-

thePlatform Unveils New "mpx" Beta and mpx Dev Kit

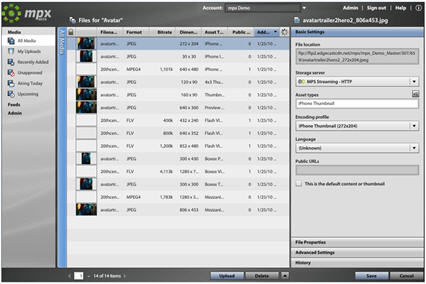

This morning, thePlatform is marking its 10th anniversary by unveiling a new version of its video management and publishing system, dubbed 'mpx" (the prior version was called "mps" for Media Publishing System) and mpx Dev Kit, a complete set of APIs and documentation. Last week Marty Roberts, thePlatform's VP of Marketing, gave me an overview of mpx and a short demo.

thePlatform had 3 primary customer goals in mind with mpx: (1) to provide more efficient management of large content libraries, (2) to enable personalized work flow options and (3) to re-orient the publishing process so

the beginning point is the outlet or "publishing profile." As Marty explained, over the course of the 10 years that thePlatform has been in business, the world of online video has become far more complex, with longer viewing durations, more distribution options, bigger content libraries, and more money at stake. Since thePlatform works primarily with big content providers and distributors, improving the ingest process to accept multiple simultaneous files, and then the navigation of existing files, was a key focus of mpx's development.

the beginning point is the outlet or "publishing profile." As Marty explained, over the course of the 10 years that thePlatform has been in business, the world of online video has become far more complex, with longer viewing durations, more distribution options, bigger content libraries, and more money at stake. Since thePlatform works primarily with big content providers and distributors, improving the ingest process to accept multiple simultaneous files, and then the navigation of existing files, was a key focus of mpx's development.In addition, having done lots of research on how its users interacted with mps, thePlatform found that they each used it in somewhat different ways and that ease-of-use remained a pain point. This led thePlatform to devote substantial resources to enabling users to create their own work flows, personalized depending on their specific role in the video management and publishing process. In the demo, Marty showed how different people, tasked with different assignments, could configure their own views of mpx's 3-pane publishing console, so that just those things they cared about were visible and accessible. Multiple views can be created and then saved, so the user can quickly return to and cycle through their various tasks.

Most interesting though, is mpx's re-orientation to start the publishing process by creating a "publishing profile" such as a pre-configured video player, or a mobile device, or a third-party syndication partner. In each case, the user first configures the outlet and then specifies exactly what types of assets are required, including encoding specs, formats, sizes, etc. Then, as video is ingested and marked for its destination, the system takes over and automatically runs the various required processes in order to deliver the required files to their destination. The same occurs for assets already in the system; the user finds what's required, associates a publishing profile and prompts the system to run the processes. It's a pretty slick approach, and no doubt will be a real time-saver for users.

Marty explained that thePlatform dedicated 70% of its engineering team to mpx's development for the last 2 years. Scale and reliability have also been key goals, as the company's large customers, especially service providers, have "5 9's" or 99.999% availability requirements. While thePlaftorm is cognizant of the range of online video platform competitors, the company believes the lessons learned over the years, which help it operate at huge scale, are a real differentiator.

Interestingly, Marty echoed what I continue to hear - that homegrown systems are still the most significant competition. However, the advent of TV Everywhere and the rise of paid media appear to be tipping these holdouts toward third-party platforms. With the online and mobile video worlds getting more complex by the day, this can be expected to continue.

What do you think? Post a comment now (no sign-in required).Note- thePlatform is a VideoNuze sponsor.Categories: Technology

Topics: thePlatform

-

It's Official: Netflix Has Entered a "Virtuous Cycle"

Looking at Netflix's Q4 '09 and full year '09 results released late last Wednesday, plus Netflix's performance over the last 3 years, I have concluded the company has officially entered a "virtuous cycle." For those of you not familiar with the term, a virtuous cycle is when a single change or improvement leads to a cascading series of follow-on benefits which both reinforce themselves and add further momentum to the original change (a hyper "one good thing leads to another" scenario, if you will). Virtuous cycles are extremely rare in business, and when they happen they have profound implications.

