-

thePlatform Continues TV Everywhere Momentum With Cox TV Online

thePlatform continues to rack up large pay-TV operators as customers for its TV Everywhere video management platform, this morning adding Cox TV Online, the TV Everywhere initiative of 3rd-largest U.S. operator Cox Communications. thePlatform is now powering 5 of the top operators in North America, including Comcast (its parent company), Rogers in Canada, BigPond from Telstra in Australia and others. In addition to the operator side of the equation, thePlatform has pushed aggressively into powering content providers' authenticated TV Everywhere programs.

Communications. thePlatform is now powering 5 of the top operators in North America, including Comcast (its parent company), Rogers in Canada, BigPond from Telstra in Australia and others. In addition to the operator side of the equation, thePlatform has pushed aggressively into powering content providers' authenticated TV Everywhere programs.

Categories: Cable TV Operators, Technology

Topics: Cox, thePlatform

-

No Surprise, Ivi is Shut Down

Broadcasters got a win this week as a U.S. District Court judge issued a preliminary injunction against Ivi, requiring the service be shut down. The decision comes as little surprise, as Ivi's claim to being a cable system, and therefore entitled to a compulsory license to rebroadcast TV networks, seemed specious from the start. Though Ivi vows to appeal the decision, casting itself as consumers' savior, there's little reason to believe we'll see Ivi - at least in its current form - back any time soon. Moral here: just because the Internet makes it possible to rebroadcast networks, that still doesn't make it legal.

Categories: Broadcasters, Regulation

Topics: CBS, Cox, Disney, FOX, Ivi, MLB, NBC, PBS, WPIX

-

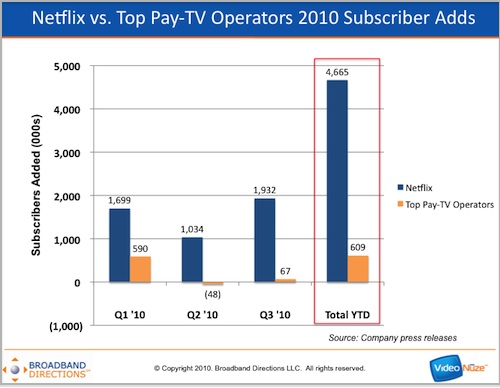

Netflix Has Added 8 Times As Many Subscribers in 2010 As Top Pay-TV Operators, Combined

Here's a pretty amazing factoid to end your week: in 2010 Netflix has added nearly 8 times as many subscribers as 8 of the top 9 pay-TV operators have, combined (#3 cable operator Cox is private and doesn't report). In the first 3 quarters of 2010, Netflix has added nearly 4.7 million subscribers while the top pay-TV operators have gained 609K.

Breaking down the pay-TV industry net gain further, the 2 main telcos (Verizon and AT&T) have added over 1.2 million subscribers and the 2 main satellite providers (DirecTV and DISH) have added 563K, while the top 4 reporting cable operators (Comcast, Time Warner Cable, Charter and Cablevision) have lost over 1.1 million.

Categories: Aggregators, Cable TV Operators, Satellite, Telcos

Topics: AT&T, Cablevision, Charter, Comcast, Cox, DirecTV, DISH, Netflix, Time Warner Cable, Verizon

-

Top U.S. Pay-TV Operators Post Narrow Subscriber Gains in Q3, Rebounding From Q2 Loss

Eight out of the nine largest U.S. pay-TV operators have reported their Q3 '10 results, gaining a slim 66,700 video subscribers, a rebound from a loss of 47,600 subscribers in Q2 '10. The Q2 loss was the first on record for the industry and fueled speculation that "cord-cutting" due to adoption of Internet-delivered video alternatives was rising. With only mildly positive subscriber adds - and 5 of the top 8 operators actually losing subscribers in Q3 - fears that cord-cutting is rising will surely accelerate.

The 8 operators (privately-held Cox Cable, the 3rd-largest cable operator does not disclose its results) represent more than 85% of all U.S. pay-TV households. Though they collectively showed a quarterly gain, if Cox and other cable operators lost subscribers at a comparable rate as the 4 large cable operators in the top 8 (Comcast, Time Warner Cable, Charter and Cablevision), the industry as a whole would have actually lost about 97K subscribers in the 3rd quarter.

