-

Comcast's Digital Transformation Continues

A year ago, in "Comcast: A Company Transformed," I asserted that in the past 10 years Comcast has dramatically evolved from a traditional, plain vanilla cable TV operator to a digital TV, broadband Internet access and voice powerhouse. Comcast's Q3 '09 earnings, released last week, offered more proof that the company continues its transformation, capitalizing on consumers' shift to digital lifestyles.

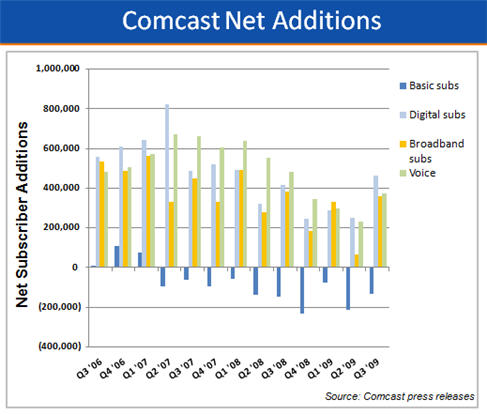

As the chart below shows, Comcast's Q3 results were once again powered by higher digital TV penetration in its cable TV subscriber base, and additional broadband and voice subscribers.

These gains offset the steady erosion in Comcast's total number of cable subs, which at the end of Q3 stood at approximately 23.8 million. Comcast has lost cable subs for 10 straight quarters (totaling 1.25 million) as competition from satellite and new telco video entrants takes its toll. Still, the company has been able to drive revenue per video subscriber steadily higher, to $116.91/month in Q3 '09, reflecting the value of product bundling and success in its business services area. As I said last year, Comcast has effectively moved "up-market," targeting consumers who are willing and able to afford a $100-$200 monthly bill to enjoy the modern digital lifestyle.

Even as the company continues to turn in solid financial performance, Comcast's slowing growth in the core areas of digital TV, broadband and voice are evident in the chart below, which converts the net additions to each service, plus the contraction in basic video subs, into trend lines. With the exception of a few sporadic blips up, over the past 3 years, all 3 areas have shown a steady deceleration in growth. For example, in the most recent 4 quarters (Q4 '08 - Q3 '09), Comcast added 3.4 million digital TV, broadband and voice subs, but this was down 38% vs. the 5.5 million digital TV, broadband and voice subs it added in the year earlier 4 quarters (Q4 '07 - Q3 '08). In the most recent 4 quarters, Comcast also lost 657,000 cable subs, vs. 436,000 in the earlier 4 quarter period, a 51% increase.

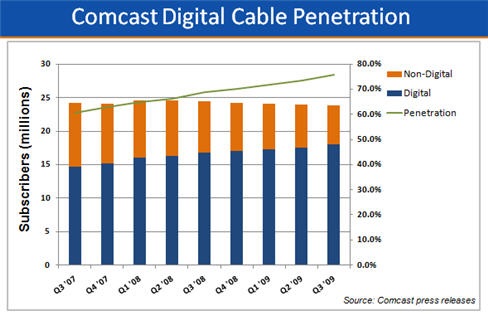

Meanwhile, a big bright spot over the last 3 years for Comcast has been the strong progress it has made in converting its subscriber base to digital TV. As the chart below shows, digital TV penetration now stands at nearly 76% of cable subs, up from about 69% at the end of Q3 '08, and about 61% at the end of Q3 '07. Between bundling, new digital channels, HD, VOD, an improved channel guide and DVR availability, Comcast has strengthened the value proposition for subscribers to convert to a digital set-top box, bringing the company higher revenues and a larger universe to deliver new services to, not to mention a stronger defense against possible cord-cutting.

With the slowdown in net additions occurring, Comcast has clearly begun contemplating where new growth, as well as expense reduction, will come from. Given its negotiations for a controlling stake in NBCU, for now it looks like the company's main strategy is deepening its stake in the content business. Since Comcast hasn't even formally acknowledged the negotiations, much less revealed what the financial and strategic benefits any deal might offer, it's too early to weigh the deal's pros and cons.