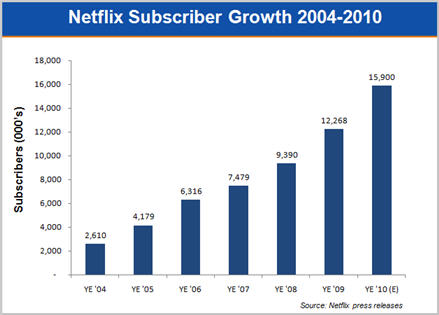

The start of Netflix's virtuous cycle is obvious: the company's introduction of its free "Watch Instantly" streaming feature in January, 2007. Streaming has fundamentally changed the Netflix service offering and consumers are increasingly aware of this. Traditionally, Netflix subscription plans were defined by limits - 1 DVD out at a time for $8.99/mo, 2-out for $13.99/mo or 3-out for $16.99/mo. But with the company's decision to remove the confusing original caps it placed on streaming consumption and move to an unlimited model, Netflix is now providing enormous new value at the same DVD rental price points. Netflix has also changed how it advertises its services, strongly emphasizing streaming (see its home page for example). The "unlimited streaming" message is breaking through and Netflix subscriber growth momentum over the last 3 years reflects this.

Subscribers grew to 12.3 million at the end of '09, 31% higher than YE '08. To get a sense of Netflix's momentum, '09 growth handily beat '08 (26%) and '07 (18%) growth. The 2.9 million subs added in '09 was 85% above the company's own 2009 beginning year forecast of 1.56 million sub additions. Looking ahead, the mid-point of Netflix's forecast for '10 is for another 30% growth in subs.

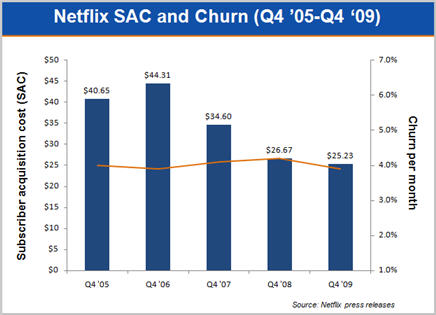

As the streaming benefits have resonated, it's very important to note that subscriber growth is actually getting progressively cheaper for Netflix to accomplish. As the following graph shows, Netflix's subscriber acquisition cost (SAC) has decreased by an impressive 43% from $44.31 in Q4 '06 to $25.23 in Q4 '09 (the 2nd lowest SAC in the company's history). Better still, the quality of these new subs seems high; average monthly churn in Q4 '09 was 3.9%, equal to the lowest churn the company has ever achieved. While Netflix isn't "buying" growth with low-quality additions (an old trick for subscription-oriented businesses), it is however putting more emphasis on the "1-out" service, which, with the addition of unlimited streaming, is an outstanding value for the low-end of the market. Netflix is eager to penetrate this segment, to whom $1 Redbox rentals are very attractive.

While Netflix's financials already reflect the virtuous cycle impact streaming is having on the business, it is likely there is much more to come as streaming takes further hold. Netflix revealed that 48% of its subscribers streamed at least 15 minutes/mo in Q4 '09, up from 41% in Q3 '09 and 26% in Q4 '08 (Incidentally, I think it's conceivable that 80% or more of recently-added subscribers are streaming). But it's just in the last year that Netflix streaming has begun to make the move from computer-only consumption to TV-based consumption, truly making it a mainstream experience. Netflix has inked deals with all the major game consoles (with a Wii marketing campaign beginning in '10), plus numerous CE devices, Blu-ray players, etc. Just ahead is a future where Wi-Fi will be ubiquitous in all new TVs and Netflix's deals with all the major TV manufacturers will ensure it is even more front and center for consumers.