Categories: Cable TV Operators, Satellite, Telcos

Topics: AT&T, Cablevision, Charter, Comcast, Cox, DirecTV, DISH, Netflix, Time Warner Cable, Verizon

-

Cox Embraces Over-the-Top Video In Unique Deal With TiVo

Another day, another head-turning example of how the boundaries between traditional and over-the-top (OTT) online video distribution are blurring. This morning Cox Communications, the 3rd-largest U.S. cable operator, is announcing that it will integrate its entire VOD library into TiVo's Premiere multi-purpose box, the first time a major cable operator has done so with a retail-only product. Cox will promote and offer free installation for Premiere which, when coupled with a CableCARD, will support Premiere as a full set-top box solution in its markets (Premiere boxes cost $300 or $500). The deal is a significant win for TiVo, which has continued to rollout clever products, but has been challenged to go beyond its traditional retail proposition.

announcing that it will integrate its entire VOD library into TiVo's Premiere multi-purpose box, the first time a major cable operator has done so with a retail-only product. Cox will promote and offer free installation for Premiere which, when coupled with a CableCARD, will support Premiere as a full set-top box solution in its markets (Premiere boxes cost $300 or $500). The deal is a significant win for TiVo, which has continued to rollout clever products, but has been challenged to go beyond its traditional retail proposition.

As important, TiVo will continue to make available all of its integrated online video offerings (e.g. Netflix, Amazon, YouTube, Break, Howcast, CNET, etc.), which means that Cox is enabling online video options to be exposed and promoted side-by-side with its own video offerings. As Jeff Klugman, TiVo's SVP/GM of Products and Revenue explained to me yesterday, TiVo's search function would allow, for example, a user searching for "30 Rock" to see results including Cox VOD listings for the current season and upcoming on-air episodes blended with prior seasons available from Netflix, Amazon or Blockbuster.

video offerings (e.g. Netflix, Amazon, YouTube, Break, Howcast, CNET, etc.), which means that Cox is enabling online video options to be exposed and promoted side-by-side with its own video offerings. As Jeff Klugman, TiVo's SVP/GM of Products and Revenue explained to me yesterday, TiVo's search function would allow, for example, a user searching for "30 Rock" to see results including Cox VOD listings for the current season and upcoming on-air episodes blended with prior seasons available from Netflix, Amazon or Blockbuster.

Categories: Cable TV Operators, Devices

Topics: Cox, EPIX, Netflix, Starz, TiVo

-

Broadcasters' New Mobile DTV Joint Venture Offers Potential

One of the more interesting things coming out of the NAB Show this week was the announcement by a dozen local TV station groups of a new mobile direct TV content service intended to reach 150 million Americans. The service, which is still unnamed, is backed by Belo, Cox, E.W. Scripps, Fox, Gannett, Hearst, ION, Media General, Meredith, NBC, Post-Newsweek and Raycom. No details on programming were revealed except to saying local and national news, sports and entertainment would be included.

For the last several years, it's felt as if local broadcasters have been on the short end as online and mobile delivery have gained steam. One looming threat has been from broadcast network partners, who have increasingly embraced online distribution, which threatens to shift audiences from consuming programs through local affiliates' stations to consuming at the networks' web sites and aggregators like Hulu.

More recently, the FCC's National Broadband Plan, with its "voluntary" spectrum reclamation would transfer valuable bandwidth to mobile carriers - a move that was quickly perceived as further marginalizing local broadcasters' role in the digital ecosystem. If this wasn't enough, the launch of Apple's iPad highlighted the growing role that consumer electronics devices - and the apps that are built for them - will play in empowering users to search and access content from many new sources, further fragmenting traditional broadcast audiences. All of this has unfolded against the recession's backdrop, which has suppressed consumer spending and local ad spending.

Now, with the new joint venture, local broadcasters seem to have the beginnings of a cohesive plan to show that they too have an important place in the digital era. Throughout the NAB Show various industry executives repeated the mantra that local broadcasters play a vital role in news, weather and emergency information, a not-so-subtle reminder to policy-makers that broadcasters shouldn't be shunted aside in favor of shiny new gadgets.

Still, it's early days for the venture and for mobile DTV in general. Next month a big DTV trial in Washington, DC is scheduled using the ATSC-M/H technical standard. The new JV doesn't have any agreements yet to put DTV tuners in handsets or with carriers for integration. Larger questions of governance still loom as well. Broad industry initiatives like this often suffer from members' differing goals, tactics and motivations. An even larger question is consumers' desire for the mobile DTV format. With countless viewing options already, and more coming every day, local stations' DTV efforts will be in a competitive battle for attention.

Big questions remain about what the new JV's ultimate impact will be, but at a minimum it at least appears to show that local broadcasters are getting serious about how they fit into the digital video ecosystem.

What do you think? Post a comment now (no sign-in required).

