-

Research: NFL is Strongest For Live Sports Viewers On Devices

Adobe Primetime and The Diffusion Group have released new research, finding among other things, that the NFL is the most popular sport to live stream on digital devices. The research surveyed 2,000 U.S. consumers, revealing viewership trends for live sports viewers or “LSVs” - adult broadband users that watch televised live sports on any screen including PCs, TVs, smartphones or tablets.

The survey found that 37% of LSVs watch live sports on non-TV devices, with PCs used the most (cited by 27%), followed by smartphones (17%) and tablets (14%). Across all 3 of these devices, the NFL is the most popular of all sports. On PCs NFL is watched by 66% of LSVs, followed by Summer Olympics (59%) and NBA basketball (59%). On smartphones, NFL is watched by 70% of LSVs, then NBA (59%) and college basketball (52%). On tablets NFL is at 67%, followed by NBA (62%) and major league baseball (61%).Categories: Live Streaming, Sports

-

Just 7% of TV Everywhere Users Cite Authentication as Main Challenge

Industry research firm The Diffusion Group has found that, contrary to conventional wisdom, authentication is not blocking broader consumer acceptance of TV Everywhere services. TDG found that just 7% of TVE users perceive the TVE authentication process as "difficult" to "very difficult" while over two-thirds (68.4%) said it was "easy" to "very easy." Nonetheless, 82% of TVE users said eliminating TVE log-in entirely would be an important enhancement.

Categories: TV Everywhere

Topics: TDG, TV Everywhere

-

LG and Clearleap Partner for Video Delivery to Smart TVs As Usage Heats Up

LG and technology provider Clearleap announced a partnership that will give pay-TV operators the ability to deliver video services directly to Smart TVs over broadband IP networks. Under the deal LG will integrate Clearleap's Stream On Demand solution into its Smart TVs, so that pay-TV operators can provision VOD and online video without the need for an ancillary set-top box. Clearleap has previously partnered with Roku and has also extended its capabilities to the iPad and connected Blu-Ray players.

The big advantage to pay-TV operators of these deals is that they can serve subscribers without expensive set-top boxes and truck rolls. Services can also be extended to rooms in homes that didn't traditionally have pay-TV service, increasing the value of the underlying subscription.

Categories: Devices

-

Webinar Tomorrow: Boosting VOD Revenue and Engagement Through Enhanced Content Discovery

Even as the range of new over-the-top connected devices brings consumers an explosion of new video choices, incumbent pay-TV operators have continued building viewership of their own video-on-demand (VOD) offerings. But, as Colin Dixon, Senior Partner at The Diffusion Group, a digital media research firm, argues in a new white paper, the vast majority of this viewership has been of free content, effectively leaving pay-TV operators out of the burgeoning rental and download markets. A key reason for this has been sub-optimal electronic program guides (EPGs).

In a complimentary webinar tomorrow at 11am PT / 2pm ET titled "The Social TV Guide: Boosting VOD Revenue and Customer Engagement Through Enhanced Content Discovery," Colin will lay out both the opportunity and specific tactics for how providers can improved their VOD offerings. Colin will be joined by Sefy Ariely, VP of Sales and Marketing for Orca Interactive, which makes content navigation software. The data and lessons that Colin will share is applicable not only to pay-TV operators, but to anyone offering online and mobile video options trying to drive higher usage and revenue.

Categories: Events

Topics: Orca Interactive, TDG

-

Webinar Highlights - Indie Online Video, Syndication and Brand Integration

On Tuesday, VideoNuze and The Diffusion Group hosted their fourth webinar in a 2010 series of six sponsored by ActiveVideo Networks, with this one focusing on "Demystifying Independent Online Video and Syndication Models."

The webinar featured informative and timely discussion/Q&A with Richard Bloom, SVP, Business Development for 5min, and Jim Louderback, CEO of Revision3. The focus of the discussion was on business models for success in independent online video with a specific lean towards syndication. Both Jim and Rich honed in on how syndication helps solve the difficulties with finding eyeballs and building audience in the fragmented broadband video landscape.

Categories: Advertising, Events

Topics: 5Min, ActiveVideo Networks, Revision3, TDG, Webinar

-

Webinar Today: Independent Online Video and Syndication

Please join The Diffusion Group and VideoNuze today at 11am PT/2pm ET when we will present the fourth complimentary webinar in our 2010 "Demystifying" series, with this session's focus on demystifying independent online video and syndication models. The series is exclusively sponsored by ActiveVideo Networks.