Should the deal happen though, it will certainly absorb significant management resources. Given how important an effective rollout of TV Everywhere is to the company, anything that distracts from this task would be a setback. Further, as I recently speculated in "How TV Everywhere Could Turn Cable Operators and Telcos Into Over-the-Top's Biggest Players," Comcast must also keep an eye on competitive drivers that might require it to serve video outside of its traditional geographical footprint (note, Comcast executives say there are no such plans). Doing so would be a herculean management challenge. Last week's research revealing that potentially 54% of Netflix's 11.1 million subscribers now use the service to stream video each month was a reminder that powerful national competitors are steadily building their IP-based delivery businesses through a variety of connected CE devices. These kinds of "over-the-top" services are inevitably competitive to Comcast and other incumbent video providers.

As Comcast has transformed itself into a digital powerhouse it has positioned itself extremely well for continued market leadership. How it chooses to allocate its vast resources, and then how well it executes on its choices will determine how much of its significant potential is realized.

What do you think? Post a comment now.

Categories: Cable TV Operators

Topics: Comcast

-

New Forrester Report Evaluates 6 Online Video Platforms

On Friday, Forrester Research released an analysis of 6 online video platform vendors. As with other comparison reports that come out regularly, Forrester's will have value as a starting point in evaluating options, but should be considered far from definitive.

With only 6 vendors evaluated, the biggest shortcoming of the new report (parts of which I've seen) is its lack of comprehensiveness. Selecting the field is always a key issue in any comparison process. And when trying to evaluate a market like online video platforms, with dozens of competitors, there's a natural tension between comprehensiveness and quality/cost. The broader the field that Forrester chose to evaluate, the more time-consuming and costly the report would have been to produce.

The downside of choosing only 6 is that a lot of other high-quality competitors, along with their particular strengths, are left out. This clearly skews overall conclusions. In Forrester's case it's also not entirely clear why the 6 - Brightcove, Ooyala, Kaltura, VMIX, Fliqz and Twistage - were actually chosen. For example, the report indicates that vendors that primarily focus on the high end of the market such as thePlatform and Digitalsmiths were not included. Yet arguably, Brightcove has as much focus on premium content providers as either of these companies do. thePlatform is also the most established player in the market, so to not include it means missing a critical market benchmark.

Forrester used 37 criteria to evaluate the vendors, grouped into 3 categories, Current Offering, Strategy and Market Presence. The sources of the data it used to assign scores to each vendor for the criteria were vendor surveys, product demos and customer reference calls. All of this is very useful, but it appears that Forrester did not do any hands-on testing itself. Having seen so many demos myself, I've come to believe that the only way to truly get a sense of the vendor's work flow and specific capabilities is to use with the platform directly. By definition demos are orchestrated to shine the best light on a platform's work flow; it's only through using one day-to-day that a nitty-gritty understanding can be gained.

Lastly, Forrester's conclusion that Brightcove and Ooyala are "Leaders," Kaltura and VMIX are "Strong Performers," and Twistage and Fliqz are "Contenders" feels like it could be more rigorous. For example, if statements like "stay away from these guys, they're truly inferior" or "if x, y and z features are critical to you, look no further" had been used, the reader would gain more clarity on where Forrester stands. Instead each vendor seems to have its own strengths, while weaknesses such as "...lack strong capabilities in areas such as distribution and scalability..." seem too high level.

All of this said, for customers looking for a first-cut evaluation of a limited segment of the market (which is how Forrester itself seems to be positioning the report), it is a useful tool. Whether it's worth the $1,749 asking price is another matter. I'd recommend also having a look at sources like VidCompare.com and the market snapshot from Marketing Mechanics.

What do you think? Post a comment now.

Categories: Technology

Topics: Forrester Research

-

4 Items Worth Noting for the Nov 2nd Week (Q3 earnings review, Blu-ray streaming, Apple lurks, "Anywhere" coming)

Following are 4 items worth noting for the Nov 2nd week:

1. Media company and service provider earnings underscore improvements in economy - This was earnings week for the bulk of the publicly-traded media companies and video service providers, and the general theme was modest increases in financial performance, due largely to the rebounding economy. The media companies reporting - CBS, News Corp, Time Warner. Discovery, Viacom and the Rainbow division of Cablevision - showed ongoing strength in their cable networks, with broadcast networks improving somewhat from earlier this year. For ad-supported online video sites, plus anyone else that's ad-supported, indications of a healthier ad climate are obviously very important.

