min, one of the many well-funded entrants in the video-based how-to/knowledge space which I wrote about last Feb, has recently introduced VideoSeed, a clever syndication tool that has already helped drive its video to dozens of partner sites aggregating 110 million unique visitors per month. VideoSeed is another indicator that the Syndicated Video Economy is helping shape product development priorities throughout the broadband industry. I spoke to Ran Harnevo, 5Min's CEO/co-founder yesterday to learn more.

VideoSeed's goal is to give 5Min's partners relevant and complimentary video that can be easily inserted into

text-oriented pages with little-to-no editorial oversight. As Ran explained it, a partner signs up, specifies which pages it wants video inserted into, selects parameters of 5Min video it wants to allow and templates for how the video should appear. 5Min editors rank all of its videos 1-5 according to an internal quality scale while rigorously assigning metadata to each.

text-oriented pages with little-to-no editorial oversight. As Ran explained it, a partner signs up, specifies which pages it wants video inserted into, selects parameters of 5Min video it wants to allow and templates for how the video should appear. 5Min editors rank all of its videos 1-5 according to an internal quality scale while rigorously assigning metadata to each.VideoSeed semantically scans all of the partner-submitted pages and matches and inserts relevant 5Min video. (Examples can be seen at Answers.com and wikiHow) As new, relevant videos are added to 5Min, they automatically rotate into the partners' pages. Videos can be viewed on the site or through 5Min's "SmartPlayer" which has features like super slow motion, zooming, etc.)

5Min currently has a library of about 40K videos, of which Ran thinks 80% are sufficiently high quality to be of interest to partners. 5Min commissions some videos and aggregates others. Ran eschews terms like "premium" and "UGC" as they've found some of the best videos come from pure amateurs.

5Min sells ads across the syndication network, using its own team and third-party ad networks. It's using overlays and pre-rolls to date. Revenue is shared with the content providers and publishing partners. Advertisers benefit by reaching a targeted, engaged audience across dozens of sites while only having to make one buy decision.

Text-oriented how-to/knowledge-based sites and subject-driven specialty sites lend themselves perfectly to accepting complimentary syndicated video. But as Ran points out, shooting video, hosting/serving it and selling ads against it is a lot of effort for most text-oriented sites. This is especially true in a down economy when resources are tight. These factors have helped contribute to 5Min expanding its partner audience rapidly to 110 million uniques, with 2-3 new partners coming on board daily.

I could also see the VideoSeed technology being interesting in other categories (celebrity video comes immediately to mind), though for now Ran says 5Min's staying focused on knowledge, and also isn't looking to license VideoSeed externally. No doubt others will watch its progress and look to emulate it. But as Ran notes, to really succeed, they must first focus on assigning highly accurate metadata so the matching process works as intended and users truly get relevant, high quality video.

What do you think? Post a comment now.

Categories: Aggregators, Indie Video, Syndicated Video Economy

Topics: 5Min

-

Adconion.TV: Trying to Do Google Content Network One Better

I've been very intrigued by two recent announcements from Adconion, which bills itself as the largest independent online advertising network.

First, in early October, it announced "AMG-TV," a video content syndication network now called "Adconion.TV" as well as its first deal, to distribute Vuguru's "Back on Topps." Then last week it acquired KTV Digital Media, a production studio and syndicator, to become a wholly-owned subsidiary called RedLever. Late last week I got a briefing from Adconion CEO/founder Tyler Moebius and Reeve Collins, CEO RedLever to learn more.

My take is that Adconion.TV/RedLever is emulating the same model as Google Content Network, except with a couple of interesting twists (for more on GCN, see "Google Content Network Has Lots of Potential, Implications"). Nevertheless, both are classic Syndicated Video Economy plays, which could have a huge impact on the fundamentals of broadband video's future business model.

For those not familiar with Adconion, it says it reaches 260M unique visitors/month, second only to Google.

Traffic is about evenly split between the U.S. and the rest of the world. It has 800+ publishers in its network, including 60-70 that it represents exclusively, primarily for international sales. The company made a big splash earlier this year when it raised a monster $80M round led by Index Ventures (the lead investor in Skype among others). It has grown from 30 employees in '06 to 285 in '08.