TDG's Colin Dixon and I will be hosting and moderating the webinar, which will include guests Jim Louderback, CEO of Revision3, and Rich Bloom, SVP of Business Development for 5Min. Jim and Rich will each do short presentations and then we'll have moderated Q&A followed by plenty of time for audience Q&A.

Jim and Rich will cover what's working for their companies and what's in store for the broader online video industry going forward. If you're an independent video producer, or part of an established media company looking to succeed in the online medium, this webinar is for you!

Click here to learn more and register about this complimentary webinar

Categories: Events, Indie Video, Syndicated Video Economy

Topics: 5Min, ActiveVideo Networks, Revision3, TDG, Webinar

-

Webinar Next Tuesday, Aug. 24th: Independent Online Video and Syndication Models

Next Tuesday, Aug. 24th, The Diffusion Group and VideoNuze will present the fourth complimentary webinar in our 2010 "Demystifying" series, with this session's focus on demystifying independent online video and syndication models. The series is exclusively sponsored by ActiveVideo Networks.

Once again, TDG's Colin Dixon and I will be hosting and moderating, and we have two terrific guests joining us, Jim Louderback, CEO of Revision3, a leading Internet-only television network, and Richard Bloom, SVP of Business Development for 5Min, a leading syndication platform for instructional and lifestyle videos. Jim and Rich will each do short presentations and then we'll have moderated Q&A followed by plenty of time for audience Q&A.

Our webinar couldn't be more timely; with online video viewership exploding (comScore reported 5.3 billion total viewing sessions in July) and myriad connected devices leveling the playing field for on-TV viewing, web producers have lots of opportunity ahead of them.

Categories: Webinars

-

Complimentary Webinar Tomorrow, July 8th: Demystifying Open vs. Closed Internet Video Distribution Platforms

Please join me for a complimentary webinar tomorrow, July 8th at 11am PT/2pm ET, as Colin Dixon, senior partner at research firm The Diffusion Group, and I debate the topic of closed vs. open Internet video distribution. Colin and I have both been watching closely all the different devices that are bridging online video to the TV. There are many different devices and many different approaches.

One key difference is the idea of "closed" vs. "open." In the "closed" experience only certain content is available, while in the "open" approach anything that's available on the Internet becomes available on the big screen. There are pros and cons to each approach. Which is more likely to ultimately succeed? Colin and I will do our best to demystify the issues and forecast what's most likely to work. There will be plenty of time for audience Q&A. Please join us for this timely complimentary webinar!Categories: Events

-

Complimentary Webinar: Demystifying Open vs. Closed Internet Video Distribution

Please join me for a complimentary webinar next Thurs, July 8th at 11am PT/2pm ET, as Colin Dixon, senior partner at research firm The Diffusion Group, and I debate the topic of closed vs. open Internet video distribution. Colin and I have both been closely watching the myriad initiatives to bring online video to big-screen TVs. There seems to be no end to the number of devices and consumer electronics manufacturers jumping into this exciting space.

Yet there are plenty of differences in the approaches players are taking. Some are offering a relatively "closed" experience with only certain content being made available. On the other hand, some advocate for a wide open approach - meaning anything that's available on the Internet should be available on the big screen.

Is one approach better than the other, and will one meet with more success? There are a host of questions surrounding this debate and Colin and I will do our best to demystify the issues and forecast what's most likely to work. There will be plenty of time for audience Q&A. Please join us for this timely complimentary webinar, sponsored exclusively by Active Video Networks!

Learn more and register now

Categories: Events

-

Complimentary Webinar on Monday, April 8th: "Demystifying Free vs. Paid Online Video"

Please join Colin Dixon, senior partner at The Diffusion Group and me for a complimentary webinar on Thursday, April 8th at 11 am PT/2pm ET titled "Demystifying Free vs. Paid Online Video." We will be joined by two special guests, Chris Wagner, EVP, Marketplace Strategy of NeuLion, a leading provider of technology and services to content owners and aggregators, and Jason Krebs, EVP of ScanScout, a leading video ad network.