Meanwhile the video service providers reporting - Comcast, Cablevision, Time Warner Cable and DirecTV all showed revenue gains, a clear reminder that even in recessionary times, the subscription TV business is quite resilient. Cable operators continued their trend of losing basic subscribers to emerging telco competitors (with evidence that DirecTV might now be as well), though they were able to offset these losses largely through rate increases. Though some people believe "cord-cutting" due to new over-the-top video services is real, this phenomenon hasn't shown up yet in any of the financial results. Nor do I expect it will for some time either, as numerous building blocks still need to fall into place (e.g. better OTT content, mass deployment of convergence devices, ease-of-use, etc.)

2. Blu-ray players could help drive broadband to the TV - Speaking of convergence devices, two articles this week highlighted the role that Blu-ray players are having in bringing broadband video to the living room. The WSJ and Video Business both noted that Blu-ray manufacturers see broadband connectivity as complementary to the disc value proposition, and are moving forward aggressively on integrating this feature. Blu-ray can use all the help it can get. According to statistics I recently pulled from the Digital Entertainment Group, in Q3 '09, DVD players continue to outsell Blu-ray players by an almost 5 to 1 ratio (15 million vs. 3.3 million). Cumulatively there are only 11.2 Blu-ray compatible U.S. homes, vs. 92 million DVD homes.

Still, aggressive price-cutting could change the equation. I recently noticed Best Buy promoting one of its private-label Insignia Blu-ray players, with Netflix Watch Instantly integrated, for just $99. That's a big price drop from even a year ago. Not surprisingly, Netflix's Chief Content Officer Ted Sarandros said "streaming apps are the killer apps for Blu-ray players." Of course, Netflix execs would likely say that streaming apps are also the killer apps for game devices, Internet-connected TVs and every other device it is integrating its Watch Instantly software into. I've been generally pessimistic about Blu-ray's prospects, but price cuts and streaming could finally move the sales needle in a bigger way.

3. Apple lurks, but how long will it stay quiet in video? - The week got off to a bang with a report that Apple is floating a $30/mo subscription idea by TV networks. While I think the price point is far too low for Apple to be able to offer anything close to the comprehensive content lineup current video service providers have, it was another reminder that Apple lurks as a major potential video disruptor. How long will it stay quiet is the key question.

While in my local Apple store yesterday (yes I'm preparing to finally ditch my PC and go Mac), I saw the new 27 inch iMac for the first time. It was a pretty stark reminder that Apple is just a hair's breadth away from making TVs itself. Have you seen this beast yet? It's Hummer-esque as a workstation for all but the creative set, but, stripped of some of its computing power to cost-reduce it, it would be a gorgeous smaller-size TV. Throw in iTunes, a remote, decent content, Apple's vaunted ease-of-use and of course its coolness cachet and the company could fast re-order the subscription TV industry, not to mention the TV OEM industry. The word on the street is that Apple's next big product launch is a "Kindle-killer" tablet/e-reader, so it's unlikely Steve Jobs would steal any of that product's thunder by near-simultaneously introducing a TV. If a TV's coming (and I'm betting it is), it's likely to be 2H '10 at the earliest.

4. Get ready for the "Anywhere" revolution - Yesterday I had the pleasure of listening to Emily Green, president and CEO of tech research firm Yankee Group, deliver a keynote in which she previewed themes and data from her forthcoming book, "Anywhere: How Global Connectivity is Revolutionizing the Way We Do Business." Emily is an old friend, and 15 years ago when she was a Forrester analyst and I was VP of Biz Dev at Continental Cablevision (then the 3rd largest cable operator), she was one of the few people I spoke to who got how important high-speed Internet access was, and how strategic it would become for the cable industry. 40 million U.S. cable broadband homes later (and 70 million overall) amply validates both points.

Emily's new book explores how the world will change when both wired and wireless connectivity are as pervasive as electricity is today. No question the Internet and cell phones have already dramatically changed the world, but Emily makes a very strong case that we ain't seen nothing yet. I couldn't help but think that TV Everywhere is arriving just in time for video service providers whose customers increasingly expect their video anywhere, anytime and on any device. "Anywhere" will be a must-read for anyone trying to make sense of how revolutionary pervasive connectivity is.

Enjoy your weekends!

Categories: Aggregators, Books, Broadcasters, Cable Networks, Cable TV Operators, Devices

Topics: Best Buy, Bl, Cablevision, CBS, Comcast, DirecTV, Netflix, News Corp, Rainbow, Time Warner Cable, Time Warner. Discovery, Viacom

-

VideoNuze Report Podcast #39 - November 6, 2009

Daisy Whitney and I are pleased to present the 39th edition of the VideoNuze Report podcast, for November 6, 2009.