Categories: Broadcasters, Mobile Video

Topics: Belo, Cox, E.W. Scripps, FOX, Gannett, Hearst, ION, Media General, Meredith, NBC, Post-Newsweek, Raycom

-

The Battle Over Movie Rentals is Intensifying

News this morning of a $30 million advertising campaign being launched by 8 Hollywood studios and 8 cable operators promoting "Movies on Demand" is fresh evidence that the battle over movie rentals is intensifying. According to the press release, the 12-week campaign, dubbed "The Video Store Just Moved In" is meant to raise consumer awareness of the convenience and affordability of renting movies on cable.

News this morning of a $30 million advertising campaign being launched by 8 Hollywood studios and 8 cable operators promoting "Movies on Demand" is fresh evidence that the battle over movie rentals is intensifying. According to the press release, the 12-week campaign, dubbed "The Video Store Just Moved In" is meant to raise consumer awareness of the convenience and affordability of renting movies on cable.

Cable Video-on-Demand (VOD) has been around for a long while (in fact 20 years ago my summer internship for Continental Cablevision was studying the ROIs for VOD's precursor, "Pay-per-view"). What's new more recently is the growth of so-called "day-and-date" availability - which means movies are released to VOD at the same time as they become available on DVD. The other recent phenomenon is the widespread adoption of digital set-top boxes and other technologies which makes selection, ordering and delivery easier than ever.

Day-and-date availability is a key competitive differentiator for cable vs. other options, though on the surface it seems somewhat incongruous that studios are on board with this considering their desire to protect DVD sales (this was the key goal of the 28-day "DVD sale" window Netflix and Warner Bros. recently created). Yet Kevin Tsujihara, president of Warner Bros. Home Entertainment Group said that apparently research has shown that simultaneous VOD release doesn't hurt DVD sales. All titles Warner Bros. releases to VOD this year will have day-and-date availability.

The day-and-date advantage is evident at least vs. Netflix for the 9 movies the press release cited as the opening slate being promoted: "Precious," "New Moon," "Ninja Assassin," "Pirate Radio," "Astro Boy," "Bandslam," "Did You Hear About the Morgans," Fantastic Mr. Fox" and "The Fourth Kind." A search on Netflix for the 9 revealed that 5 are listed as "Short wait," 1 becomes available on Mar 20th, 1 on Mar 23rd, and 2 on April 13th (none are available for streaming). However, it's a different story for Amazon - all of the cable VOD movies are currently available for rental from Amazon (except "Mr. Fox") and for purchase. The Amazon rental price is $3.99 for each, whereas the rental price from Comcast (my service provide) is $4.99.

For now anyway, it seems Hollywood studios have decided that cable VOD and online rental firms get day-and-date access, while subscription services like Netflix wait longer (btw Redbox too is being pushed into the "wait longer" category). According to the NY Times article, this is likely because VOD and online rental give studios a 65% share of revenue vs. lower percentages for other outlets.

For consumers, the cable VOD option is likely the most convenient and instantly gratifying. There's no new box to set up or pay for as with Roku, TiVo or another, which would be needed to access Amazon VOD, for example, on TV. For those that haven't bridged broadband to their TV with such a box or a direct connection, on-computer viewing only would be a limitation in the experience. Still, while the day-and-date option is key for those consumers who just have to see a particular title right then, because it's a la carte, it's a far more expensive option than a monthly Netflix subscription, which starts at $8.99/mo. Convenience clearly has its price.

Consumers aren't monolithic though; there isn't one right or wrong model. Each viewing option offers pros and cons and consumers will choose which one, given the particular moment or circumstance, best meets their needs. With the battle for movie rentals escalating, the real winner here looks like the consumer who is being presented more choices than ever.

What do you think? Post a comment now (no sign-in required).

Categories: Cable TV Operators, FIlms, Studios, Video On Demand

Topics: 20th Century Fox, Armstrong, Bend Broadband, Bright House Networks, Comcast, Cox, Focus Featu, Insight, iO TV, Time Warner Cable

-

thePlatform's New Cable Deals: Finally, an Industry Push into Broadband Video Delivery?

thePlatform, the video management/publishing company that's been a part of Comcast since early '06, had a very good day yesterday. First it jointly announced with Time Warner Cable a deal to power the #2 cable operator's Road Runner portal. And the Wall Street Journal ran a story stating that it has also signed deals with the cable industry's #3 player Cox Communications and #5 player, Cablevision Systems, which thePlatform corroborates.

Netting all this out, thePlatform will now power 4 of the top 5 cable industry's broadband portals (all except

Charter Communications), with a total reach exceeding 28 million broadband homes, according to data collected by Leichtman Research Group. That also equals approximately 44% of all broadband homes in the U.S. And it's a fair bet that thePlatform's industry penetration will further grow.