Traffic is about evenly split between the U.S. and the rest of the world. It has 800+ publishers in its network, including 60-70 that it represents exclusively, primarily for international sales. The company made a big splash earlier this year when it raised a monster $80M round led by Index Ventures (the lead investor in Skype among others). It has grown from 30 employees in '06 to 285 in '08. The similarities between Adconion.TV and GCN are as follows: both believe their vast network of publisher web sites - which were initially built to serve ads - can now be modified to also accept high-quality syndicated video content. Each leverages the same algorithms it used to optimize which ads to insert, so that video too will only be served to the most appropriate sites. One might think of both these companies as being in the real estate business. Each has colonized vast tracts of web property and is now trying to identify, as real estate pros would say, the "highest and best use" of its inventory: ads, video or some combination of the two.

At the core of both Adconion.TV and GCN is the conviction that content should be brought to users wherever they may live, as opposed to attempting to drive them to a destination site, a la the "must-see TV" model of old. This has been a key tenet of the Syndicated Video Economy concept I've been fleshing out in '08. With the fragmentation of users over the web, social networks, mobile devices, gaming consoles, etc. the way to build a franchise is to propagate video into all of the web's nooks and crannies. Note others like Grab Networks, Syndicaster, 1Cast, Jambo and others are also heavily pursuing the syndication opportunity, each with their own competitive angle.

In both initiatives content-distribution-brand advertising are the three legs of the business model stool. Consider: in Adconion.TV's launch deal it was a package of Vuguru/Back On Topps (content) - Adconion.TV (distribution) and Skype (brand), while GCN's was Seth MacFarlane/Cavalcade of Comedy (content) - GCN (distribution) - Burger King (brand). I asked Tyler whether this three-legged stool is the model for independent broadband content (whose nascent studios have been slammed by the down economy) to be funded in the future, he emphatically replied "yes."

This highlights one key difference between GCN and Adconion.TV. Google of course has been very clear in steering away from content creation, consistently declaring it's "not a content company." Adconion, on the other hand, specifically intends to custom produce brand-infused broadband video programming. That's where the KTV acquisition comes in. Tyler explained that it is deep into talks with numerous agencies and brands about creating programs that showcase the brand sponsors. Two deals are expected to be announced soon.

Another difference is that GCN tried to drive traffic back to YouTube to incent users to subscribe to ongoing program updates and get exposed to other related programs. In my GCN post, I wrote enthusiastically that the marriage of AdSense-powered video distribution as the "spokes" with YouTube as the "hub" was formidable because it gives GCN a mechanism to build ongoing viewership beyond the first exposure at the publisher site.

Today Adconion lacks a comparable destination site. Tyler doesn't think that's important since it offers ways to subscribe, get email alerts and share within the player itself. Plus he's not hearing demand for it from brands. Still I think as this story unfolds and Adconion.TV finds itself competing with GCN for the highest-potential content, a destination site compliment will become essential. Should it agree, an acquisition would make sense to fill this hole (Metacafe? DailyMotion?).

For now though, Adconion has an aggressive plan to build Adconion.TV as an exciting new entry on the Syndicated Video Economy landscape. With its resources, reach and new production capabilities, this is clearly one to keep an eye on.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, Syndicated Video Economy

Topics: 1Cast, Adconion, Google, Google Content Network, Grab Networks, KTV Digital Media, Syndicaster, YouTube

-

The Cable Industry Closes Ranks

First, apologies for those of you getting sick of me talking about the cable TV industry and broadband video; I promise this will be my last one for a while.

After attending the CTAM Summit the last couple of days, moderating two panels, attending several others and having numerous hallway chats, I've reached a conclusion: the cable industry - including operators and networks - is closing ranks to defend its traditional business model from disruptive, broadband-centric industry outsiders.

Before I explain what I mean by this and why this is happening, it's critical to understand that the cable business model, in which large operators (Comcast, Time Warner Cable, etc.) pay monthly carriage or affiliate fees to programmers (e.g. Discovery, MTV, HGTV, etc.) and then bundle these channels into multichannel packages that you and I subscribe to is one of the most successful economic formulations of all time. The cable model has proved incredibly durable through both good times and bad. In short, cable has had a good thing going for a long, long time and industry participants are indeed wise to defend it, if they can.