This week Daisy and I first dig into the research I shared about Netflix's Watch Instantly users that I wrote about earlier this week. The research, by One Touch Intelligence and The Praxi Group, indicated that 62% of respondents have used the Watch Instantly streaming feature, with 54% saying they use it to watch at least 1 movie or TV show per month. Daisy and I discuss the significance of these and other data from the research. As a reminder the research is available as a complimentary download from VideoNuze.

Daisy is in NY this week attending Ad:Tech, and she then shares observations from a couple of sessions she's attended. In particular she passes on the advice that Sir Martin Sorrell, head of large agency holding company WPP, about where the advertising business is heading and how he's preparing WPP for the future.

Click here to listen to the podcast (14 minutes, 45 seconds)

Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!

Categories: Advertising, Aggregators, Podcasts

-

YouTube As the Ultimate Brand Engagement Platform

Surfing over to YouTube the other day, I was struck by how the site could well become the ultimate brand engagement platform. Below is a screen shot of what I found - nearly all the visible real estate showcased 2 different brand contests encouraging users to submit videos for a chance to win prizes.

The first contest, the "Kodak True Colors: Video Portrait Challenge," was just kicking off, and therefore had prominent positioning. The contest urges users to submit as many 10-second videos as they'd like in pursuit of a grand prize including 2 tickets to a taping of the "Conan O'Brien" show. The other contest, "The Best of Us Challenge," by the International Olympic Committee, shows athletes doing something outside their specialty (e.g. Michael Phelps doing speed putting, Lindsey Jacobellis doing the hula hoop) and asks user to emulate these or create their own challenge. The winner receives a trip for 2 to the 2010 Vancouver winter games. The contest was featured in YouTube's "Spotlight," a section on the home page populated by YouTube's editors based on user ratings.

These types of brand contest are not necessarily new, nor are their inclusion in YouTube. Over a year ago I suggested there was real opportunity in what I called "purpose-driven user-generated video" - the idea that with YouTube turning millions of people into amateur video producers, their enthusiasm and skills could be channeled to specific purposes. The success of campaigns like Doritos' $1 Million Super Bowl challenge has amply demonstrated that great creative and great buzz can be generated from a well-executed UGV campaign.

What YouTube's home page that day demonstrated to me is that as brands continue embracing online video and user participation, the go-to partner will be YouTube. There's simply no better way to reach a broad audience of likely contestants than by making a big splash on YouTube. While YouTube's monetization challenges have become one of the most-talked about industry topics this year, I'd argue there's been insufficient focus on the fact that since May '08, YouTube's share of overall video viewing has stayed right around 40%, at least according to comScore. In that time, YouTube's videos viewed per month have more than doubled, from 4.2 billion, to 10.4 billion in September '09.

Even as sites like Hulu and others have launched and promoted new and innovative sites, YouTube continues to retain its share of the fast-growing online video market. YouTube has also matured considerably, with its Content ID system largely sanitizing the site from pirated video and helping change its perception among copyright owners. (Note that on my recent visit to YouTube I searched in vain for a video of Johnny Damon's double steal in Game 4 and found nothing but "This video is no longer available due to a copyright claim by MLB Advanced Media." In the old days a video like that would have been available all over the site.)

While YouTube has made headway adding premium content partners, a significant part of its appeal remains users uploading and sharing videos. YouTube's combination of massive audience, ubiquitous brand, user interactivity and promotional flexibility make it an ideal partner for brands looking to engage their audiences through video.

Last summer I got plenty of flak for my post, "Does It Actually Matter How Much Money YouTube Loses?" in which I argued that YouTube's long-term strategic value (and Google's financial muscle to support the site's short-term losses) superseded the company's current losses. While I didn't mean to suggest in that post that a company can afford to lose money forever, I was trying to contend that YouTube, the dominant player in a fast-growing and highly disruptive market will eventually find its way to profitability and is well worth Google's continued investment.

YouTube is a rare example of a "winner take all" situation; there is no other video upload and sharing site even on the radar. As video becomes ever more strategic for all kinds of brands, they will increasingly recognize that YouTube is a must-have partner. If Google can't figure out how to make lemonade out of YouTube's lemons, then shame on them. I'm betting, however, that they will.