Charter Communications), with a total reach exceeding 28 million broadband homes, according to data collected by Leichtman Research Group. That also equals approximately 44% of all broadband homes in the U.S. And it's a fair bet that thePlatform's industry penetration will further grow.I caught up with Ian Blaine, thePlatform's CEO yesterday to learn a little more about the deals and whether the industry's semi-standardization around one broadband video management platform harkens a serious, and I'd argue overdue, industry push into broadband video delivery.

Ian noted that of its various customer deals, the ones with distributors like these are particularly valuable because of their potential for "network effects." This concept means that content and application providers are more likely to also adopt thePlatform if their key distributors are already using it themselves. Ian's point is very valid, as I constantly hear from content providers about the costs of complexity in dealing with multiple distributors and their varying management platforms. Yet the potential is only realized if the distributors actually build out and promote their services, offering sizable audiences to would-be content partners.

This of course has been the aching issue in the cable industry. While they've had their portal plays for years, they've been eclipsed in the hearts and minds of users by upstarts ranging from YouTube to Hulu to Metacafe to countless others, each now drawing millions of visitors each month. While solidly utilitarian, cable's portals (with the possible exception of Comcast's Fancast) are not generally regarded as go-to places for high-quality, or even UGC video. That's been a real missed opportunity.

Ian thinks the industry is experiencing an awakening of sorts, now recognizing the massive potential it's sitting on. This includes its content relationships, network ownership and huge customer reach. Of course, all of this was plainly visible in 1998 as broadband was first taking off, yet here we are 10 years later, and it somehow seems discordant to think the industry is only now grasping its strategic strengths.

Some would explain this as the cable industry being more of a "fast follower" than a true pioneer, a posture that has helped the industry avoid hyped-up and costly opportunities others have chased to their early graves. Others would offer a less charitable explanation: the industry's executives have either been asleep at the switch, overly focused on defending traditional closed video models against open broadband's incursion, or both.

In truth, and as I've mentioned repeatedly, the broadband video industry is still very early in its development, making a "fast follower" strategy still quite viable. Semi-standardization on thePlatform gives the industry a huge potential advantage in attracting content providers. It also gives the industry a more streamlined mechanism for bridging broadband video over to the TV, an area of intense interest now being pursued by juggernauts including Microsoft, Apple, Sony, Panasonic and others.

Still, cable operators' broadband video delivery potential (and the true upside of thePlatform's omnipresence) rests more on whether cable operators are finally going to embrace broadband as an eventual complement, and possibly even successor to their traditional video business model. That would be a major leap for an industry better known for cautious, incremental steps. Time will tell how this plays out.

What do you think? Post a comment!

Categories: Cable TV Operators, Devices, Technology

Topics: Apple, Cablevision, Comcast, Cox, Microsoft, Panasonic, Sony, thePlatform, Time Warner

-

I Got My Official Comcast-TiVo Beta Trial Invite This Week

This week I heard from the folks at Comcast who are running the upcoming beta trial with TiVo. I'm officially on the list and should be getting a box soon. Hooray.

This week I heard from the folks at Comcast who are running the upcoming beta trial with TiVo. I'm officially on the list and should be getting a box soon. Hooray.As many of you are aware, Comcast has been on the cusp of kicking off this trial for some time now, which will let real users experience the joys of TiVo software running inside a Comcast digital set-top box. This will mark a milestone for Comcast in delivering a better user experience than the generic DVR feature that it and other cable operators rolled out a couple of years ago.

After hosting Jeff Klugman, TiVo's Senior VP, GM of its Service Provider and Advertising Engineering Division for a "fireside chat" at a cable industry conference last July, I became very bullish on the opportunity for TiVo to transform itself through these cable deals into a software and services powerhouse. In other words, long-term getting out of the high-cost, low-margin consumer device business.

Running a successful trial with Comcast is all-important to TiVo and they've been working for 2 years on this integration. Success will likely mean wide rollouts with Comcast, followed by #3 operator Cox (with whom TiVo already has a deal), and then others no doubt to follow. I'll be keeping you posted on my experience when I get the box. If it works as advertised it's going to be a killer device.

Categories: Cable TV Operators, Devices, Partnerships

-

TiVo: The Comeback Kid

If some kind of ratio could be calculated to measure consumers’ love for a product in relation to that product’s actual market success, TiVo’s score would undoubtedly top the list. Few products have ever achieved such undying fervor from their owners as have TiVo’s. Yet at the same time, few companies have underachieved their market potential as dramatically as has TiVo since its inception ten years ago.Despite my own love for my TiVo Series 2 box, not that long ago when I was asked by a friend what the future held in store for TiVo, I responded that with deep regret, I was hard-pressed to envision a happy ending for this plucky little company.