Learn more and register now for this complimentary webinar

In this webinar we will examine all sides of the debate including the effectiveness of online subscription models, how well online video advertising is taking advantage of the Internet's unique interactivity/engagement, the pending influence of "TV Everywhere" rollouts and much more. Chris and Jason will share best practices and insights based on their companies' experiences. Colin and I will ask them questions and then open up the webinar for plenty of audience Q&A. If you're trying to get your head around online video business models, then this webinar will be a high-impact educational opportunity.

The webinar will also be a terrific lead-in session for many of the issues we will drill into 2 1/2 weeks later at the "VideoSchmooze" Broadband Video Leadership Evening in NYC on Monday, April 26th. The title for the panel at VideoSchmooze is "Money Talks: Is Online Video Shifting to a Paid Model?" Early bird discounted tickets are now available and I hope you'll be able to join us for both the webinar and VideoSchmooze.

This webinar is the 2nd of 6 in the "Demystifying" series that TDG and VideoNuze are presenting in 2010, sponsored exclusively by ActiveVideo Networks.

Categories: Events

Topics: NeuLion, ScanScout, TDG, VideoSchmooze, Webinar

-

Sezmi is Slick; Marketing It Will Be the Big Challenge

While in LA this week, I caught up with Phil Wiser, Sezmi's president and co-founder and got another good look at the Sezmi service, which just officially launched in the entire LA market with Best Buy. I've been covering Sezmi for over 3 years, and from a technical and product standpoint, I continue to be impressed with what it has accomplished, especially for a 1.0 launch. Out-of-the box set up is very straightforward and a series of intuitive menus quickly creates a personalized user profile complete with recommended shows based on your interests and selections from linear and on-demand channels.

Sezmi gained my attention early on because unlike other broadband-only devices (e.g. Roku, Vudu, ZillionTV, AppleTV, gaming consoles, etc.), Sezmi's goal has always been to become a full replacement for existing multichannel video programming distributors ("MVPDs"). That "boil the ocean" strategy has

required it to develop its own hybrid broadcast/broadband content delivery system, sign up local broadcasters for access to their bandwidth, ink carriage deals with cable networks and design the user experience from scratch, among other things. Having done much of that work (with a key exception being to still get the remaining cable channels from Disney/ESPN, Fox, Scripps and A&E into the line-up), Sezmi's next challenge is to actually market the service and add subscribers cost-effectively. This could well prove to be Sezmi's biggest challenge.

required it to develop its own hybrid broadcast/broadband content delivery system, sign up local broadcasters for access to their bandwidth, ink carriage deals with cable networks and design the user experience from scratch, among other things. Having done much of that work (with a key exception being to still get the remaining cable channels from Disney/ESPN, Fox, Scripps and A&E into the line-up), Sezmi's next challenge is to actually market the service and add subscribers cost-effectively. This could well prove to be Sezmi's biggest challenge.The market for multichannel video subscriptions has never been more competitive than it is today. Deep-pocketed cable operators, satellite operators and telcos (and in some places 3rd party "overbuilders" like RCN) are beating the hell out of each other in many U.S. geographies. For example, here in the Boston area we're bombarded daily with ads on radio, in newspapers, in direct mail, through door-hangers and other means, to switch providers. While there are a lot of noisy promotional offers, there are plenty of product and technology-based pitches as well - more HD channels, faster broadband speeds, better VOD and so on. The "triple play" bundle of video, voice and data is a significant marketing lever. I don't know what the marketing cost per acquired customer is for Comcast or Verizon these days, but I have no doubt it has never been higher.

This is battleground that Sezmi is now entering after nearly four years of development. Many people are skeptical about Sezmi's odds of success (read TDG president Michael Greeson's well-done piece from last week for a rundown of the issues), at least as Sezmi is currently configured. Some of these concerns are very valid, in particular Sezmi's $299 upfront equipment fee (which is pretty much unique in the industry), its currently incomplete channel lineup (note also that HBO, Showtime and Starz are also not available) and the $20/mo rate which is marginally better than alternatives (but is likely to increase anyway as more channels and especially expensive ones like ESPN are added).

No question, Sezmi faces a steep marketing challenge. Still, I believe there are reasons for optimism. First, as Sezmi has said many times, it is not a box company and Best Buy isn't its only route to market. It plans deals with telco and ISP partners who will not only bundle its pricing but also erase the upfront charge through a rental model. The rental could be very aggressive depending on the partner's goals, opening up more pricing competitiveness for Sezmi. Second, Sezmi's user interface and certain product features are very compelling differentiators. Granted, incumbent MVPDs are not standing still (see Cablevision's "Media Relay" announcement just yesterday), but the fact that Sezmi owns its whole system from end to end gives it more control and flexibility to enhance the product (for example in VOD it is not relying on traditional vendors).