To make streaming attractive, Netflix has had to essentially build a second content library. As I've suggested in the past, this isn't easy, as the company must navigate a thicket of pre-existing Hollywood rights and business relationships. Most notably, Netflix has run into the premium cable networks (HBO, Showtime, Starz and Epix) which have a monopoly on Hollywood's output for their release window. Netflix's deal with Starz was an important first step but still, I've been skeptical that Netflix would land streaming deals with the others.I'm now gaining more confidence that this will indeed happen, especially for these networks' original productions. Netflix is simply getting too big to ignore. It represents a whole new revenue opportunity for premium channels, plus an important loyalty-building outlet. Further out though, while Netflix CEO Reed Hastings says he wants the company to be a distributor for these premium channels, I think it's nearly inevitable that Netflix will compete head-on with them for Hollywood's output. Economics dictate that eventually it makes more sense for Netflix to bid directly for Hollywood rights than work through a premium channel middleman.

In fact, Netflix already has tons of Hollywood relationships, and its recent deal with Warner Bros, creating a 28-day DVD window is emblematic of how Netflix looks at streaming content acquisition going forward. In that superb deal, which was ludicrously criticized by some, Netflix simultaneously helped a critical partner sustain its DVD sales window, while gaining cheaper access to more DVD copies on day 29 and increased streaming rights for catalog titles. As Hastings pointed out on the Q4 earnings call, given the inconsistencies in DVD release strategies, most consumers have little-to-no idea when a title becomes available on DVD, so, while still early, opening up the 28 day window has caused no subscriber complaints. And the company's analysis of subscriber "Queues" indicates, just 27% of requests are for newly-released titles.

Importantly, Netflix's strategy is to pour savings from its DVD deals into streaming content acquisition. As I noted recently, Netflix's detailed subscriber data and usage analysis gives it a huge asymmetric advantage in negotiating additional streaming licenses from Hollywood. Netflix can surgically concentrate its resources on only those titles it knows its subscribers will value. Over time, as DVD sales continue to collapse, Netflix will be there to offer its subs a broader and broader rental selection.

The biggest challenge to Netflix for streaming content acquisition is how much it chooses to spend. Netflix's relatively small size among giants like Comcast and others is what prompted me to suggest over a year ago that Microsoft would acquire Netflix. I'm officially retracting that prediction now, as 2009 demonstrated how much streaming progress Netflix can make on its own. In fact, I think all rumors of a possible Netflix acquisition are off-base; I see the company remaining independent for some time to come.

Netflix is now riding a serious wave and its executives recognize the mile-wide opportunity ahead of it. The product is immeasurably stronger and more appealing with unlimited streaming included. That's in turn leading to impressive sub growth with much-reduced SAC and improving churn. The number of devices bridging Netflix to the TV is growing and portends ubiquity at some point down the road as these devices further leverage Netflix's platinum consumer brand. Streaming content selection is improving, bringing side benefits of reduced DVD postage and inventory costs. With millions of subscribers Netflix now has both the economics and the scale to be a very significant player in the video ecosystem.

Last but not least is a very favorable competitive climate. Aside from a hobbled Blockbuster, astoundingly, Netflix doesn't have any other direct DVD subscription/online streaming hybrid competitor (Amazon and Apple, are you paying attention?). And while Comcast and other multichannel video programming distributors ("MVPDs") are rolling out TV Everywhere services (5 years later than they should have, in my opinion), these are still early stage, and still encumbered by archaic regional limitations. Indeed, Netflix's growth may well cause these companies to consider their own over-the-top plans, as I've suggested.

For years I have been saying that broadband video is the single most disruptive influence on the traditional video distribution value chain. Netflix's success with streaming and the consequences that are yet to play out are resounding evidence of this. Above and beyond YouTube, Hulu, Amazon, Apple and others, Netflix is by far the most important video distributor to watch.

What do you think? Post a comment now (no sign-in required)

Categories: Aggregators, Devices

Topics: Comcast, Netflix, Warner Bros.