What do you think? Post a comment now.

Categories: Aggregators, Brand Marketing, UGC

Topics: Doritos, Google, IOC, Kodak, YouTube

-

New Research on Netflix's "Watch Instantly" Shows Surging Usage

Netflix's "Watch Instantly" streaming video usage is surging, according to new research by One Touch Intelligence, in association with The Praxi Group. The firms surveyed a qualified online panel of 1,000 Netflix subscribers in October. I've been eagerly following the Netflix's streaming initiative and this is the first research I've seen which reveals Netflix subscribers' Watch Instantly usage patterns. I'm pleased to offer the top-line results and analysis as a complimentary download.

Click here to download the research

The research confirms that Watch Instantly ("WI") enjoys broad support, with 62% of respondents (extrapolated to approximately 6.9 million of Netflix's 11.1 million subscribers) reporting that they have used WI since it was introduced and 54% (extrapolated to approximately 6 million subs) saying that they use it to watch at least 1 movie or TV show per month. Netflix itself has only disclosed (on its recent Q3 '09 earnings call) that 42% of its subscribers streamed at least 15 minutes of a TV show or movie during the 3rd quarter.

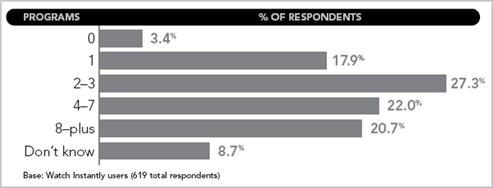

Netflix subscribers also appear to be using WI intensively, watching an average 6 titles per month. The following chart shows the distribution of usage from zero to 8+ titles per month.

WI usage is heavily tilted toward movie watching, with 92% saying they've used WI to stream a movie vs. 55% for a TV show. For each monthly usage level, more movies were watched than TV shows, likely reflecting the fact that movies are the majority of the 17,000 title WI catalog.

Though Netflix has made huge strides in embedding the WI client software in CE devices (e.g. Xbox, Roku, Blu-ray DVD players, PS3, etc.), over 60% of WI viewing still happens on the computer. Coming in second, with 13.4% is computers connected to a TV. Only then do the CE devices start showing up in the research: video game console (11.1%), DVD player (5.7%) and Roku (3.6%). Clearly we're still in the very early days of the "convergence era" where broadband is widely connected to the TV. The research does highlight that the 3.6% Roku figure could be extrapolated to suggest that about 400,000 Roku devices are being used by Netflix subscribers, a relatively strong showing by the company.

Meanwhile, if you thought Netflix WI would be leading to rampant "cord-cutting" of current video services (cable/satellite/telco), think again. Only 2% of the respondents said they've cancelled their incumbent video service, and it should be noted that the question asked if the disconnect was due to Netflix in general, not just WI in particular.

Further encouraging to current video service providers is that 67% of respondents say they prefer to have both a Netflix and a cable/satellite subscription. Asked if they had to give up one, 20% said they'd give up Netflix first vs. 13% who said they'd give up cable/satellite first. None of this is reason for incumbent for relax - especially as WI and other streaming video services are poised to improve - but it does suggest that at least for now, Netflix isn't an either/or proposition for most people.

This is just a quick summary of the findings; there's more available in the report. My view is that Netflix has made enormous progress with WI in a very short period of time. The decision to make it a value add to subscribers, rather than charging for it, has no doubt been key. In fact, TV Everywhere providers have wisely taken a cue from WI by also planning to offer TVE as a value add. Netflix has also made WI extremely easy to use, with only 15% of survey respondents saying it is "too complicated to use regularly." This too is a lesson for others to follow.

With WI offering the prospect of Netflix lowering its massive postage bill, reducing its DVD inventory, and providing greater convenience to its subscribers, we can expect the company to continue investing heavily in WI. The big challenge for Netflix, as I've noted many times before, is beefing up their content selection. With WI the company is running into the thicket of prevailing Hollywood release windows which are not going to dramatically change any time soon. Still, I continue to consider Netflix the best-positioned emerging player in broadband-only premium video delivery. This story is still in its earliest days.

(Thanks to One Touch's Stewart Schley for providing the research)

What do you think? Post a comment now.