Lastly, and I'll admit this is where things get fuzzy, but I do think there's a segment of existing MVPD customers who hunger for something new, better and lower cost than is currently available. I've made the analogy for Sezmi to what JetBlue has done in the airline industry and I think that still holds. Depending on how distinctive Sezmi's positioning and messaging is, I think it could really resonate with younger, urban, tech-savvy users. One Sezmi feature alone - access to all YouTube videos - is a totally new value proposition. Phil and I quickly searched YouTube yesterday for "Alec Baldwin Hulu Super Bowl Ad" and in seconds there it was. Can any other MVPD offer that today?

There are plenty of reasons to discount Sezmi's chances of success, but I think that's premature thinking, especially given how dynamic the video landscape is today. But even if Sezmi doesn't thread the needle and fully surmount the marketing challenges ahead, the company still has a lot of value in its technology and products. If Vudu fetched a reported $100 million from Wal-Mart, and Sling got $380 million from DISH as announced a couple years ago, then there should be a palatable financial exit in store for Sezmi as well, even with $75 million or so invested to date. Of course its investors and executives are hoping for far more than just a "palatable" final chapter. The real test of what's in store for Sezmi is just now beginning.

What do you think? Post a comment now (no sign-in required).

Categories: Cable TV Operators, Satellite, Telcos

Topics: Comast, SezMi, Sling, TDG, Verizon, VUDU

-

Join Me for Net Neutrality Webinar with TDG Tomorrow, Feb. 4th

Please join me for the complimentary "Demystifying Net Neutrality" webinar tomorrow, Thurs, Feb. 4th at 11am PT / 2pm ET. This is the first of six webinars VideoNuze is presenting in 2010, in partnership with The Diffusion Group, one of the leading digital media research firms. The webinars are sponsored exclusively by ActiveVideo Networks

TDG's Colin Dixon and I will host the webinar, and we will have 2 expert guests with us who are on opposite sides of the net neutrality debate: Barbara Esbin, Senior Fellow and Director, Center for Communications and Competition Policy, Progress & Freedom Foundation (against) and Chris Riley, Policy Counsel for Free Press (for). Barbara and Chris will advocate their positions and then Colin and I will question each of them before opening it up to audience Q&A.

The webinar promises to be a deep-dive educational session examining all of net neutrality's pros and cons. For anyone with a stake in broadband/online content delivery and over-the-top video specifically, it will be a must attend session.

Categories: Broadband ISPs, Regulation, Webinars

Topics: Net Neutrality, TDG, Webinar

-

2 Complimentary Upcoming Webinars

I'll be participating in 2 complimentary upcoming webinars that will be of interest to VideoNuze readers.

First, on Thurs, Sept. 24th, Colin Dixon, Senior Partner at The Diffusion Group and I will present "The Terror of Terminology: Demystifying Broadband TV." Colin is one of the smartest broadband analysts around, and we periodically compare notes on the market. In an effort to clarify some of the confusion we continually hear around certain terminology in the market, we're going to discuss 5-6 different concepts and try to clear away the fog. Expect a fun and educational conversation, with plenty of time for audience Q&A. Learn more and register.

Then on Wed, Sept. 30th I'll be participating in a Brightcove-sponsored webinar, "New Video Distribution Strategies - Taking Video Beyond the PC." Other speakers include Chris Little, Technology Director at Brightcove and Rich Ezekial, Director of Strategic Partnerships, Connected TV, Yahoo. Accessing online video on other devices like TVs and smartphones is one of the hottest areas of the broadband video landscape, and we'll be digging in to key trends, best practices and monetization opportunities. In particular, we'll hear specifics about Yahoo's Connected TV strategy. Learn more and register.

I look forward to seeing you on one or both of these exciting webinars!

Categories: Events

Topics: Brightcove, TDG, Yahoo

-

4 Items Worth Noting from the Week of August 3rd

Following are 4 items worth noting from the week of August 3rd:

1. Research, research, research - For some unknown reason, there was a flurry online video-related research and forecasts released this week. In no particular order:

eMarketer was out with a new forecast indicating 188 million online video viewers in the U.S. in 2013.