It's also important to know that the industry is very well ordered and as consolidation has winnowed its ranks to about half a dozen big operators and network owners, the stakes to maintain the status quo have become ever higher. All the executives at the top of these companies have been in and around the industry for years and have close personal and professional ties. There's a high degree of transparency, with key metrics like cash flow, distribution footprint, ratings and even affiliate fees all commonly understood.

One last thing that's worth understanding is that the cable industry has very strong survival instincts, or as a long-time executive is fond of saying, "Real cable people (i.e. not recent interlopers from technology, CPG or online companies that have joined the industry) were raised in caves by wolves." The fact is that the industry started humbly and experienced many very shaky moments. Yet it has managed to survive and continually re-invent itself (for those who want to know more, I refer you to "Cable Cowboy: John Malone and the Rise of the Modern Cable Business" by Mark Robichaux, still the best book on the industry's history that I've read).

All of that brings us to broadband and its potential impact on the cable model. As I've said many times, broadband's openness makes it the single most disruptive influence on the traditional video distribution value chain. Principally that means that by new players going "over the top" of cable - using its broadband pipes to reach directly into the home - cable's model is at serious risk of breaking down, once and for all.

The cable industry now gets this, and I believe has closed ranks to frown heavily on the idea of cable programming, which operators pay those monthly affiliate fees for, showing up for free on the web, or worse in online aggregators' (e.g. Hulu, YouTube, Veoh, etc.) sites. The message is loud and clear to programmers: you'll be jeopardizing those monthly affiliate fees come renewal time if your crown jewels leak out; worse, you'll be subverting the entire cable business model.

And this message isn't being delivered just by cable operators such as Peter Stern from Time Warner who said on my Broadband Video Leadership Breakfast panel that "a move to online distribution by cable networks would directly undermine the affiliate fees that are critical to creating great content." It's also coming from the likes of Discovery CEO David Zaslav who said on a panel yesterday that "there's no economic value from online distribution," and that "great brands like Discovery's must not be undervalued by making full programs available for free online."

The issue is, as a practical matter, can the industry really control all this? If there's zero online distribution, then as Fancast's impressive new head, Karin Gilford said on my panel yesterday, "pressure builds up and another channel inevitably opens" (read that as The Piracy Channel). The problem is that if, for example, an operator does put programs up on its own site - as Fancast is doing - they're available to ALL the site's visitors, not just existing cable subscribers, unless other controls are put in place like passwords, IP address authentication, geo-targeting, etc. But these are confusing and cumbersome to users whose expectations are increasingly being set by broadcasters who are making their primetime programs seamlessly available to all comers.

So what does this closing ranks suggest? Going forward, I think we'll still see cable networks putting up plenty of clips and B-roll video from their programs, maybe the occasional online premiere, some made-for-the-web stuff, paid program downloads (iTunes, etc.) and promotional/community building contests, as Deanna Brown from Scripps described with "Rate My Space" or Zaslav discussed with "MythBusters."

But when it comes to full cable network programs going online, I think that spigot's going to dry up. That has implications for online aggregators like Hulu, who will continue to have big holes in their libraries until they're ready to pay up for these carriage rights. And it also means that broadband-to-the-TV plays are also going to be hampered by subpar lineups unless these companies too are willing to pay for cable programming.

By closing ranks the cable industry's making a bold bet that its ecosystem can withstand broadband's onslaught and the rise of the Syndicated Video Economy. In yesterday's post I noted that the music industry tried a similar approach; we know where that got them. There are plenty of reasons to think things could indeed be different for the cable industry, but there are as many other reasons to think the cable industry is massively deluding itself and could someday be grist for a chapter in the updated version of Clay Christensen's "The Innovator's Dilemma," (my personal bible for how to pursue successful disruption), right alongside the inevitable chapter about how the once mighty American auto industry spectacularly lost its way.

For my part, there are just too many moving parts for me to call this one just yet.

What do you think? Post a comment now!