-

4 Items Worth Noting for the Jan 25th Week (Netflix Q4, Nielsen ratings, AOL-StudioNow, Net Neutrality Webinar)

With the new Apple iPad receiving wall-to-wall coverage this week, it was easy to overlook other significant news. Here are 4 items worth noting for the January 25th week:

1. Netflix Q4 earnings increase my bullishness - On Wednesday, Netflix reported blowout results for Q4 '09, adding almost 3 million subscribers during the year (and a million just in Q4), bringing their YE '09 subscriber count to 12.3 million. Netflix also forecasted to end this year with between 15.5 million and 16.3 million subscribers, implying subscriber growth will be in the range of 26% to 33%. Importantly, Netflix also said that 48% of its subscribers used the company's streaming feature to watch a movie or TV show in Q4, up from 41% in Q3 and 28% a year ago. Wall Street reacted with glee, sending the stock up $12 yesterday to a new high of $63.04.

VideoNuze readers know I've been bullish on Netflix for some time now, and the Q4 results make me more so. A key concern I've had has been around their ability to gain further premium content for streaming. On the earnings call, CEO Reed Hastings and CFO Barry McCarthy addressed this issue, offering up additional details of their content strategy and how the recent Warner Bros. 28-day DVD window deal will work. On Monday I'm planning a deep dive post based on what I heard. As a preview, I'm now convinced that Netflix is the #1 cord-cutting threat. Cable, satellite and telco operators need to be watching Netflix very closely.

2. Nielsen announces combined TV/online ratings plan, but still falls short - This week brought news that Nielsen intends to unveil a "combined national television rating" in September that merges traditional Nielsen TV ratings with certain online viewing data. This is data that TV networks have been hungering for as online viewing has surged, potentially siphoning off TV audiences. I pointed out recently that the lack of such a measurement could seriously retard the growth of TV Everywhere, as cable networks hesitate to risk shifting TV audiences to unmeasurable online viewing.

Nielsen's move is welcome, but still doesn't go far enough. As reported, it seems the new merged ratings will only count online views that had the same ads and ad load as on-air. That immediately rules out Hulu, which of course carries far fewer ads than on-air, and sometimes uses custom creative as well. Obviously if the new Nielsen ratings don't truly capture online viewership they'll be worth little in the market. Ratings are a story with many future chapters to come.

3. AOL acquires StudioNow in bid for to ramp up video content - Also not to be overlooked this week was AOL's acquisition of StudioNow for $36.5 million in cash. StudioNow operates a distributed network of 3,000 video producers, creating cost-effective video for small and large companies alike. I'm very familiar with StudioNow, having spoken with their CEO and founder David Mason a number of times.

AOL is clearly looking to leverage the StudioNow network to generate a mountain of new video content, complementing its Seed.com "content farm." In addition, AOL picks up StudioNow's recently-launched Video Asset Management & Syndication Platform (AMS) which gives it video management capabilities as well. For AOL the deal suggests the company is finally waking up to video's vast potential. But with the rise of online video syndication, it's still a question mark whether creating a whole lot of new video is the right strategy, or whether AOL would have been better served by just partnering with a syndicator like 5Min.

Meanwhile, AOL isn't the only portal realizing video is the place to be. In Yahoo's earnings call this week, CEO Carol Bartz said "Frankly, our competition is television" and as Liz wrote, Bartz also said "that makes video really important." Yahoo just partnered with Ben Silverman's new Electus indie video shop, and it sounds like more action is coming. Geez, the prospect of AOL and Yahoo competing on acquisitions? It would be like the old days again.

4. Net Neutrality webinar next Thursday is going to be awesome - A reminder that next Thurs, Feb. 4th at 11am PT/2pm ET The Diffusion Group and VideoNuze will present a complimentary webinar "Demystifying Net Neutrality." The webinar is the first in a series of 6 throughout 2010, exclusively sponsored by ActiveVideo Networks. Colin Dixon from TDG and I will be hosting and we have 2 fabulous guests, who are on opposing sides of the net neutrality debate: Barbara Esbin, Senior Fellow and Director of the Center for Communications and Competition Policy at the Progress and Freedom Foundation and Chris Riley, Policy Counsel for Free Press.

Net neutrality is a critically important part of the landscape for over-the-top video services, and yet it is widely misunderstood. Join us for this one-hour session which promises to be educational and impactful.

Enjoy your weekend!