Categories: Aggregators

Topics: Netflix, One Touch Intelligence, The Praxi Group

-

More on Comcast's "Excalibur" Project

Last week's piece in Cable Digital News, "Comcast Forges Excalibur for IPTV" generated a number of emails to my inbox. Despite an oddly misleading title using the primarily telco-oriented term "IPTV," the substance of the article caught lots of people's attention. It explained that Comcast, America's largest cable operator, has set up a new division, "Comcast Converged Products" (CCP) and that Comcast "...would put all IP services, including video, into a common provisioning and management system."

VideoNuze readers who contacted me interpreted Excalibur as being the basis for a potential out-of-market, over-the-top (OTT) plan by Comcast. These folks were referencing a post I wrote in September, "How TV Everywhere Could Turn Cable Operators and Telcos Into Over-the-Top's Biggest Players," in which I

asserted that the next phase of TV Everywhere - "TVE 2.0" as I called it - could well find incumbent service providers invading each others' geographical turf with an IP/broadband-only service. While this type of move would represent a major break from traditional industry norms, I suggested that it may be irresistible for growth reasons and inevitable for competitive reasons.

asserted that the next phase of TV Everywhere - "TVE 2.0" as I called it - could well find incumbent service providers invading each others' geographical turf with an IP/broadband-only service. While this type of move would represent a major break from traditional industry norms, I suggested that it may be irresistible for growth reasons and inevitable for competitive reasons. I talked to a Comcast spokesperson yesterday to learn more about Excalibur and to ferret out any indications that it could indeed be the basis for a Comcast OTT play. According to the spokesperson, Excalibur's mission is to "use IP to deliver cross-platform interactive services." The spokesperson noted that it would be a mistake to think of these as solely video-oriented. Comcast already uses IP technology extensively in its network and Excalibur is meant to find ways to "improve the consumer experience across platforms." One example cited was a feature like checking your voicemail from the Comcast.net portal.

When pressed for specifics on CCP deployments, new products or timelines, the spokesperson said there are no specific plans at this time. The spokesperson did confirm that Sam Schwartz (formerly the head of Comcast Interactive Capital) has been appointed president of CCP, but said the "core Excalibur team" is smaller than the 100 people that CDN reported. I referenced my recent OTT post and the spokesperson had no comment on my speculation Comcast would go out of footprint.

Admittedly that doesn't add a lot of new detail about Excalibur. From my perspective, I'm dubious that the company would reassign Schwartz to anything that wasn't highly strategic. While using IP to enhance the customer experience is worthwhile, Comcast has major competitive battles brewing that are critical to focus on. Yesterday's news that Apple is floating a $30 subscription offering is a reminder that the Steve Jobs lion will pounce at some point. Similarly, Netflix, which just reported superb Q3 results, broad usage of its streaming feature, an integration with PS3 (and a rumored one with the Wii) is looking more and more like a national cable competitor, leveraging myriad CE devices. Others to be mindful of include YouTube, Hulu and Amazon. These are of course in addition to fierce satellite and telco rivals.

Given all of this, Comcast's smartest move would in fact be to reassign its savviest tech-oriented executive, given him/her a large team and task him/her with ensuring the company's competitiveness in the face of new entrants. In particular, gaming how to compete with Apple should be near the top of the list. Apple has shown an uncanny ability to reinvent markets with its easy-to-use, ultracool devices. While gaining access to cable programming is far from a slam-dunk, Apple's ability to innovate is unmatched, potentially making it a totally new kind of cable competitor.

Last week, coming out of the CTAM Summit, I expressed concern that the cable industry was not fully recognizing online video as a bona fide new medium, which it needs to embrace and capitalize on. For now Excalibur's real agenda is murky; time will tell how aggressive it is.

What do you think? Post a comment now.

Categories: Cable TV Operators

Topics: Apple, Comcast, Excalibur, Netflix

-

Health-Related Video Vertical Poised for Growth

Last week brought two announcements suggesting that the health-related video vertical market is poised for growth: first, that HealthiNation will be distributing its videos on AT&T U-Verse and HealthGrades, and the second, that HealthCentral is partnering with 5Min to syndicate its videos across 5Min's distribution network.