However, that was before last week when I had the opportunity to spend an evening with Jeff Klugman, TiVo’s Senior VP, General Manager of its Service Provider and Advertising Engineering Division and David Sandford, TiVo’s Vice President, Marketing & Product Management, Service Provider and Media & Advertising Divisions.

In addition to this time together, I also saw a presentation and demo of TiVo’s new integrated cable TV digital set-top box offering and also hosted them for a "fireside chat." All of this happened at a CTAM of New England-organized session at a cable TV industry conference in Newport, R.I.

Much as I thought I’d never say this, hear me now: TiVo is going to be the Comeback Kid. And it’s completely clear why. Read on to understand my logic.

The Old TiVo: Making Buyers "Crawl Across Broken Glass" to Enjoy the ProductAn immutable law of TiVo ownership has always existed: once you get one set up, you will fall in love with it. With its simple program recording process, tantalizing ad-skipping capability, intuitive user interface and more recently, its endless series of innovations (home networking readiness, remote scheduling, TiVoToGo portability, WishLists, Amazon Unbox downloads, Universal Swivel Search, TiVoCast broadband video channels, etc. etc.) TiVo is a blockbuster consumer value proposition.Despite all this, TiVo has always suffered from a problem that Jeff Klugman astutely describes: the company has essentially made prospective buyers "crawl across broken glass" to get from purchase decision to completed setup. Such a harsh assessment is well-earned. Consider: first TiVo required the user to find their way to a retail store (or go online) to buy the TiVo box, further cluttering the precious shelf space beneath the TV set. Then it required the buyer to select a monthly service plan that was on top of what the consumer already paid for cable TV or satellite service (to add insult to injury, TiVo did away with its $300 "Lifetime"plan a while ago). This change meant that a consumer’s choice to have a one-time bloodletting was replaced with a requirement that TiVo stick its probe into your credit card for as long as you wished to continue getting the service.

But that wasn’t all. Get the TiVo box home and you faced the oh-so-pleasurable task of contorting your body to access the back of your TV, while fending off that embarrassing swarm of dust bunnies lurking back there, all the while juggling a flashlight to figure out how TiVo’s gaggle of wires should marry up to your existing gaggle of wires. Your persistent fear was that not only might you end up not actually getting TiVo to work, you might find that you irreversibly tampered with your existing set-up, reducing your TV to a snow-and-static haze. Factor in your family members glowering at you while you puzzled through this process and it’s a pretty daunting and ugly picture.

This picture became even uglier when cable and satellite operators introduced a viable alternative to TiVo several years ago: simply pay a few extra bucks to them and you can have DVR features (ok, a sucky imitation of TiVo to be sure) built right into your new digital set-top box. So no contorting, fretting, glowering and of course, no extra box to buy and install.

TiVo’s Picture Darkens FurtherGiven this rigmarole, it’s no surprise that, despite the love fest people have for TiVo, it has only managed to sell a few million standalone boxes over the years, a relatively minor market impact. In fact, by far the majority of its market presence is through a deal with DirectTV, which contributes several million TiVo-enabled set-top boxes deployed. However, growth with DirectTV is over, with the company instead choosing to use technology from former sister company NDS instead.The sudden popularity of high definition TV brought yet another huge challenge for TiVo. Eventually, as consumers fully understand HD, they will all want an HD set-top box, capable of delivering real HD programming. Right on the heals of HD, people will want DVR features - of course HD-capable. Cable and satellite operators figured this out a few years ago and stepped up by offering their HD-DVR integrated set-top boxes for just a few extra dollars per month.

But TiVo only recently managed to release its own standalone HD-capable box, the "Series 3." And while the box is a marvel of product design, it weighed in with an $800 price tag, a price completely discordant for consumers whose expectations have been set by the fact that DVD players can now be had for as little as $13 at their local Wal-Mart. Coincidentally, it’s worth noting that just today TiVo announced a $300 version of the Series 3, which, while helping relieve upfront sticker shock, still requires the additional monthly service fees. And also the contorting, puzzling and glowering aspects of the installation process.

And Now for the Silver Lining in this StoryBy now you’re probably wondering how all of this doom-and-gloom is going to give way to the "Comeback Kid" scenario.In fact, the secret to TiVo’s success is, and has always been, jettisoning its hardware business model and becoming a software company. In other words, stop making boxes and instead just license the TiVo software to others whose boxes stand a better chance of being accepted by consumers (i.e. video providers). This was the vision from the start. I recalled reading a trenchant New York Times magazine piece that Michael Lewis (of Liar’s Poker and Moneyball fame) wrote 7 summers ago in August, 2000 on TiVo and Replay, its competitor at the time. I was able to dredge it up (thanks, Google) and in it, Jim Barton, TiVo’s co-founder, and current CTO plainly put it, "We’ll know we’ve succeeded when the TiVo box vanishes."