Categories: Aggregators, Broadband ISPs, Deals & Financings, Portals, Regulation, Webinars

Topics: AOL, Net Neutrality, Netflix, Nielsen, StudioNow, Webinar

-

VideoNuze Report Podcast #47 - January 29, 2010

Daisy Whitney and I are pleased to present the 47th edition of the VideoNuze Report podcast, for January 29, 2010.

With the old adage that "everything's been said, but not everyone's said it" in mind, in this week's podcast Daisy and I talk about what else but the new Apple iPad. Daisy actually attended the iPad unveiling at the Yerba Buena Center for the Arts on Wednesday and offers her first hand observations.

Generally we're in agreement that the iPad is not going to rock the video universe any time soon, with Daisy's write-up here, and my write-up here. We do however disagree about the role of the e-book reader functionality of the iPad. Daisy thinks that, at least for now, Apple should position the iPad as a better e-book reader to the Kindle and other products, while I think that would be pigeonholing it and, because at 2x the price of the Kindle, the iPad's enhanced features would be unlikely to peel off many Kindle buyers anyway. Regardless, given Steve Jobs's aspirations for the iPad, it is almost certainly out of the question that he would narrow the iPad's positioning so drastically; I'm guessing he'd rather see it wither on store shelves first.

Click here to listen to the podcast (13 minutes, 9 seconds)

Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!

-

The New Apple iPad - What's It Mean for Online and Mobile Video?

Steve Jobs finally made it official yesterday, unveiling the iPad before a world breathlessly awaiting the next big thing from Apple's factory of wonders. The device did not disappoint from a coolness perspective. It is a digital Swiss army knife of sorts, capable of browsing the web, playing games, reading books, looking at photos, working on docs, etc. all in a gorgeous ("intimate" in Jobs's words) package. All that aside, my main interest has been how significant will the iPad be for video providers and specifically for the evolution of online and mobile video? For now anyway, I think the answer is "not very."

For the iPad to breakthrough for video providers it has to sell really well, creating an addressable universe of millions, if not tens of millions of users. Only widespread adoption makes it a potential game-changer for

video economics, possibly enhancing the paid business model. That may happen over time, but in the immediate future I think it's doubtful. For as cool as the iPad is, in many ways, it's still a "gadget" - overflowing with novelty and packed with status appeal, but hard-pressed to be defined as a "must have" device like a cell phone or a laptop. Maybe I'm really missing something but I still haven't drunk the Kool-Aid for why tablets are going to be so critical in users' lives.

video economics, possibly enhancing the paid business model. That may happen over time, but in the immediate future I think it's doubtful. For as cool as the iPad is, in many ways, it's still a "gadget" - overflowing with novelty and packed with status appeal, but hard-pressed to be defined as a "must have" device like a cell phone or a laptop. Maybe I'm really missing something but I still haven't drunk the Kool-Aid for why tablets are going to be so critical in users' lives.To me, the question comes down to how many people will be able to identify the distinct value the iPad brings them and deem it worthy of purchase? Apple certainly exceeded expectations by offering a $499 low-end iPad, putting it in spitting distance for those who may have been clamoring just for an e-book reader and are willing to step up a bit more. But the $499 price is somewhat illusory. If you want connectivity beyond your home or sporadic Wi-Fi hotspots, you'll need to buy at least the lowest end 3G-enabled iPad, for $629. And you'll certainly buy the case to protect that gorgeous screen, likely for another $50. So with tax you're in the $700 range. But the real killer is you'll almost certainly need to take the iPad's $30/mo AT&T all-you-can-eat 3G service to get online when you're outside your house or within reach of a Wi-Fi hotspot.

Despite the iPad's claim that its price is "well within reach," I think that for all but a pretty narrow slice of Americans, that's not the case - $700 plus another $30/mo easily puts it in the "considered purchase" zone for most potential buyers. Think about it another way: if the iPhone had not been so heavily subsidized by AT&T and other carriers, bringing its price down to $100-$200, how many iPhones do you think Apple would have sold at $500-$600 apiece? Not many is right. And that's for a device that has at least partial "must have" appeal (it is a cell phone after all). Now I know Apple just reported a blow-out holiday quarter, but America is still mired in a recession, with high joblessness and the vast majority of people cutting back on discretionary purchases.