Categories: Aggregators, Broadcasters, Cable Networks, Cable TV Operators, Devices, Syndicated Video Economy

Topics: Comcast, CTAM Summit, Discovery, Fancast, Scripps, Time Warner

-

EveryZing's New MetaPlayer Aims to Shake Up Market

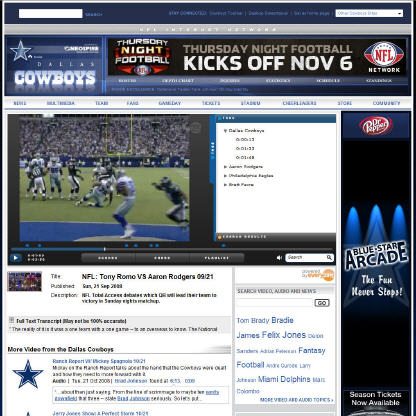

EveryZing, a company I wrote about last February, is announcing the launch of its MetaPlayer today and that DallasCowboys.com is the first customer to implement it. My initial take is that MetaPlayer should have strong appeal in the market, and could well shake things up for other broadband technology companies and for content providers. Last week I spoke to EveryZing's CEO Tom Wilde to learn more about the product.

MetaPlayer is interesting for at least three reasons: (1) it drives EveryZing's video search and SEO capabilities inside the videos themselves, (2) it provides deeper engagement opportunities than typically found in other video player environments and (3) it enables content providers to dramatically expand their video catalogs, while maintaining branding and editorial integrity.

To date EveryZing's customers have used its speech-to-text engine to create metadata for their sites' videos, which are then grouped into SEO-friendly "topical pages" that users are directed to when entering terms into the sites' search box. Speech-to-text and other automated metadata generating techniques from companies like Digitalsmiths are becoming increasingly popular as content providers continue to recognize the value of robust metadata.

MetaPlayer takes metadata usage a step further by creating virtual clips based on specified terms, which are exposed to the user. A user's search produces an index of these virtual clips, which can be navigated through time-stamped cue points, transcript review, and thumbnail scenes (see below for example). The virtual clip approach is comparable in some ways to what Gotuit has been doing and is pretty powerful stuff, as it lets the user jump to desired points, thus avoiding wasted viewing time (e.g. just showing the moments when "Tony Romo" is spoken)

Next, MetaPlayer enables deeper engagement with available video. Yesterday, in "Broadband Video Needs to Become More Engaging," I talked about how the importance of engagement to both consumers and content providers. MetaPlayer is a move in this direction as it allows intuitive clipping, sharing and commenting of a specific video clip within MetaPlayer. Example: you can easily send friends just the clips of Romo's touchdown passes along with your comments on each.

Last, and possibly most interesting from a syndication perspective, MetaPlayer allows content providers to dramatically expand their video offerings through the use of what's known as "chromeless" video players. I was first introduced to the chromeless approach by Metacafe's Eyal Hertzog last summer. It basically allows the content provider to maintain elements of the underlying video player, such as its ability to enforce a video's business policies (ad tags, syndication rules, etc.), while allowing new features to be overlayed (customized look-and-feel, consistent player controls, etc.).

MetaPlayer takes advantage of chromeless APIs available now from companies like Brightcove, and also importantly YouTube. For example, the Cowboys could harvest select Cowboys-related YouTube videos and incorporate them into their site (this is similar to what Magnify.net also enables). With the chromeless approach, the Cowboys's user experience and their video player's branding is maintained while YouTube's rules, such as no pre-roll ads are also enforced.

To the extent that chromeless APIs become more widely available, it means that syndication can really flourish. The underlying content provider's model is protected while simultaneously enabling widespread distribution. All of this obviously leads to more monetization opportunities through highly targeted ads.

Bottom line: EveryZing's new MetaPlayer addresses at least three real hot buttons of the broadband video landscape: improved navigation, enhanced engagement and expanding content selection/monetization. All of this should give MetaPlayer strong appeal in the market.

What do you think? Post a comment now!