Veronis Suhler released its forecast of 2009-2013 communications industry spending, showing advertising shrinking as a percentage of total spending.

PWC's UK office released its 2009-2013 forecast, which also anticipates declines in advertising.

CBS's research head David Poltrack used detailed data to explain the company's online video strategy and buttress its argument that in a TV Everywhere world, it should be compensated for its content (slides are here, via PaidContent).

Ipsos found that Americans streamed a record amount of TV programs and movies, doubling their consumption from Sept '08 to July '09.

Yahoo and a group of research partners released data finding that 70% of online video consumption happens throughout the day and night, as opposed to traditional TV viewing which is concentrated in the prime-time window.

Last but not least, TDG released excerpts of its research on "over-the-top" video services, available for download at VideoNuze.

2. Unicorn Media launches, hires ex-Move Networks executive David Rice - It will be hard for some to believe there's room for yet another white label video publishing and management platform, but startup Unicorn Media is going to try elbowing its way into the crowded space, with a specific focus on large media companies. I spoke with Unicorn's executive team this week, led by Bill Rinehart, who was the founding CEO of Limelight.

Unicorn is positioning itself as the first "enterprise-grade" solution, staking out key differentiators such as enhanced analytics/reporting, faster/easier transcoding, improved APIs for content ingest/management and more flexible monetization/ad queuing. I have not yet seen a demo, but I'm intrigued by what I heard. The company has raised $5M to date from executives/angels and has a staff of 25. David Rice, formerly Move's VP of Marketing has come on board as Chief Strategy Officer. Given the team's industry expertise and relationships, this could be a company to watch.

3. Google acquires On2 Technologies and other encoding-related news - The blogosphere was in a flurry about Google's $106M acquisition of video compression provider On2 Technologies this week. Speculation flew about Google open-sourcing On2 new VP8 codec, which could potentially force a new standard to emerge as a challenge to H.264, today's leading codec. This is important stuff, though a little further down the stack than I usually focus, so I refer you to Dan Rayburn's analysis of the deal's implications, which is the best I've seen.

There was other news in the emerging cloud-based encoding/transcoding/delivery market this week, as Encoding.com announced a new premium service with tighter service level agreements (4 minute max wait time and 50 Gbyte/hour/customer throughput). Encoding.com's Gregg Heil and Jeff Malkin explained the company is using the new SLAs to move upmarket to service tier 1 and 2 media companies. Separate, Encoding.com's competitor mPoint's CEO Chiranjeev Bordoloi told me they're now on a $3M annualized revenue run rate as cloud-based alternatives continue to gain acceptance.

4. Don't try this at home - On a lighter note, there's been no shortage of knuckle-head stunt videos we've all seen online, but this one is near the top of my personal favorite list. Do NOT try replicating this over the weekend!

Categories: Deals & Financings, Technology

Topics: CBS, eMarketer, Google, Ipsos, ON2, PWC, TDG, Unicorn Media, Veronis Suhler, Yahoo

-

New Complimentary TDG Research on Over-the-Top Video Services

Continuing a past VideoNuze practice of making key data available from industry research firms, today I'm pleased to provide a dozen excerpt slides from The Diffusion Group's recent study, "Consumer Interest in

OTT Video Services." TDG is one of the leading firms studying broadband adoption and shifting video consumption habits (and is also a long-time VideoNuze partner). These slides are from TDG's Q1 '09 proprietary survey of 2,000 U.S. adults, the results of which have only been shared with its paying clients to date.

OTT Video Services." TDG is one of the leading firms studying broadband adoption and shifting video consumption habits (and is also a long-time VideoNuze partner). These slides are from TDG's Q1 '09 proprietary survey of 2,000 U.S. adults, the results of which have only been shared with its paying clients to date.Click here to download the slides

"Over-the-top" is an industry term for any video provider (e.g. free, paid, on-demand, live, streaming, etc.) using the broadband infrastructure of an unaffiliated ISP to reach their intended audience. Since most broadband ISPs are either cable companies or telcos who also offer their own subscription multichannel video services, the idea is that these new services (e.g. Netflix, YouTube, Hulu, Amazon VOD, etc.) are provided "over-the-top" of these broadband/video incumbents, directly to broadband-enabled audiences.