Meanwhile, in the demo yesterday, Jobs showed off how well a YouTube video looks on the iPad, and of course, as with the iPods and the iPhone you can purchase and download video from iTunes. But is there something new that the iPad specifically does for video, beyond delivering a more intimate experience? Is the iPad going to offer some new, previously unavailable video access? Or some new interactivity? Or something else Jobs will conjure? If there is, it wasn't demo'd yesterday. Maybe in time.

These days video providers are inundated with options for where to focus their attention and allocate their scarce resources. Online distribution (on their own sites and/or syndicated)? Mobile? Over-the-top devices? Aggregators? IPTV? VOD? Short form? Long form? Branded content? The list goes on and on. Resources are tight and the first filter for any new initiative is always, "how many eyeballs and potential dollars does it offer?"

Of course, over time the iPad's price will come down and more people will adopt it, making it incrementally more attractive. Its beautiful screen, enabling a fabulous video experience, will help sell the device itself. But Apple will still need to surmount certain niggly things like what do about lack of Flash (like the iPhone it's not currently supported by the iPad, meaning no watching Hulu, just for starters), limited battery life when watching video and AT&T's already-overloaded 3G network, which is bound to disappoint iPad buyers. And beyond these, the larger question looms: if I'm interested in watching video on the go on a nice large screen, why not just do so on my laptop, which is almost certainly with me already?

The iPad is a revolutionary device and an Apple engineering marvel. But as a consumer proposition, it's a much bigger leap for Apple to succeed. With Macs, the iPod and the iPhone, Apple made better, revolutionary products in categories that already existed. With the iPad, Apple is trying to create a whole product new category, looking for daylight where none may exist. Maybe it will be big, maybe not. In the near term, I'm skeptical that it will have any major impact for video providers and for the evolution of online and mobile video.

What do you think? Post a comment now (no sign-in required).

Categories: Devices

-

Join Me for Net Neutrality Webinar With TDG on Thurs. Feb 4th

I'm excited to announce that VideoNuze has partnered with The Diffusion Group, one of the leading digital media research firms, to host a series of 6 complimentary webinars in 2010. The webinars are sponsored

exclusively by ActiveVideo Networks. Each webinar will focus on one specific topic key to the evolving online video/digital media landscape (suggestions are welcome btw!). Colin Dixon from TDG and I will host the webinars and we will also have 1-2 expert guests joining us each time to provide diverse perspectives and insight.

exclusively by ActiveVideo Networks. Each webinar will focus on one specific topic key to the evolving online video/digital media landscape (suggestions are welcome btw!). Colin Dixon from TDG and I will host the webinars and we will also have 1-2 expert guests joining us each time to provide diverse perspectives and insight.The first webinar in the series will be "Demystifying Net Neutrality" on Thursday, February 4th at 11am PT / 2pm ET. If you're in the digital media industry, it's been hard to miss the intense recent debate over net neutrality, sparked by FCC Chairman Julius Genachowski's speech last September, which called for the FCC to impose unprecedented new Internet regulations. However, earlier this month, the DC Court of Appeals indicated it may invalidate the FCC's 2008 order punishing Comcast for blocking BitTorrent traffic, suggesting the FCC may not even have proper authority to regulate the Internet after all. Meanwhile, large and small media and technology companies have continued to heavily lobby the FCC, providing data and arguments on both sides of the issue.

Net neutrality is so important, the argument goes, because as new over-the-top players (e.g. Netflix, Xbox, Roku, Boxee, etc.) seek to bring video services into the home, they need to be assured their services won't be impaired by broadband ISPs like cable operators Comcast and Time Warner Cable or telcos like Verizon and AT&T, who also happen to be the largest incumbent video providers themselves. Opponents essentially argue that net neutrality is a solution in search of a problem, and that the Internet has thrived until now due to the government keeping its hands off, and it should stay that way.