I've been following HealthiNation for a while and last week CEO and co-founder Raj Amin told me that the AT&T deal brings to about 28 million the number of American homes where HealthiNation's content is

available on video-on-demand (VOD). Raj's enthusiasm for VOD distribution helps validate points I made last May in "Made-for-Broadband Video and VOD are Looking Like Peanut Butter and Chocolate," in which I suggested that rather than broadband video and VOD being competitive with each other, they can actually complement each other well.

available on video-on-demand (VOD). Raj's enthusiasm for VOD distribution helps validate points I made last May in "Made-for-Broadband Video and VOD are Looking Like Peanut Butter and Chocolate," in which I suggested that rather than broadband video and VOD being competitive with each other, they can actually complement each other well. In HealthiNation's case, Raj indicated that VOD distribution is particularly important for its sponsors, as they value views in the living room in addition to those on the computer, where most broadband video occurs today. The multiple ways that VOD is promoted by incumbent video providers given HealthiNation's content lots of visibility. The downside Raj noted is that VOD lacks the same interactivity/engagement opportunities as viewing online provides, and that inserting ads is not nearly as easy. The latter means that HealthiNation must manually attach ads to each of its VOD streams. This would be extremely laborious for content providers with hundreds or thousands of titles, but for HealthiNation, which offers dozens of VOD titles at a time, it is manageable. Raj emphasizes that VOD's ability to help surround the consumer with content and sponsor messages is a key differentiator for HealthiNation, and a key reason it has pushed hard into VOD.

HealthiNation's strategy is primarily to syndicate its content rather than be a destination site, and it has over 50 partners in its network now, with potential reach of about 40 million unique visitors/month. HealthiNation insists that its video be played in its player, and that it controls the ad inventory. This is primarily because of its commitments to its sponsors (mainly pharma) to deliver only highly targeted viewers, provide detailed performance metrics and use mostly display ads, not pre-rolls. All of these contribute to HealthiNation offering a differentiated value proposition relative to typical TV ads.

Separate, HealthiNation also announced a partnership last week with HealthGrades, which is the leading provider of ratings information on doctors, hospitals and nursing homes. Overall Raj said that at its peak, HealthiNation is now generating 3 million uniques/month. It has over 300 videos that are 2-3 minutes long (or longer for VOD) and growing. The company has raised $12.5 million in total, and Raj says it will be profitable in 2010.

Meanwhile last week also brought news that HealthCentral, a large online provider of health-related content and operator of a health-related online ad network, is partnering with 5Min, a video syndicator which I wrote

about here. Under the deal HealthCentral's videos will be added to 5Min's existing health library, for syndication to over 350 different sites. HealthCentral will take on exclusive ad sales responsibilities for pharma and OTC clients for 5Min's video focused on health, specific conditions, parenting, pregnancy, fitness and nutrition.

about here. Under the deal HealthCentral's videos will be added to 5Min's existing health library, for syndication to over 350 different sites. HealthCentral will take on exclusive ad sales responsibilities for pharma and OTC clients for 5Min's video focused on health, specific conditions, parenting, pregnancy, fitness and nutrition. The HealthCentral deal is similar to the recent deal 5Min did with Scripps Networks in the food and home & garden categories. In both, 5Min landed a large anchor content partner, to which it then gave exclusive ad sales responsibilities for part of the category. In this way 5Min gains both valuable content and also category-specific advertising expertise. I continue to like how 5Min is building out its model methodically across important content categories.

Even as Washington slogs through health care reform legislation, the health-related online video space is rapidly evolving. More than ever, individuals recognize the need to educate themselves. Video provides a breakthrough way to simply and completely explain complex ideas. As a result I see lots of growth ahead in this vertical.

What do you think? Post a comment now.

Categories: Indie Video, Telcos, Video On Demand

Topics: 5Min, AT&T U-verse TV, HealthCentral, HealthGrades, HealthiNation

VideoNuze Posts

Connect with VideoNuze

Exclusive News Roundup

- Netflix says it’s streamed 95 billion hours in 2025, and a lot of ads too The Verge

- NBCUniversal’s Peacock Is Hiking Prices by $3 per Month Variety

- MLB Commissioner says Sunday media rights could go to NBC, Apple - or back to ESPN CNBC

- Media Vet Peter Liguori Appointed CEO Of VideoAmp After Leading The Ad Tech Firm As Executive Chairman Deadline

- PubMatic Launches AI Sports Ad Marketplace for Live Streaming Adweek

- Broadcast Falls Below 20 Percent of TV Use for the First Time The Hollywood Reporter