With the proliferation of convergence devices (e.g. Roku, Xbox, AppleTV, etc.) OTT video is increasingly getting all the way to viewers' TVs. Many of you have heard me talk about how powerful and unprecedented broadband's "openness" is in the traditionally tightly controlled video industry. Like the Internet itself, broadband's openness is foundational; it has enabled a totally new and free-flowing relationship between video content providers and viewers.

There's been no shortage of buzz that OTT providers could disrupt the multibillion dollar per year subscription TV business, enticing subscriber's to "cut the cord" on incumbent cable/telco/satellite providers. I've weighed in multiple times on the likelihood of cord-cutting, originally laying out my arguments last October in "Cutting the Cord on Cable: For Most of Us It's Not Happening Any Time Soon." With cable's TV Everywhere services now gaining steam, I think the likelihood of cord-cutting en masse is even more remote.

Nonetheless OTT remains a genuine long-term threat for many good reasons. So TDG's survey is a welcome effort at quantifying consumers' potential interest in OTT services, at various price points and in multiple types of offerings. TDG identifies 4 audience segments: "Replacers," "Supplementers," "OTT Optimals," and "Non-OTT Consumers." The survey tests demand for paid OTT services at various price points, revealing each segment's willingness to pay. Each segment is motivated by different reasons, meaning that OTT service providers are going to have to be very disciplined about understanding who exactly they're targeting and how to generate appeal.

No doubt there will be plenty more research on OTT and cord-cutting yet to come. For anyone thinking about these market opportunities, I think the TDG research is very useful.

Categories:

Topics: TDG

-

March '08 Recap - 3 Key Themes

As I mentioned at the end of February, each month I plan to step back and recap a few key themes from recent VideoNuze posts. Here are three from March '08. (And remember you can see all of March's broadband news, aggregated from across the web, by clicking here)

The Syndicated Video Economy: An Introduction

In March I introduced the concept of the "Syndicated Video Economy" ("SVE") to describe how the broadband video providers are increasingly coalescing on a strategy for widespread distribution of video through myriad outlets. In the SVE media companies shift their focus from "aggregating eyeballs" in a centralized destination to "accessing eyeballs" wherever (and whenever) they live. The SVE is a big departure from traditional tightly-controlled, scarcity-driven distribution approaches. Investors have responded by funding SVE-oriented content and technology startups.

In March I provided several examples of SVE initiatives. CBS launched its Local Ad Network to distribute content to local bloggers and web sites. 60Frames, a new broadband studio, is explicitly focused on partnerships for distribution, and is not even building destination web sites for its programs. And FreeWheel is developing management tools so that content can be optimally monetized across a content provider's sprawling network of syndication partners.

The SVE resonated strongly with VideoNuze readers; many are focused on it and vested in its further development. Expect to hear a lot more about the SVE from me in coming posts. I'll also have supporting slides I'm developing for upcoming webinars on the topic.

Over-the-Top: Getting Broadband Video to the TV

Bringing broadband video all the way to the TV by bypassing existing service providers (so-called "over-the-top") continues to be the big elusive prize for many. This past month YouTube and TiVo announced a partnership to let a subset of TiVo owners gain full YouTube access on their TVs, a welcome move.

Following that, in "YouTube: Over-the-Top's Best Friend" I suggested the YouTube, with its dominant market position and brand loyalty could in fact be the linchpin to over-the-top devices gaining a foothold with consumers. Google-YouTube executives' vision for YouTube as a video platform, powering experiences wherever they are, lends support to my proposition. Lastly on over-the-top, new contributor Michael Greeson, founder of market researcher TDG, proposed that adapting low-cost devices like DVD player may well be the best way to bridge broadband and TV.

Social media and video: 2 sides of the same coin

This past month also continued an escalation of interest in the intersection of social media and broadband video. At the Media Summit there was intense focus on engagement, and how broadband can uniquely create new user experiences that deeply involve the user. These social experiences include sharing, personalization, commenting, rating and so on. In this vein, Maginfy.net introduced new social features to support its specialized user-created channels, a smart evolution of its product.

And in a follow-up to "The Intersection of UGC and Brand Marketing?" I clarified the opportunities that brand marketers may or may not have to get involved with this hot space. For those interested in more on this subject, new VideoNuze sponsor KickApps provided an informative webinar which is still available here.

So that's March's recap. There will be plenty more on all of these and other broadband video topics in April and beyond!