Categories: Advertising, Sports, Syndicated Video Economy, Technology, Video Search, Video Sharing

Topics: Brightcove, Dallas Cowboys, Digitalsmiths, EveryZing, Gotuit, Magnify.net, MetaCafe, YouTube

-

At Last, Google Flexes YouTube's Strategic Muscles

In the two years since Google acquired YouTube, I've often wondered about two things: (1) was there really a strategic rationale behind the deal? and, (2) if there was indeed a strategic rationale, when might we see it borne out in actual business initiatives?

For sure YouTube's organic growth has continued unabated during these two years and from a traffic

perspective, it is more dominant now than ever. Yet the dearth of initiatives that are tangibly strategic (or meaningfully revenue-producing for that matter) to Google, or that even minimally strengthen either company's underlying value proposition, has led me to conclude that the deal had more to do with the Google guys wanting to acquire YouTube for its "coolness" factor - simply because they could - than anything else.

perspective, it is more dominant now than ever. Yet the dearth of initiatives that are tangibly strategic (or meaningfully revenue-producing for that matter) to Google, or that even minimally strengthen either company's underlying value proposition, has led me to conclude that the deal had more to do with the Google guys wanting to acquire YouTube for its "coolness" factor - simply because they could - than anything else. I don't mean to sound unfair to the YouTubers who work diligently to make YouTube an incredible experience, which of course it truly is. Yet it is hard to deny the obvious: exactly what has YouTube done differently during the last two years that it couldn't have done had it remained independent (and saying "afforded its monthly CDN bills" doesn't count!), and how exactly have either YouTube or Google benefited from being together during this time?

However, I think things are finally changing. In fact, with little fanfare or proactive PR, Google at last seems to be strategically flexing YouTube's muscles. While some of what they're doing is experimental, other moves have significant market potential and could be highly disruptive to other broadband oriented media and technology companies.

At the top of my "highest potential" list is Google Content Network, especially as it's envisioned as "spokes" tied to YouTube's "hub." I wrote at length about GCN a month ago in "Google Content Network Has Lots of Potential, Implications" so I won't rehash my arguments here. But note yesterday's news about "Poptub" as the second video series to get the GCN/YouTube treatment; I expect a steady drumbeat of these types of deals in the months to come. GCN has the potential to become a key driver of the Syndicated Video Economy.

Another high-potential activity is YouTube's plan to start streaming full episodes. The first deal with CBS is no doubt a signal of many more to come. Full episode streaming is strategic on a number of levels. It enhances YouTube's and Google's access to big brands' ad dollars. While Google has thrived in the self-service, "long tail of advertising" world, it needs more cred among big brands, especially as it pursues its Google TV initiative (see latest deal with NBCU) and other eventual broadband-to-the-TV activities. Full episodes are also a winner from a user standpoint: a unified video experience across premium, indie, long tail and UGC video is very compelling and also squeezes competitors with narrower offerings.

Yet another high-potential activity is the implementation of search ads on YouTube. When the deal was originally done, my first reaction was to think it was a no-brainer to simply start displaying ads against every YouTube search (example - you search for "West Wing" in YouTube and the results page shows an ad to buy the DVD set). If there's one thing Google knows cold, it's the search ad business. YouTube searches represent billions of incremental opportunities each year to extend its core franchise.

Lastly - and this is admittedly more of a "Will Richmond thing" than anything Google or YouTube are yet pursuing: I think it's practically inevitable that the company will start investing in independent broadband video companies at some point. I touched on this in yesterday's piece about NBCU-60Frames and MSN-Stage 9. As time marches on and some of the above activities bear fruit, it's going to become very tempting for Google/YouTube to lever its strengths more directly into content ownership. I know what Google's always maintained about being a technology company, committed to neutrality in way that even Switzerland would appreciate. But as Google's ad business matures and it inevitably is pressured for growth, content is going to be a very alluring opportunity.