On the webinar, Colin and I will untangle all of this, with the assistance of Chris Riley, Policy Counsel for Free Press, a national, nonpartisan organization working to reform the media, which is a leading proponent of net neutrality and another guest, TBD who is opposed to net neutrality. The webinar promises to be a deep-dive educational session examining all of net neutrality's pros and cons. For anyone with a stake in broadband/online content delivery, it will be a must attend session.

Categories: Broadband ISPs, Regulation, Webinars

Topics: FCC, Free Press, Net Neutrality, Webinar

-

Kyte Launches Console 2.0, Emphasis on Ease-of-Use

More online video platform product news today, as Kyte is unveiling its Console 2.0 product. Last week, COO Gannon Hall gave me a rundown of the new features, which include enhanced work flows, playlist creation, channel and player management and show scheduling among others.

It's no news that OVPs are in an intense feature war, and it is increasingly important for each player to find points of differentiation. Three things that Kyte has focused on to separate itself from the pack are support

for user generated content, mobile devices and social/video sharing. Gannon sees the UGC functionality as particularly important as Kyte is seeing customer demand growing for user engagement opportunities. Two customer examples he cited were ESPN's "Talk of the Terrace" live studio show in the U.K., which actively solicits user contributions (pictures, video and text), and McGraw-Hill's "Professor for a Day" initiative, which encourages students to upload a short video of themselves delivering a lecture on a subject of their choosing.

for user generated content, mobile devices and social/video sharing. Gannon sees the UGC functionality as particularly important as Kyte is seeing customer demand growing for user engagement opportunities. Two customer examples he cited were ESPN's "Talk of the Terrace" live studio show in the U.K., which actively solicits user contributions (pictures, video and text), and McGraw-Hill's "Professor for a Day" initiative, which encourages students to upload a short video of themselves delivering a lecture on a subject of their choosing. In these and other UGC examples, it's critical to be able to quickly moderate submissions and approve them for publishing. In the case of ESPN, Gannon noted that they had a multi-step approval process through compliance and copyright officers, which Kyte enabled. The proliferation of video capturing devices like smartphones and personal video cameras, plus the intense desire by brands to engage their audience, suggests that UGC support will become a more important OVP feature. As far as I'm aware, the only other OVP that has really emphasized UGC moderation is VMIX, a situation that is likely to change.

Mobile is another area where Kyte is trying to differentiate itself. Though its app frameworks for iPhone and Blackberry, and soon Nokia and Android, customers are able to quickly build apps for these mobile devices and then, using Kyte's Mobile Producer feature, can manage and publish video to their channels. Gannon said that for example, Fox News now routinely has field reporters capturing video with iPhones and then uploading it for audience viewing. Kyte was also involved in quickly turning around an iPhone app for last Friday's "Hope for Haiti" digital telethon.

I continue to believe that the world is getting more and more complicated for content producers. That's a theme that I've heard repeatedly at the NATPE conference in Las Vegas, where I am now. In the old days content people focused on producing great content, and then others worried about distribution and audience development. What's changing in the digital era is that content producers need to be just as focused on distribution in order to generate an ROI. In this respect OVPs are playing a more important role, providing the work flow, distribution and engagement functionality. Making all of this ever easier and more effective will continue to be a primary success factor for OVPs.

What do you think? Post a comment now (no sign-in required).

Categories: Technology

Topics: Kyte

-

Brightcove Makes Its First Move Into TV Everywhere

This morning Brightcove is making its first TV Everywhere ("TVE") related announcement, introducing its "TV Everywhere Solution Pack" (TVE-SP), which is the Brightcove 4 enterprise edition augmented with new components and services to support TVE rollouts. It is also unveiling a strategic alliance with Ping Identity to integrate its PingFederate security software with TVE-SP, to enable user authentication and authorization. Lastly, Brightcove has promoted Eric Elia from VP of Professional Services to VP of TV Solutions, charged with leading the company's TVE initiatives. Brightcove's CEO and founder Jeremy Allaire briefed me last week.