With TiVo’s promising, but ultimately unfulfilling deal with DirectTV unraveling, the company’s real potential to deliver on its vision lay with making deals with the cable industry. For a variety of reasons not worth recounting here, those deals proved elusive until early 2005 when TiVo struck a deal with Comcast. Things started looking even better for this game plan when the TiVo appointed Tom Rogers, who has significant cable bona fides, as CEO in mid-2005.

Flash forward 2 years later and it is looking increasingly likely that TiVo is on the cusp of executing its original strategy, positioning itself, at long last, for its moment in the sun.

TiVo + the Cable Industry, A Match Made in ARPU HeavenAs summer turns to fall, Comcast, by far the largest cable operator in the US and Cox, the third largest, are planning their initial rollouts of TiVo-enabled HD set-top boxes.After all these years, a more perfect time for TiVo and the cable industry to get together can scarcely be imagined. The incentives for these deals to succeed are very strong all around.

The cable industry is fighting hard to convince consumers to resist switching to Verizon and AT&T in the communities in which these telcos have rolled out their wizzy new video services. With telcos offering stiff price competition, ARPU (average revenue per unit) growth can only happen through new services, not price increases. Further, Comcast in particular has been working overtime to convince Wall Street that Video-on-Demand is its killer competitive advantage to satellite even while it struggles with its poorly-designed user interfaces which serve to impede, not assist, its subscribers’ discovery of valuable VOD programming.

Enter TiVo. TiVo offers Comcast/Cox/the cable industry one of the best-known and best-loved consumer brands with which to align itself on a de-facto exclusive basis. As mentioned, DirectTV’s deal is over. EchoStar’s relationship with TiVo is toxic due to mammoth patent litigation between the two companies. Verizon and AT&T barely have the resources to get their networks up and running much less take on the challenge of how to integrate their set-top boxes with TiVo software.

Meanwhile, the cable industry continues to grapple with how to get more consumers to sign on for digital cable service. Years after its introduction, digital still remains a sketchy value proposition for many. But TiVo gives cable operators a powerful feature to goose demand. Further, since Jeff showed how elegantly TiVo has incorporated VOD navigation and recording into its UI, integrated TiVo service also offers the promise of addressing that cable operators’ challenge in that area.

Last, but not least, on the assumption that TiVo service will carry an upsell charge of around $3-4 per month to the consumer (which are completely my estimates, with nothing having been disclosed by TiVo or its partners at this point), and assuming 2/3 of that goes to the cable operator, TiVo provides tantalizingly high-margin new ARPU growth for cable operators. Those high margins are made possible through the magic of OCAP, the cable industry’s new standard for remotely downloading applications like TiVo to tens of millions of currently-deployed set-tops (i.e. no expensive truck rolls).

That Sweet Sound of Ka-Ching, Ka-ChingTo help understand the revenue and margin potential of the cable deals for TiVo, consider the following:Pick your favorite analyst’s forecast for DVR growth. Forrester, for example believes that by 2011 there will be 65 million DVR homes, up from somewhere around 15-17 million today. So net adds of around 50 million homes. Comcast and Cox together pass about 58 million or 53% of all American homes. So their proportionate share of those 50 million DVR net adds should be at least 26 million. If they market the service right, it’s probably fair to assume that over time, at least 80% of DVR users are going to prefer the TiVo solution to cable’s crummy homegrown DVR alternative (if this option even survives). If so, then these deals’ potential is about 21 million homes taking the TiVo cable service by 2011.

Again, say the TiVo service costs an incremental $3 per month and then assume TiVo keeps a $1 of that, which is my approximation for the combination of its per sub and technology licensing fees. So, eventually 21 million new TiVo homes x $1 month x 12 months. Just from Comcast and Cox that would eventually total $252 million of annual revenue for TiVo. Now factor in when all the other cable operators smell the coffee and abandon their homegrown DVR solutions in favor of TiVo. And then of course it’s inevitable that TiVo will sign up Verizon and AT&T. However in those deals TiVo should be able to negotiate to keep maybe half the monthly fee instead of just a third as they did with the cable crowd (hey, it’ll be a proven service, plus the telcos will be playing catch-up, as usual).