Categories: Brand Marketing, Devices, Syndicated Video Economy, Video Sharing

Topics: 60Frames, CBS, FreeWheel, KickApps, Magnify.net, Media Summit, Syndicated Video Economy, TDG, TiVo, YouTube

-

Words Matter: Rethinking Messaging for Home Networks

I am pleased to welcome Michael Greeson's second contribution to VideoNuze. Michael is president of The Diffusion Group, a leading analytics and advisory firm helping companies in the connected home and broadband media markets.

Words Matter: Rethinking Messaging for Home Networks

Michael Greeson, President, The Diffusion Group

Since its arrival in the consumer market earlier this decade, the home network has been envisioned as a linchpin for the delivery of all types of IP-based residential services including video, data, entertainment, control, and communications. Despite this lofty vision, however, home network diffusion has fallen far short of expectations. Why has this happened?

For mainstream consumers, the phrase "home network" still spurs comments such as "never heard of them," "sounds too complex for me," or (worst of all) "don't see much value in having one." So how can these perceptions be changed? Here are a few thoughts that, while far short of being exhaustive, are no doubt relevant to this discussion.

(1) Ease-of-use must be a common property of every device and service. We've been talking about plug-and-play forever yet we're light-years away from making it a reality. A "solid-state experience" is essential to mainstream diffusion, meaning that home networks must be as easy to connect and use as yesterday's consumer electronics.

(2) There must be a compelling array of benefits uniquely enabled by home networking such that consumers feel they must have one. In this area, bridging broadband video directly to the TV could be particularly valuable.

(3) Market messages must reject the language of networking - in other words, stop calling it a "home network."

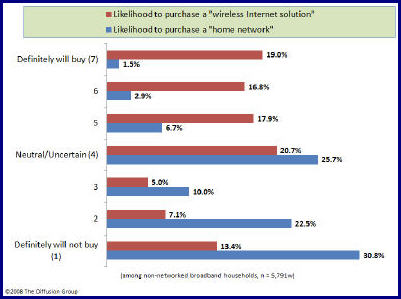

This last aspect is especially important, for regardless of how the technology and cost structures improve, if marketers aren't crafting their messages in language that speaks to consumers, all this innovation is for naught. To give you an example of just how important the issue of messaging is for the future of home networks, consider the following. During a recent national survey we conducted, consumers were informed of what a home network is and does (and in very simple language), then asked how likely they would be to purchase a home network in the next six months. The phrase "home network" was used three separate times in the description. The result? Only 11.1% expressed any degree of interest, with only 4.4% being highly or extremely likely to purchase.

Right after this first question, we asked their interest in purchasing a solution that enabled them to wirelessly connect their desktop and notebooks PCs to the Internet from any room in their home - we didn't use the phrase "home networking" nor did we explain in any detail the virtues of owning a home network. We simply asked about the likelihood that they would purchase a "wireless Internet solution" sometime in the next six months. The results? More than 54% expressed an interest in purchasing, with 36% being highly or extremely likely to purchase. That's a five-fold increase in total interest and an eight-fold increase in high levels of interest - simply by removing the phrase "home network" and focusing on one particular application that we believed to be of primary importance to today's consumer.

Think of it this way: I might have no interest in a home network (assuming I actually know what a "home network" is and does), but I am extremely interested in an inexpensive, easy-to-set/easy-to-use solution that allows me to wirelessly connect to the Internet regardless of where I am in my home. This may be particularly true for mainstream apps like video.

Whether in marketing CE devices or political candidates, sometimes we need to be reminded of just how much words do matter.

Click here to learn more about TDG's new report, "The Future of Home Networks"

Categories: Devices

Topics: Home Networks, TDG

Posts for 'TDG'

|

Connect with VideoNuze

Exclusive News Roundup

- Peacock Brings Starz to the Platform as First-Ever Add-On Subscription CNET

- Willy Wonka Competition Show at Netflix Uses AI to Re-Create Gene Wilder’s Voice The Hollywood Reporter

- Peacock Ad-Free Tier Launches On YouTube Primetime Channels As Part Of 2025 Distribution Deal Deadline

- Microdramas, Often Dismissed as Lowbrow Curiosities, Eye the Mainstream NY Times

- YouTube Shorts are getting even shorter with an update that lets you double the playback speed TechCrunch

- TikTok and YouTube are reinventing sports viewership. Broadcasters are taking note CNBC