Lastly - and this is admittedly more of a "Will Richmond thing" than anything Google or YouTube are yet pursuing: I think it's practically inevitable that the company will start investing in independent broadband video companies at some point. I touched on this in yesterday's piece about NBCU-60Frames and MSN-Stage 9. As time marches on and some of the above activities bear fruit, it's going to become very tempting for Google/YouTube to lever its strengths more directly into content ownership. I know what Google's always maintained about being a technology company, committed to neutrality in way that even Switzerland would appreciate. But as Google's ad business matures and it inevitably is pressured for growth, content is going to be a very alluring opportunity. Regardless of what happens on this last point, YouTube now seems to have a full plate of strategic activities underway. It's great to finally see this happening.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, Broadcasters, Indie Video, Syndicated Video Economy

Topics: 60Frames, CBS, Disney, Google, Google Content Network, MSN, NBCU, YouTube

-

Lessons from Two Recent Deals: NBCU-60Frames and Microsoft/MSN Video-Disney/Stage 9

I always hesitate to conclude too much from just a couple data points, but two deals in the last week - between NBCU and 60Frames and between Microsoft/MSN Video and Disney/Stage 9 - feel to me like leading indicators of more deals of this kind to come.

In case you missed the news, last Tuesday, NBCU and 60Frames, an independent broadband-only studio I've written about, announced a comprehensive content development and ad sales deal. Critically, NBCU will take original broadband-only shows from 60Frames to brands/agencies with which it has relationships to pursue both upfront sponsorships and possible brand integration.

Then this past Monday, Disney and Microsoft announced at MIPCOM that Stage 9, Disney's in-house broadband-only studio which I've also written about, would begin syndicating its shows to MSN Video for European viewers. While smaller in scope, the Disney-MS deal is no less noteworthy.

I see at least three underlying threads to these deals that suggest broader market implications. First, the

deals are further evidence that the broadband-only video model is still nascent and in need of market validation and financial support. If these deals are in fact harbingers, this support will come from established players like NBCU and Microsoft who have significant reach and access to ad dollars. Somewhat ironically these are also companies that have financial stakes (either through direct ownership of or important customer/strategic relationships with) the very incumbent media properties that the broadband-only crowd is trying to grab eyeballs away from.

deals are further evidence that the broadband-only video model is still nascent and in need of market validation and financial support. If these deals are in fact harbingers, this support will come from established players like NBCU and Microsoft who have significant reach and access to ad dollars. Somewhat ironically these are also companies that have financial stakes (either through direct ownership of or important customer/strategic relationships with) the very incumbent media properties that the broadband-only crowd is trying to grab eyeballs away from.Second, the down economy is a catalyst for more of these types of deals. Last week, in "5 Conclusions About the Bad Economy's Effect on Broadband Video," I asserted that the broadband-only studios would tighten their belts a bit to conserve resources in this uncertain climate. One way to mitigate their financial risk and uncertainty is through these linkups with deep pocketed partners. NBCU's backing of the 60Frames slate appears to be the most extensive of these types of deals to date. That Stage 9 - owned by well-funded Disney - is also hunting down big distribution partners which have brand relationships is still further evidence that risk mitigation is a key priority.

Third, the deals point to an acceleration of the trend toward broadband video syndication. In a presentation I give periodically to industry executives, I have a slide titled "Syndicated Video Economy Accelerates" which lists the reasons as: (1) Ongoing video explosion causes heightened need to break through to audiences, (2) Device proliferation causes even more audience fragmentation, (3) Ad model firms up, improving ROI for free, widely distributed video and (4) Social media use means surging user-driven syndication. That slide needs to be updated for a new #1 reason motivating syndication: "In a down economy, syndication could mean the difference between success and failure for broadband-only studios and even big media backed broadband initiatives."

Third, the deals point to an acceleration of the trend toward broadband video syndication. In a presentation I give periodically to industry executives, I have a slide titled "Syndicated Video Economy Accelerates" which lists the reasons as: (1) Ongoing video explosion causes heightened need to break through to audiences, (2) Device proliferation causes even more audience fragmentation, (3) Ad model firms up, improving ROI for free, widely distributed video and (4) Social media use means surging user-driven syndication. That slide needs to be updated for a new #1 reason motivating syndication: "In a down economy, syndication could mean the difference between success and failure for broadband-only studios and even big media backed broadband initiatives."Here's something else to consider: what role might YouTube, the market's undisputed 800 pound gorilla, play as an emerging distributor and financial backer of broadband-only video? Despite its much-avowed