To put all of this in context, for the fiscal year ending 1/31/07, TiVo’s revenues were $259 million, so if the Comcast and Cox deals alone succeed to even a fraction of their fullest potential, they should still have a major impact on the company’s financials. And bear in mind that if the cable strategy succeeds, then along the way TiVo’s retail hardware business would have been euthanized, erasing all that low margin box revenue. What would be left is a high-margin software licensing and services powerhouse, ready to go international, add portable applications and generate all kinds of new features, such ramping up its already solid broadband programming lineup.

But perhaps most important, with TiVo able to track the viewing behavior of all of those millions of homes, its long-held vision of building out an ad-based revenue business based on precise user viewing suddenly seems attainable. Of course it’ll be a little cheeky of TiVo to be pitching agencies and advertisers on these ad services after TiVo all but wrecked their traditional model with its ad-skipping features. But what choice will these folks really have if they want to succeed? And these meetings are already happening, and according to Jeff, who oversees all this, it sounds like all is forgiven and good progress is already being made.

What’s the Catch?The catch here is that initially TiVo is almost entirely dependent on Comcast and Cox putting enough marketing muscle behind this new service and executing it properly. So will Comcast and Cox do this? Though it’s way too early to tell, given all of the aforementioned incentives, there’s ample reason to believe that both will. For Comcast alone, which has borne the brunt of two years of arduous technical integration work with TiVo, failure to follow through with strong marketing would be a huge and embarrassing blunder. So I’m betting these savvy cable guys will get the marketing part right (if you’re really interested in how, keep scrolling to see the below Addendum for a couple of sample marketing scenarios).And if they do, then you heard it here first— TiVo is well-poised to become The Comeback Kid.

ADDENDUM: 2 MARKETING SCENARIOS FOR COMCAST

To make TiVo’s potential more tangible, consider the following 2 scenarios. In both cases you just bought a 42 inch LCD or plasma TV. Of course you now need an HD-capable set-top box. You call Comcast to order one and here’s what should happen:

Scenario 1: You own or have owned a TiVo Series 1 or 2 box

You’re told that an HD set-top will run you $5.00 more per month than your current box. Then you say you’re interested in DVR capability. "Ah," the Comcast rep says, "have you ever owned a TiVo?". You say "Yes." "Well", she continues, "did you know that you can now get the same (mostly) awesome TiVo service - including the familiar user interface, remote control and blooping sounds as you program the box AND have all Video-on-Demand programming expertly integrated into the service, only from Comcast? It is one of our most popular services, and I can offer it to you today for just another $8 more per month than the HD set-top box you want." You say, "let me get this straight, I’m already used to paying $13/month for my TiVo Series 2 service, so instead of paying that, I would pay $8 per month and get virtually all the same benefits of TiVo, but don’t have to go out and buy another TiVo box? And this isn’t the crummy DVR service I saw at my neighbor’s house that I know you also offer, right?" "No sir, it’s TiVo." "Any other sneaky upfront charges?" "No." "Any disconnect charges if I want to drop it?" "No." "Am I missing something here?" "No." "WOW, sign me up - what a great offer. Thanks Comcast."

Scenario 2: You’ve never owned a TiVo box, but you have some familiarity with the product because any number of friends, neighbors, relatives and co-workers have been bragging to you for years that it’s the greatest thing since sliced bread.

You’re told that an HD set-top will run you $5.00 more per month than your current box. Then you say, "I’m kind of interested in this whole DVR thing everyone keeps talking about." After the Comcast rep verifies you’ve never actually owned a TiVo, but that you’re sort of familiar with what it does, she says, "Well, Comcast has a very special offer for you. TiVo DVR service has become one of our most popular services and we think if you experience it for yourself, you’ll see why. So I’d like to offer you 90 days of free TiVo service. If you don’t like it, simply call us at any time and we’ll remotely remove it from your box. That means you don’t need to wait at home for a technician to disable TiVo service for you." You ask what it will cost per month and upon hearing the answer ($8 more per month than the HD box base rate) you make a mental note to ask your friends, neighbors, relatives how much they pay, to see what kind of deal you’re getting (later they’ll confirm it’s the same as they’re currently paying for their Series 1 or 2 monthly plans). You see no downside to trying it, so you do. After you and your family use TiVo for approximately 3 days, you all fall in love with it and wonder how you could have ever lived without it. You call Comcast to say thanks.

Categories: Cable TV Operators, Devices, Partnerships

-

Broadband Video Isn't Competition for Cable Says My CTAM Panel

Today I moderated a spirited discussion panel at CTAM NY’s annual Blue Ribbon Breakfast at Gotham Hall in NYC. The title was "Over the Top TV....Can Broadband Video Be Cable's Newest Opportunity?" We had an amazing group of panelists (click here to see list and listen to podcast) and with 450+ attendees a packed house as well.