To understand how TVE-SP fits in, it is important to quickly review the TVE model. To date, most discussion of TVE has focused on multichannel video programming distributors ("MVPDs") providing their subscribers with online access to TV programming through

their own portals or services, for no extra charge (e.g. Comcast's Fancast Xfinity TV). Receiving less attention so far is that the programmers who agree to participate in MVPD portals will likely require they are also able to offer their same programs on their own sites, which are an increasingly important part of their brand identity and direct-to-consumer focus.

their own portals or services, for no extra charge (e.g. Comcast's Fancast Xfinity TV). Receiving less attention so far is that the programmers who agree to participate in MVPD portals will likely require they are also able to offer their same programs on their own sites, which are an increasingly important part of their brand identity and direct-to-consumer focus. Something else that hasn't received a lot of attention to date is that not all MVPDs will follow Comcast's model of managing, hosting and delivering the online programs themselves. Rather, some MVPDs will prefer to provide just the barebones online navigation, with TV programmers providing an embeddable video player and also delivering all the programming. Less-resourced MVPDs could end of relying heavily on programmers to power their TVE offerings. Where programmers already have online video platforms such as Brightcove in place, these OVPs are in a position to influence how TVE operates. (As a sidenote, I've heard multiple times that Comcast itself is also offering a white labeled version of its FXTV portal to other MVPDs).

All of this means there's likely to be plenty of heterogeneity in TV Everywhere rollouts. Recognizing this, a key part of Brightcove's product strategy is aligning with Ping to use PingFederate and the SAML 2.0 standard for user authentication and authorization. SMAL is used to exchange data between domains (e.g. between a TV programmer, whose web site visitor is trying to access a certain program and an MVPD which holds that user's subscription profile). This type of secure exchange will be essential for TV programmers to offer their own programs on their own sites in a TVE world.

SAML has been widely used in the SaaS business applications and Ping itself lists Comcast, Cox, Bell Canada and Discovery, among others, as customers. However, I suspect these are likely on the enterprise side, not the consumer-facing side. As a result, Brightcove's approach will require significant testing before it will be deemed acceptable by MVPDs. In fact, Brightcove's new white paper indicates that additional standards are required and that some of this is underway at CableLabs, the cable industry's development lab.

It's also worth noting that thePlatform (owned by Comcast) has 4 of the top 5 U.S. cable operators, plus Rogers in Canada, as customers, and ExtendMedia has the major U.S. telcos, plus Bell Canada, as customers. With Brightcove powering video at 60+ TV programmer websites, there are no doubt some interesting dynamics ahead as these OVPs' customers negotiate their TVE relationships and influence the interoperability of their respective technology providers. For its part, thePlatform, which also supports many content providers' video, introduced last November an "Authentication Adaptor" as part of its media publishing system to smooth the authentication and authorization process for programmers offering TVE shows on their own sites.

Confused yet? This is pretty dense stuff, and illustrates some of the hurdles ahead for TVE's widespread rollout. Meanwhile, lurking over TVE's shoulder are the raft of over-the-top alternatives (e.g. Netflix, Boxee, Apple, Xbox, YouTube, etc.) that are sure to gain additional traction with consumers (as a sidenote, yesterday's Best Buy Sunday circular promoted no fewer than 5 Blu-ray players as Netflix compatible, with each showcasing the Netflix logo).

As the TVE story unfolds, Brightcove is sure to be in the middle of the action given its market presence and technical capabilities. But how it all shakes out remains to be seen.

What do you think? Post a comment now (no sign-in required).

(Note - Brightcove, thePlatform and ExtendMedia are VideoNuze sponsors)

Categories: Technology

Topics: Brightcove, Comcast, ExtendMedia, Ping Identity, thePlatform

VideoNuze Posts

Connect with VideoNuze

Exclusive News Roundup

- Delta, YouTube Ink Inflight Entertainment Partnership The Hollywood Reporter

- The NFL and YouTube are getting closer, and their relationship could change everything NY Times

- NFL Commissioner Roger Goodell says league could renegotiate media deals as soon as 2026 CNBC

- Big Media Companies Spent $210 Billion on Content in 2024, Led by Comcast, YouTube and Disney Variety

- As Wired Turns Its Journalists Into Influencers, Subscriptions Surge Adweek

- Gemini is coming to Google TV starting today The Verge