A key question we dug into was whether and to what extent cable’s traditional (and highly successful) paid subscription model will be impaired by the rise of broadband video usage. Try as I did to see if any of the panelists believe that it will, none would admit to it. The reasons given included, "some form of a paid model will always exist but will never succumb entirely to a free, ad-supported model" to "cable networks won’t push broadband video distribution of their programs so hard as to upset the current model of receiving affiliate fees from cable operators", to "the low probability that inexpensive PC-to-TV bridge devices will proliferate any time soon" to "viewers have shown that they want a selection of channels to browse."

While I think each of these answers is quite legitimate, my point of view is that we are in the early days of an fundamental transformation in the video (and indeed the media more generally) business that will eventually (though of course who knows when and to what eventual degree) see most, if not all programming get unbundled into a fully on-demand paradigm.

I believe the ultimate answer to how cannibalistic broadband is toward cable ultimately turns on whether consumers believe it’s a "zero sum" game, meaning they choose between EITHER accessing programs via a VOD or DVR offering only available if they’ve bought into a monthly multi-channel video subscription (that’s to say the way the world works today) OR if they opt out of that subscription offering and INSTEAD choose to buy these programs a la carte, or receive them free, courtesy of a highly targeted ad model. The opt out option would of course be available through open broadband video distribution.

All trends point to the latter ultimately prevailing. While cable operators are well-positioned to shift their models to exploit this behavior if they act aggressively, they are also vulnerable to it if they don’t. The most important driver of the "opt out" scenario is that for an increasingly larger portion of our society, their behavior and expectations are formed by the Internet. And the ‘net is a completely personalizable and on demand medium. Especially for most online media, it is also mainly free, or paid on a fully a la carte basis (e.g. iTunes). Users’ expectations are through the roof and only getting higher. As broadband proliferates they will bring these same expectations to their decision-making.

Is it really realistic to believe that in 5 years when today’s MySpace/Facebook/YouTube/iTunes crazed 16 year old kid goes to set up his/her first apartment, s/he is going to embrace the notion of subscribing to a hundred channel package just so s/he can watch a handful of programs on demand? And of course, the ‘net’s behavior change isn’t confined to kids, it’s pervasive across all age groups.

Cable operators have an outstanding opportunity to capitalize on these macro behavioral trends. But doing so will require cable operators to make a significant and risky departure from their traditional subscription-based business models. It’s a classic incumbent’s dilemma. It will be interesting to see if they can do so.

Categories: Aggregators, Cable Networks, Cable TV Operators, Events, Indie Video

Topics: Comcast, Cox, CTAM NY, Discovery, Google, Next New Networks

-

CTAM NY Blue Ribbon Breakfast is On Tap

I'm really looking forward to moderating the CTAM NY chapter's annual Blue Ribbon Breakfast on Wednesday morning at Gotham Hall. The session is entitled, Over the Top TV....Can Broadband Video Be Cable's Newest Opportunity?"

I'm really looking forward to moderating the CTAM NY chapter's annual Blue Ribbon Breakfast on Wednesday morning at Gotham Hall. The session is entitled, Over the Top TV....Can Broadband Video Be Cable's Newest Opportunity?"We have a world-class group of panelists:

- Bruce Campbell, President, Digital Media and Business Development, Discovery Communications

- Dallas Clement, Senior Vice President, Strategy & Development, Cox Communications

- David Eun, Vice President, Content Partnerships, Google

- Herb Scannell, CEO & Co-Founder, Next New Networks

- Matt Strauss, Senior Vice President, New Media, Comcast

The event has been sold out for 2 weeks and CTAM just figured out a way to shoehorn in another 25 people from the waitlist, bringing the overall attendance to 460+.

It's going to be an amazing event. The cable industry – both operators and programmers – are right in the middle of the whole broadband video revolution. Their actions will have a big impact on the course and pace of the industry's future.

CTAM is recording the event to podcast it, and I'll be sharing my observations in this space as well.

Categories: Events

Topics: Comcast, Cox, CTAM NY, Discovery, Events, Google, Next New Networks

Posts for 'Cox'

|

Connect with VideoNuze

Exclusive News Roundup

- Paramount+ is building out a free tier to lure cost-conscious viewers Business Insider

- Amazon is redesigning Prime Video with more AI, but will it fix what frustrates viewers? Digital Trends

- Peacock Finally Turns a Profit Ahead of NBCUniversal Split The Wrap

- YouTube Ad Sales Keep Growing at Healthy Clip, Rising 13% to $11 Billion in Q2 Variety

- 'Creator' Content Now 26% Of Time Spent With TV/Video Mediapost

- Netflix Paid $587 Million for Ben Affleck’s AI Company The Hollywood Reporter